Exam 18: Portfolio Performance Evaluation

Exam 1: Investments: Background and Issues55 Questions

Exam 2: Asset Classes and Financial Instruments59 Questions

Exam 3: Securities Markets60 Questions

Exam 4: Managed Funds and Other Investment Companies60 Questions

Exam 5: Risk and Return: Past and Prologue58 Questions

Exam 6: Efficient Diversification56 Questions

Exam 7: Capital Pricing and Arbitrage Pricing Theory59 Questions

Exam 8: The Efficient Market Hypothesis and Behavioral Finance60 Questions

Exam 9: Bond Prices and Yields58 Questions

Exam 10: Managing Bond Portfolios60 Questions

Exam 11: Equity Valuation60 Questions

Exam 12: Macroeconomic and Industry Analysis58 Questions

Exam 13: Financial Statement Analysis55 Questions

Exam 14: Options and Risk Management60 Questions

Exam 15: Futures and Risk Management60 Questions

Exam 16: Investors and the Investment Process60 Questions

Exam 17: Hedge Funds60 Questions

Exam 18: Portfolio Performance Evaluation54 Questions

Select questions type

Consider the theory of active portfolio management. Shares A and B have the same positive alpha and the same non-systematic risk. Share A has a higher beta than share B. You should want ________ in your active portfolio.

Free

(Multiple Choice)

4.9/5  (41)

(41)

Correct Answer: Verified

Verified

A

It is very hard to statistically verify abnormal fund performance because of all except which one of the following?

Free

(Multiple Choice)

4.9/5 (37)

Correct Answer:Verified

D

What is the contribution of security selection to relative performance?

Free

(Multiple Choice)

4.9/5 (40)

Correct Answer:Verified

A

A managed portfolio has a standard deviation equal to 22% and a beta of 0.9 when the market portfolio's standard deviation is 26%. The adjusted portfolio P________ needed to calculate the M2 measure will have ________ invested in the managed portfolio and the rest in T-bonds.

(Multiple Choice)

4.9/5 (34)

In the Treynor-Black model, the weight of each analysed security in the portfolio should be proportional to its ________.

(Multiple Choice)

4.9/5 (39)

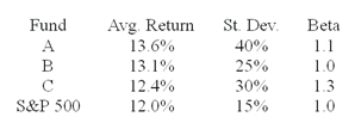

The average returns, standard deviations and betas for three funds are given below along with data for the S&P 500 index. The risk-free return during the sample period is 6%.  You wish to evaluate the three mutual funds using the Treynor measure for performance evaluation. The fund with the highest Treynor measure of performance is ________.

You wish to evaluate the three mutual funds using the Treynor measure for performance evaluation. The fund with the highest Treynor measure of performance is ________.

(Multiple Choice)

4.9/5 (35)

The portfolio that contains the benchmark asset allocation against which a manager will be measured is often called ________.

(Multiple Choice)

5.0/5 (40)

Shares A and B have alphas of .01 and betas of .90. Share A has a residual variance of .020 while share B has a residual variance of .016. If Share A represents 2% of an active portfolio, share B should represent ________ of an active portfolio.

(Multiple Choice)

4.8/5 (38)

A portfolio generates an annual return of 13%, a beta of 0.7 and a standard deviation of 17%. The market index return is 14% and has a standard deviation of 21%. What is the M2 measure of the portfolio if the risk-free rate is 5%?

(Multiple Choice)

4.9/5 (31)

Perfect timing ability is equivalent to having ________ on the market portfolio.

(Multiple Choice)

4.9/5 (30)

The risk-free rate, average returns, standard deviations and betas for three funds and the S&P500 are given below.  What is the T2 measure for Portfolio A?

What is the T2 measure for Portfolio A?

(Multiple Choice)

4.8/5 (37)

A portfolio generates an annual return of 17%, a beta of 1.2 and a standard deviation of 19%. The market index return is 12% and has a standard deviation of 16%. What is the M2 measure of the portfolio if the risk-free rate is 4%?

(Multiple Choice)

4.8/5 (32)

Consider the theory of active portfolio management. Shares A and B have the same beta and the same positive alpha. Share A has higher non-systematic risk than share B. You should want ________ in your active portfolio.

(Multiple Choice)

4.9/5 (39)

Suppose that over the same period two portfolios have the same average return and the same standard deviation of return, but Portfolio A has a higher beta than Portfolio B. According to the Sharpe measure, the performance of Portfolio A ________.

(Multiple Choice)

4.8/5 (29)

Henriksson found that, on average, betas of funds ________ during market advances.

(Multiple Choice)

4.8/5 (33)

Portfolio managers Paul Martin and Kevin Krueger each manage $1 000 000 funds. Paul Martin has perfect foresight and the call option value of his perfect foresight is $150 000. Kevin Krueger is an imperfect forecaster and correctly predicts 50% of all bull markets and 70% of all bear markets. The value of Kevin Krueger's imperfect forecasting ability is ________.

(Multiple Choice)

4.7/5 (44)

A market timing strategy is one where asset allocation in the share market ________ when one forecasts the share market will outperform treasury bonds.

(Multiple Choice)

4.7/5 (45)

A portfolio generates an annual return of 13%, a beta of 0.7 and a standard deviation of 17%. The market index return is 14% and has a standard deviation of 21%. What is the Treynor measure of the portfolio if the risk-free rate is 5%?

(Multiple Choice)

4.7/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)