Exam 14: Audit of the Inventory and Distribution Cycle

Exam 1: The Demand for Audit and Other Assurance Services69 Questions

Exam 2: The Public Accounting Profession and Audit Quality68 Questions

Exam 3: Legal Liability55 Questions

Exam 4: Professional Judgment and Ethics72 Questions

Exam 5: Audit Responsibilities and Objectives67 Questions

Exam 6: Client Acceptance and Planning the Audit60 Questions

Exam 7: Materiality and Risk65 Questions

Exam 8: Internal Controls and Control Risk61 Questions

Exam 9: Audit Evidence80 Questions

Exam 10: Audit Strategy and Audit Program67 Questions

Exam 11: Audit Sampling Concepts67 Questions

Exam 12: Audit of the Revenue Cycle134 Questions

Exam 13: Audit of the Acquisition and Payment Cycle64 Questions

Exam 14: Audit of the Inventory and Distribution Cycle66 Questions

Exam 15: Audit of the Human Resources and Payroll Cycle66 Questions

Exam 16: Audit of the Capital Acquisition and Repayment Cycle66 Questions

Exam 17: Audit of Cash Balances65 Questions

Exam 18: Completing the Audit67 Questions

Exam 19: Audit Reports on Financial Statements67 Questions

Exam 20: Other Assurance and Nonassurance Services59 Questions

Select questions type

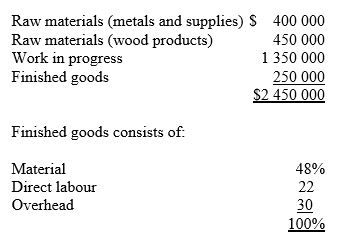

You are conducting the audit of Files R Us Inc. (FRI), a family-owned business that manufactures a variety of different wooden and metal file cabinets. In business for over twenty years, FRI has a reputation for providing high-quality products on time or even ahead of schedule. FRI does not sell to the public, but only to fine furniture stores and to a variety of office supply chains.

As of the current year-end, the company has a total of $6.3 million in assets. Inventory information is as follows:

File cabinet production is intensely competitive, primarily due to imports from Asia and Mexico. To help manage costs, FRI uses a job-order, standard cost system. Standard costs are assessed quarterly. Each job is costed and compared to standard. Inventory is counted only at the end of the year. There is no perpetual inventory system.

Due to problems with raw material quality and new staff, losses have been incurred in the last six months of the year. Your review of last year's audit file indicated that there were numerous inventory adjustments required last year.

Required:

Using the audit risk model, assess the risks associated with the audit of inventory.

File cabinet production is intensely competitive, primarily due to imports from Asia and Mexico. To help manage costs, FRI uses a job-order, standard cost system. Standard costs are assessed quarterly. Each job is costed and compared to standard. Inventory is counted only at the end of the year. There is no perpetual inventory system.

Due to problems with raw material quality and new staff, losses have been incurred in the last six months of the year. Your review of last year's audit file indicated that there were numerous inventory adjustments required last year.

Required:

Using the audit risk model, assess the risks associated with the audit of inventory.

(Essay)

4.9/5  (34)

(34)

Master files, worksheets, and reports that accumulate material, labour, and overhead as the costs are incurred are

(Multiple Choice)

4.8/5 (37)

The test of details of balance procedure that requires the auditor to review contracts with suppliers and customers and inquire of management for the possibility of the inclusion of consigned or other non-owned inventory is an attempt to satisfy the objective of

(Multiple Choice)

4.9/5 (34)

A well-designed computerized system of perpetual inventory data files includes information about the

(Multiple Choice)

4.9/5 (38)

A common inventory observation procedure is to be alert for items that are damaged, rust- or dust-covered, or located in inappropriate places. The balance-related audit objective achieved by this procedure is

(Multiple Choice)

4.8/5 (36)

The existence of an adequate storeroom with a competent custodian in charge results in the orderly storage of inventory and can protect inventory from theft and misuse. How would an auditor assess these controls?

(Multiple Choice)

4.8/5 (38)

When labour is a significant part of inventory, verifying the proper accounting of these costs should be tested in the

(Multiple Choice)

4.9/5 (34)

As part of the audit of valuation, the auditor is conducting pricing tests by comparing to supplier invoices. The auditor is making sure that, for each item tested, sufficient supplier invoices are examined to cover the quantity of inventory that was on hand during the physical inventory count. What type of pricing error could this detect?

(Multiple Choice)

4.9/5 (31)

A) State seven specific balance-related audit objectives for inventory pricing and compilation and, for each objective, describe one common test of details of balances related to that objective.

B) Explain why the audit of work-in-process and finished goods inventory is generally more complex than the audit of purchased inventory.

(Essay)

4.8/5 (42)

XYZ Company uses standard costs for allocating costs to work-in-process and finished goods inventory. For the last few months, there have been high variances between total standard costs and actual costs. What is one of the likely reasons for this variance?

(Multiple Choice)

4.8/5 (38)

Dishware Distribution Limited uses average costing to cost its inventory. It keeps a perpetual inventory file that is linked to its sales systems. It orders inventory in for specific customers as needed, and traditionally has a slow time just before its year-end. Accordingly, inventory at the year-end is about $2000, while materiality is about $30 000. How should the auditor approach the audit of physical inventory?

(Multiple Choice)

4.7/5 (35)

CAS for audit procedures for inventory indicate that the auditor

(Multiple Choice)

4.8/5 (36)

The test of details of balance procedure that requires the auditor to perform tests of lower-of-cost-or-market, selling price, and obsolescence is an attempt to satisfy the objective of

(Multiple Choice)

4.9/5 (33)

Describe the major risks of error or fraud in the inventory and distribution cycle using the headings of i) risks of error, ii) risks of misappropriation of assets, other fraud, or illegal acts, and iii) risks of inadequate disclosure or incorrect presentation of financial information, including fraudulent financial reporting.

(Essay)

4.8/5 (43)

What is the first step that the auditor takes when auditing the valuation of inventory?

(Multiple Choice)

4.9/5 (42)

It is frequently possible to test the physical inventory prior to the balance sheet date when

(Multiple Choice)

4.8/5 (39)

What are inventory price tests and inventory compilation tests? Provide an example of each.

(Essay)

5.0/5 (35)

When auditing merchandise inventory at year-end, the auditor performs a purchase cutoff test to obtain evidence that

(Multiple Choice)

4.8/5 (34)

State six specific balance-related audit objectives for physical inventory observation and, for each objective, describe one common test of details of balances related to that objective.

(Essay)

4.7/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)