Exam 7: Proprietary Type Fundsenterprise and Internal Service Funds

Exam 1: Governmental and Nonprofit Accounting Environment and Characteristics28 Questions

Exam 2: The Use of Funds in Governmental Accounting30 Questions

Exam 3: Budgetary Considerations in Governmental Accounting53 Questions

Exam 4: An Introduction to General and Special Revenue Funds52 Questions

Exam 5: General and Special Revenue Funds Continued62 Questions

Exam 6: Capital Projects Funds, Debt Service Funds, and Permanent Funds49 Questions

Exam 7: Proprietary Type Fundsenterprise and Internal Service Funds42 Questions

Exam 8: Fiduciary Funds54 Questions

Exam 9: Reporting Principles and Preparation of Fund Financial Statements45 Questions

Exam 10: Government-Wide Financial Statements51 Questions

Exam 11: Analysis of Financial Statements and Financial Condition52 Questions

Exam 12: Federal Government Accounting and Reporting53 Questions

Exam 13: Accounting for Nonprofit Organizations59 Questions

Exam 14: Accounting for Health Care Organizations46 Questions

Exam 15: Fundamentals of Accounting45 Questions

Select questions type

The FASB and GASB both have standards for reporting capital asset impairment but with different results. Which of the following is not one of the three methods required by the GASB or the FASB for calculating the impairment of capital assets?

(Multiple Choice)

4.8/5  (38)

(38)

An Internal Service Fund typically provides services to the other funds and departments of a government, such as a motor pool or a data processing service.

(True/False)

4.8/5 (41)

Internal Service Funds may only provide services to individuals or entities outside the government.

(True/False)

4.9/5 (36)

A Water Enterprise Fund (EF) issues $4 million of 5% revenue bonds on October 1, 2018. The EF will make its first payment of interest on March 31, 2019, together with a principal payment of $200,000. What amount, if any, should the EF report in its fund statement of revenues, expenses, and changes in net position for the year ended December 31, 2018?

(Multiple Choice)

4.9/5 (40)

An Enterprise Fund (EF) issued bonds in the amount of $100,000 and immediately acquired capital assets from the bond proceeds at a cost of $100,000. As of December 31, 2018, accumulated depreciation on the assets was $10,000. Also, as of December 31, 2018, the EF had paid back $15,000 of the debt principal. In its December 31, 2018, statement of net position, how much should the EF report as its net investment in capital assets?

(Multiple Choice)

4.9/5 (27)

In some circumstances, Enterprise Funds are permitted to report capital assets using the modified approach? What is one reason why the GASB permits this method versus simple depreciation accounting required by the FASB for businesses?

(Multiple Choice)

4.8/5 (43)

The Weber County Printing Internal Service Fund (ISF) spent $82,000 in cash provided by contributions from the County's General Fund to purchase a commercial quality offset printer. Assuming the printer has an expected useful life of 10 years with no salvage value, which of the following entries should be used to record the printer when acquired and related depreciation at year end?

a. Two entries:

Capital assets-offset printer 82,000 Cash 8,200 To record purchase of offset printer 8,200 Depreciation expense 8,200

b. Two entries:

Capital assets-offset printer 82,000 Capital contributions from General Fund 82,000 To record purchase of offset printer 8,200 Depreciation expense 8,200

c. One entry:

Expenditures-offset printer 8,200 Capital contributions from General Fund 8,200 To record purchase of offset printer

d. One entry:

Expenditures-offset printer 8,200 Cash 8,200 To record purchase of offset printer

(Short Answer)

4.8/5 (37)

The City of Casa Cortez uses an Internal Service Fund (ISF) to provide centralized printing services for all City agencies. City agencies are billed on a per-page basis (number of pages in a document times the number of documents printed). The City requires the ISF to develop its billing rate that it recovers all costs on the accrual basis of accounting, plus the cost of repaying a $400,000 start-up loan made by the City to the ISF. Compute the rate per page to be charged by the ISF, based on the following factors:

a. Start-up loan from City to ISF - $400,000 non-interest bearing loan, to be

repaid in equal payments over 10 years

b. Printing equipment - estimated to cost $300,000 and to have an average life of

10 years

c. Personnel costs - Estimated salaries of $500,000, plus contribution to Pension

Trust Fund of 10% of salaries

d. Paper- Opening inventory of $16,000; expected purchases of $72,000;

expected ending inventory of $12,000

e. Occupancy costs - Estimated at $50,000 per year

f. Expected number of pages to be printed - 20 million.

(Short Answer)

4.8/5 (30)

Revenue bonds are debt that is secured exclusively by the revenues generated by an activity accounted for in a specific fund, generally an Enterprise Fund.

(True/False)

4.9/5 (36)

When Internal Service Funds [ISFs] bill the government's other funds or departments for the services they provide, ISFs report the amount billed as revenues.

(True/False)

4.9/5 (37)

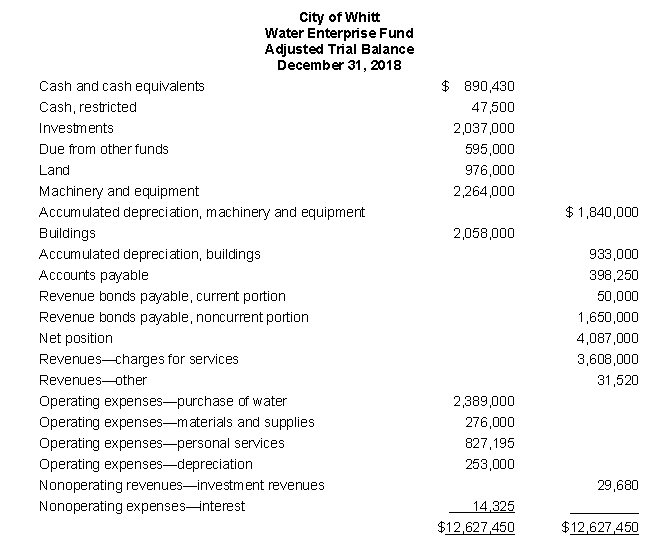

Presented on the following page is the adjusted trial balance for the Water Enterprise Fund of the City of Whitt at December 31, 2018, the end of its fiscal year. Based on this information:

a. Prepare the entry necessary to close the accounts

b. Compute the ending fund net position balances for (1) net investment in capital assets, (2) restricted net position, and (3) unrestricted net position

(Note: Debt related to the capital assets consists solely of the City's revenue bonds payable.)

(Short Answer)

4.9/5 (39)

Twizzle City establishes an Internal Service Fund (ISF) to account for the costs of printing services that it will provide to the various City departments. Make journal entries to record the following transactions in the ISF only.

a. The General Fund transfers $425,000 to the ISF as a contribution to start the printing activity.

b. The ISF immediately uses $400,000 of the cash to purchase printing equipment. (The printing equipment is estimated to have an average useful life of 8 years.)

c. On various occasions during the year, the ISF buys paper and other supplies in the amount of $90,000 on open account. The supplies are put into inventory.

d. Invoices for the supplies purchased in c., above are paid.

e. Employee salaries for the year amounting to $345,000 are paid.

f. The ISF makes a payment of $41,000 for defined contribution pensions for its personnel.

g. The ISF receives an invoice of $28,000 from the General Fund for occupancy costs, which includes space and utility costs.

h. The ISF sends invoices throughout the year to several City agencies for printing services, as follows:

(1) To General Fund departments $575,000

(2) To the Water Enterprise Fund 9,500

i. The ISF receives payments of $555,000 from General Fund agencies and $9,500 from the Water Enterprise Fund.

To prepare its financial statements, the ISF must make adjusting entries to account for the following:

j. To record one-year's depreciation on the equipment purchased in b., above.

k. To record the expense of paper and supplies consumed during the year. A year-end inventory showed unused paper and supplies amounting to $8,000. (See c., above.)

l. To record unpaid salaries of $13,500.

(Short Answer)

4.7/5 (32)

An Enterprise Fund must be used whenever a government charges fees to external users for goods or services.

(True/False)

4.8/5 (37)

When governments establish an activity that must use Enterprise Fund accounting and reporting, many also create a separate legal entity, like a public authority or public corporation.

(True/False)

4.7/5 (41)

These transactions relate to Metro Bus, which provides transportation services to residents of Parker County. Metro Bus is accounted for as a County Enterprise Fund. Make journal entries to account for the following 2018 transactions in the Enterprise Fund.

a. On April 1, 2018, Metro borrows $3,000,000 by issuing 10-year revenue bonds. Bond principal is to be paid back in 20 equal semi-annual installments, starting October 1, 2018, together with interest of 6% a year on the unpaid principal.

b. On July 1, Metro pays cash for 10 buses costing $150,000 each. Metro also pays cash for land costing $100,000 and a building costing $900,000 to house its repair activity.

c. On July 1, Metro invests $200,000 of unused cash in a Certificate of Deposit (CD).

d. Metro pays cash of $50,000 to acquire an inventory of repair parts.

e. Metro collects bus fares of $900,000, which it deposits in the bank.

f. Metro sends an invoice for $10,000 to the County Social Services Agency for taking senior citizens on bus tours. That Agency receives appropriations from the General Fund.

g. Metro pays salaries of $500,000 to its bus operators, mechanics, and administrative staff.

h. The CD (transaction c.) matures and Metro receives a check for $203,000.

i. On October 1, 2018, Metro pays the first installment of principal and interest on the revenue bonds in transaction a.

To prepare its financial statements at December 31, 2018, Metro must make adjusting journal entries for the following items:

j. To record six months' depreciation on the buses and building bought in transaction b. Estimated lives are: buses - 10 years; building - 30 years.

k. To record consumption of repair parts. A year-end physical inventory shows repair parts on hand amounting to $8,000. (See transaction d.)

l. To accrue for unpaid salaries of $12,000.

m. To accrue interest on the revenue bonds outstanding at December 31, 2018. (See transactions a. and i.)

(Short Answer)

4.7/5 (37)

Some Enterprise Funds report special assessments as a revenue source. Which of the following is most descriptive of those assessments or fees?

(Multiple Choice)

4.9/5 (42)

Accounts receivable that an Enterprise Fund estimates won't be collectible are reported as bad debt expense in its statement of revenues, expenses, and changes in fund net position.

(True/False)

4.9/5 (43)

GASB requires governments to report deferred outflows and deferred inflows of assets separate from assets and liabilities.

(True/False)

4.7/5 (39)

Only Enterprise Funds may use the modified approach to report infrastructure assets.

(True/False)

4.9/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)