Exam 5: Risk and Return: Past and Prologue

Exam 1: Investments: Background and Issues55 Questions

Exam 2: Asset Classes and Financial Instruments59 Questions

Exam 3: Securities Markets60 Questions

Exam 4: Managed Funds and Other Investment Companies60 Questions

Exam 5: Risk and Return: Past and Prologue58 Questions

Exam 6: Efficient Diversification56 Questions

Exam 7: Capital Pricing and Arbitrage Pricing Theory59 Questions

Exam 8: The Efficient Market Hypothesis and Behavioral Finance60 Questions

Exam 9: Bond Prices and Yields58 Questions

Exam 10: Managing Bond Portfolios60 Questions

Exam 11: Equity Valuation60 Questions

Exam 12: Macroeconomic and Industry Analysis58 Questions

Exam 13: Financial Statement Analysis55 Questions

Exam 14: Options and Risk Management60 Questions

Exam 15: Futures and Risk Management60 Questions

Exam 16: Investors and the Investment Process60 Questions

Exam 17: Hedge Funds60 Questions

Exam 18: Portfolio Performance Evaluation54 Questions

Select questions type

Treasury notes are paying a 4% rate of return. A risk averse investor with a risk aversion of A = 3 should invest in a risky portfolio with a standard deviation of 24% only if the risky portfolio's expected return is at least ________.

(Multiple Choice)

4.7/5  (30)

(30)

Your timing was good last year. You invested more in your portfolio right before prices went up and you sold right before prices went down. In calculating historical performance measures which one of the following will be the largest?

(Multiple Choice)

4.9/5 (38)

You are considering investing $1000 in a complete portfolio. The complete portfolio is composed of Treasury notes that pay 5% and a risky portfolio, P, constructed with two risky securities X and Y. The optimal weights of X and Y in P are 60% and 40% respectively. X has an expected rate of return of 14% and Y has an expected rate of return of 10%. To form a complete portfolio with an expected rate of return of 11%, you should invest ________ of your complete portfolio in Treasury notes.

(Multiple Choice)

4.8/5 (44)

Your investment has a 40% chance of earning a 15% rate of return, a 50% chance of earning a 10% rate of return and a 10% chance of losing 3%. What is the standard deviation of this investment?

(Multiple Choice)

4.9/5 (26)

You are considering investing $1000 in a complete portfolio. The complete portfolio is composed of Treasury notes that pay 5% and a risky portfolio, P, constructed with two risky securities X and Y. The optimal weights of X and Y in P are 60% and 40% respectively. X has an expected rate of return of 14% and Y has an expected rate of return of 10%. The dollar values of your positions in X, Y, and Treasury notes would be ________, ________ and ________ respectively if you decide to hold a complete portfolio that has an expected return of 8%.

(Multiple Choice)

4.9/5 (38)

Suppose you pay $9700 for a $10 000 par Treasury bond maturing in three months. What is the holding period return for this investment?

(Multiple Choice)

4.8/5 (36)

You invest $1000 in a complete portfolio. The complete portfolio is composed of a risky asset with an expected rate of return of 16% and a standard deviation of 20% and a Treasury bond with a rate of return of 6%. You should invest ________ of your complete portfolio in the risky portfolio if you want your complete portfolio to have a standard deviation of 9%.

(Multiple Choice)

5.0/5 (33)

The rate of return on ________ is known at the beginning of the holding period while the rate of return on ________ is not known until the end of the holding period.

(Multiple Choice)

4.8/5 (39)

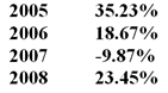

You have the following rates of return for a risky portfolio for several recent years:  The annualised average return on this investment is ________.

The annualised average return on this investment is ________.

(Multiple Choice)

4.7/5 (36)

You have $500 000 available to invest. The risk-free rate as well as your borrowing rate is 8%. The return on the risky portfolio is 16%. If you wish to earn a 22% return, you should ________.

(Multiple Choice)

4.9/5 (45)

Consider the following two investment alternatives. First, a risky portfolio that pays 15% rate of return with a probability of 40% or 5% with a probability of 60%. Second, a Treasury bond that pays 6%. The risk premium on the risky investment is ________.

(Multiple Choice)

4.8/5 (32)

An investment earns 10% the first year, 15% the second year and loses 12% the third year. Your total compound return over the three years was ________.

(Multiple Choice)

4.9/5 (38)

You have calculated the historical dollar-weighted return, annual geometric average return and annual arithmetic average return. You always reinvest your dividends and interest earned on the portfolio. Which method provides the best measure of the actual average historical performance of the investments you have chosen?

(Multiple Choice)

4.9/5 (32)

You have calculated the historical dollar-weighted return, annual geometric average return and annual arithmetic average return. If you desire to forecast performance for next year, the best forecast will be given by the ________.

(Multiple Choice)

5.0/5 (32)

You invest $1000 in a complete portfolio. The complete portfolio is composed of a risky asset with an expected rate of return of 16% and a standard deviation of 20% and a Treasury bond with a rate of return of 6%. The slope of the capital allocation line formed with the risky asset and the risk-free asset is ________.

(Multiple Choice)

4.9/5 (42)

The return on the risky portfolio is 15%. The risk-free rate as well as the investor's borrowing rate is 10%. The standard deviation of return on the risky portfolio is 20%. If the standard deviation on the complete portfolio is 25%, the expected return on the complete portfolio is ________.

(Multiple Choice)

4.9/5 (34)

One method to forecast the risk premium is to use the ________.

(Multiple Choice)

4.8/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)