Exam 7: Monopoly and Its Regulation

Exam 1: What is Economics73 Questions

Exam 2: Markets and Prices78 Questions

Exam 3: The Business Firm: Organization,motivation,and Optimal Input Decisions75 Questions

Exam 4: Getting Behind the Demand and Supply Curves75 Questions

Exam 5: Market Demand and Price Elasticity68 Questions

Exam 6: Economic Efficiency,market Supply,and Perfect Competition72 Questions

Exam 7: Monopoly and Its Regulation77 Questions

Exam 8: Monopolistic Competition,oligopoly,and Antitrust Policy73 Questions

Exam 9: Pollution and the Environment56 Questions

Exam 10: The Supply and Demand for Labor73 Questions

Exam 11: Interest,rent,and Profit70 Questions

Exam 12: Poverty,income Inequality,and Discrimination60 Questions

Exam 13: Economic Growth71 Questions

Exam 14: Public Goods and the Role of the Government70 Questions

Exam 15: National Income and Product71 Questions

Exam 16: Business Fluctuations and Unemployment72 Questions

Exam 17: The Determination of National Output and the Keynesian Multiplier75 Questions

Exam 18: Fiscal Policy and National Output75 Questions

Exam 19: Inflation70 Questions

Exam 20: Money and the Banking System78 Questions

Exam 21: The Federal Reserve and Monetary Policy71 Questions

Exam 22: Supply Shocks and Inflation64 Questions

Exam 23: Productivity,growth,and Technology Policy58 Questions

Exam 24: Surpluses,deficits,public Debt,and the Federal Budget68 Questions

Exam 25: Monetary Policy,interest Rates,and Economic Activity72 Questions

Exam 26: Controversies Over Stabilization Policy70 Questions

Exam 27: International Trade70 Questions

Exam 28: Exchange Rates and the Balance of Payments66 Questions

Select questions type

A firm that realizes minimum average costs at an output rate sufficient to satisfy the entire market is an example of

Free

(Multiple Choice)

4.9/5  (35)

(35)

Correct Answer: Verified

Verified

B

The calculation of marginal revenue is best described by which of the following equations if R(q)equals total revenue for a given level of output (q)?

Free

(Multiple Choice)

4.8/5 (39)

Correct Answer:Verified

D

For a perfectly competitive firm,at any output rate

Free

(Multiple Choice)

4.9/5 (43)

Correct Answer:Verified

E

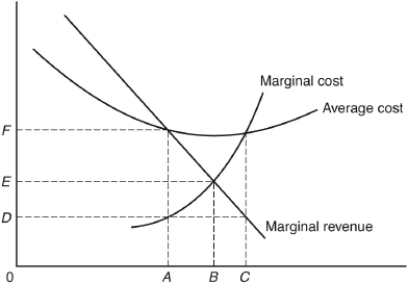

The following question are based on the following diagram of a monopolist:

-If a perfectly competitive,constant-cost industry is monopolized,the

-If a perfectly competitive,constant-cost industry is monopolized,the

(Multiple Choice)

4.8/5 (36)

If people are willing to pay $130 for a particular bicycle and its marginal cost is $80

(Multiple Choice)

4.7/5 (31)

Which of the following firms is the best example of one that has achieved its monopoly advantage because of network externalities?

(Multiple Choice)

4.8/5 (29)

When marginal revenue exceeds marginal cost,a monopolist should reduce

(Multiple Choice)

4.8/5 (47)

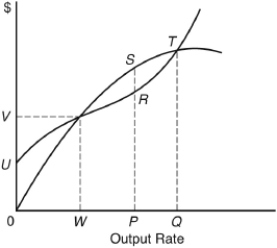

The following question are based on the following graph:

-The total profit at the profit-maximizing output is

-The total profit at the profit-maximizing output is

(Multiple Choice)

4.8/5 (30)

When marginal revenue exceeds marginal cost,a monopolist should

(Multiple Choice)

4.7/5 (38)

A major factor that weakened Standard Oil's monopoly power prior to being broken up by the Supreme Court in 1911 was

(Multiple Choice)

4.8/5 (40)

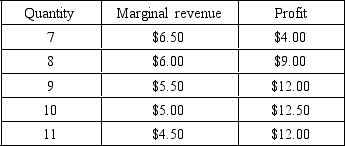

The following question are based on the following data for a monopolist:

-The profit-maximizing output rate is

-The profit-maximizing output rate is

(Multiple Choice)

4.9/5 (31)

For a monopolist the Golden Rule of Output Determination is to set the output rate at the point where marginal revenue equals

(Multiple Choice)

4.8/5 (48)

One problem associated with public regulation of industries has been the tendency for

(Multiple Choice)

5.0/5 (36)

In general,as a monopolist increases its output rate,its profit

(Multiple Choice)

4.7/5 (34)

The following question are based on the following data for a monopolist:

-At the profit-maximizing output rate,marginal costs are

(Multiple Choice)

4.9/5 (37)

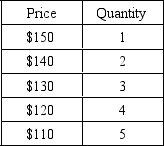

The following question are based on the following demand schedule for a monopolist:

-The marginal revenue associated with the sale of the third unit is

-The marginal revenue associated with the sale of the third unit is

(Multiple Choice)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)