Exam 20: Accounting Changes and Error Corrections

Exam 1: Environment and Theoretical Structure of Financial Accounting181 Questions

Exam 2: Review of the Accounting Process 139 Questions

Exam 3: The Balance Sheet and Financial Disclosures168 Questions

Exam 4: The Income Statement, Comprehensive Income, and the Statement of Cash Flows178 Questions

Exam 5: Revenue Recognition316 Questions

Exam 6: Time Value of Money Concepts126 Questions

Exam 7: Cash and Receivables187 Questions

Exam 8: Inventories: Measurement182 Questions

Exam 9: Inventories: Additional Issues153 Questions

Exam 10: Property, Plant, and Equipment and Intangible Assets: Acquisition149 Questions

Exam 11: Property, Plant, and Equipment and Intangible Assets: Utilization and Disposition223 Questions

Exam 12: Investments183 Questions

Exam 13: Current Liabilities and Contingencies155 Questions

Exam 14: Bonds and Long-Term Notes256 Questions

Exam 15: Leases262 Questions

Exam 16: Accounting for Income Taxes176 Questions

Exam 17: Pensions and Other Postretirement Benefits246 Questions

Exam 18: Shareholders Equity179 Questions

Exam 19: Share-Based Compensation and Earnings Per Share231 Questions

Exam 20: Accounting Changes and Error Corrections152 Questions

Exam 21: The Statement of Cash Flows Revisited192 Questions

Select questions type

A company failed to record unrealized gains of $20 million on its available for sale debt security investments. Its tax rate is 30%. As a result of this error, comprehensive income would be:

(Multiple Choice)

4.9/5  (44)

(44)

C. Good Eyeglasses overstated its inventory by $30,000 at the end of 2018. In 2019, the discovery of this error, before adjusting or closing entries, would require:

(Multiple Choice)

4.9/5 (38)

Which of the accounting changes listed below is more associated with financial statements prepared in accordance with U.S. GAAP than with International Financial Reporting Standards (IFRS)?

(Multiple Choice)

4.9/5 (29)

What are the changes in accounting principle that require the prospective approach?

(Essay)

4.9/5 (29)

The cumulative effect of most changes in accounting principle is reported:

(Multiple Choice)

4.9/5 (36)

Name and briefly describe the three categories of accounting changes.

(Essay)

4.8/5 (44)

An item that should be reported as a prior period adjustment is the:

(Multiple Choice)

4.8/5 (34)

When an accounting change is reported under the retrospective approach, account balances in the general ledger:

(Multiple Choice)

4.8/5 (29)

Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the most correct term.

-Prospective approach

(Multiple Choice)

4.9/5 (38)

Retrospective restatement usually is appropriate for a change in:

(Multiple Choice)

4.9/5 (28)

In the previous year, a firm failed to record premium amortization of $40,000 and $30,000, respectively, on its bonds payable and held to maturity bond investments. These errors affect both income before tax and taxable income. The firm's tax rate is 30%. As a result of this error, net income was:

(Multiple Choice)

4.9/5 (41)

Indicate the nature of each of the situations described below using the following three-letter code.

CODE DESCRIPTION

CPR: Change in principle reported retrospectively

CPP: Change in principle reported prospectively

CES: Change in estimate

CRE: Change in reporting entity

PPA: Prior period adjustment required

_____ Technological advance that renders worthless a patent with an unamortized cost of $45,000.

_____ Change from LIFO inventory costing to average inventory costing.

_____ Including in the consolidated financial statements a subsidiary acquired several years earlier that was appropriately not included in previous years.

_____ Change from FIFO inventory method to LIFO.

_____ Pension plan assets for a defined benefit pension plan achieving a rate of return in excess of the amount anticipated.

_____ Change from the pay-as-you-go method to estimating warranty expense in the period the related product is sold.

_____ Change from declining balance depreciation to straight-line.

_____ Change from determining lower of cost or net realizable value for inventories by the individual item approach to the aggregate approach.

_____ Settling a lawsuit for less than the amount accrued previously as a loss contingency.

_____ Change in the estimated useful life of office equipment.

(Essay)

4.9/5 (35)

Which of the following accounting changes should not be accounted for prospectively?

(Multiple Choice)

4.7/5 (35)

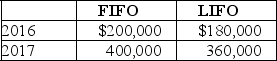

Macintosh Inc. changed from LIFO to the FIFO inventory costing method on January 1, 2018.

Inventory values at the end of each year since the inception of the company are as follows:  Required:

Ignoring income tax considerations, prepare the entry to report this accounting change.

Required:

Ignoring income tax considerations, prepare the entry to report this accounting change.

(Essay)

4.8/5 (28)

National Hoopla Company switches from sum-of-the-years' digits depreciation to straight-line depreciation. As a result:

(Multiple Choice)

4.8/5 (33)

Due to an error in computing depreciation expense, Prewitt Corporation overstated accumulated depreciation by $20 million as of December 31, 2018. Prewitt has a tax rate of 30%. Prewitt's retained earnings as of December 31, 2018, would be:

(Multiple Choice)

4.9/5 (29)

There is not always a clear-cut distinction between a change in estimate and a change in principle or a simultaneous change in estimate and change in principle. How are such situations accounted for?

(Essay)

4.9/5 (32)

Which of the following is not an example of a change in accounting principle?

(Multiple Choice)

4.7/5 (44)

Most changes in accounting principle require a disclosure justifying the change in the first set of financial statements that the change is made.

(True/False)

4.9/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)