Exam 12: Reporting and Analyzing Financial Investments

When the fair value of a company's portfolio of available-for-sale equity securities is lower than its book value, how should the difference be handled?

D

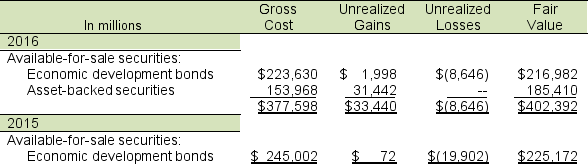

Following is a portion of the investments footnote from Athletic Supply's 2016 annual report.

A. At what amount does Athletic Supply report its available-for-sale securities on its balance sheets for 2016 and 2015?

B. How does Athletic Supply account for its trading securities? How does the accounting differ from their accounting method for available-for-sale?

C. What are the net unrealized gains (losses) for 2016 and 2015? How did these unrealized gains (losses) affect the company's reported income in 2016 and 2015?

D. What is the difference between realized and unrealized gains and losses? Are realized gains and losses treated differently in the income statement than unrealized gains and losses for the available-for-sale securities?

A. At what amount does Athletic Supply report its available-for-sale securities on its balance sheets for 2016 and 2015?

B. How does Athletic Supply account for its trading securities? How does the accounting differ from their accounting method for available-for-sale?

C. What are the net unrealized gains (losses) for 2016 and 2015? How did these unrealized gains (losses) affect the company's reported income in 2016 and 2015?

D. What is the difference between realized and unrealized gains and losses? Are realized gains and losses treated differently in the income statement than unrealized gains and losses for the available-for-sale securities?

A. Available-for-sale securities are reported at fair value on the balance sheet. Thus, Athletic Supply's available-for-sale investments are reported at: $402,392 million as of 2016 and $225,172 million as of 2015.

B. Like available-for-sale securities, trading securities are reported at fair value on the balance sheet. Unlike available-for-sale securities, the unrealized gains or losses on trading securities would be reported in the income statement.

C. Net unrealized gains for 2016 are $24,794 million ($33,440 million gains - $8,646 million losses).

Net unrealized losses for 2015 are $(19,830) million ($72 million - $19,902 million).

These unrealized losses correspond to the available-for-sale portfolio so they bypass the income statement and are reported directly in the balance sheet.

D. Unrealized gains and losses occur when the stock increases or decreases in value after the investor buys the stock (i.e. "paper profits"). Realized gains and losses occur when the investor sells the stock. For available-for-sales securities, unrealized gains and losses flow through other comprehensive income in the equity section of the balance sheet (i.e. no income statement effects). When available-for-sale securities are sold (assuming there is a gain), other comprehensive income is reduced and a gain is realized in the income statement.

GAAP identifies three levels of influence/control. Which level of influence/control would a company use if it was investing in a company that gave it 15% of the outstanding voting stock?

A

An investor company can be considered to have control over the investee company even if it owns less than 50% of the outstanding voting stock of the investee company.

Financial statements of investee and investor companies can only be consolidated if both companies use the same accounting principles.

When a passive investment is sold, the gain (loss) is typically reported in "other" income.

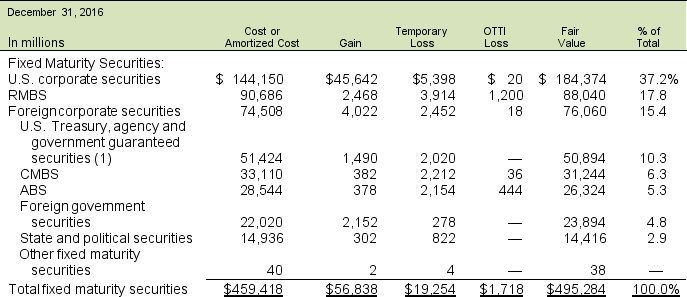

Following is a portion of the investments footnote from Red Barron Life Insurance's 2016 annual report. Investment earnings are a crucial component of the financial performance of insurance companies such as Red Barron Life Insurance, and investments comprise a large part of Red Barron's assets. Red Barron accounts for its bond investments as available-for-sale securities.

A. What amount does Red Barron report for bond investments on its balance sheets for 2016?

B. What are the net unrealized gains (losses) for 2016? How did these unrealized gains (losses) affect the company's reported income in 2016?

C. What is the difference between realized and unrealized gains and losses? Are realized gains and losses treated differently in the income statement than unrealized gains and losses?

A. What amount does Red Barron report for bond investments on its balance sheets for 2016?

B. What are the net unrealized gains (losses) for 2016? How did these unrealized gains (losses) affect the company's reported income in 2016?

C. What is the difference between realized and unrealized gains and losses? Are realized gains and losses treated differently in the income statement than unrealized gains and losses?

Which will be accounted for differently from GAAP under the proposed IFRS?

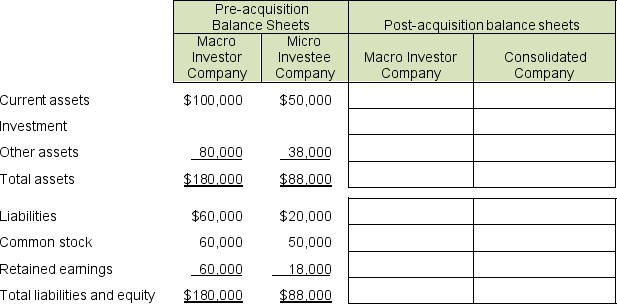

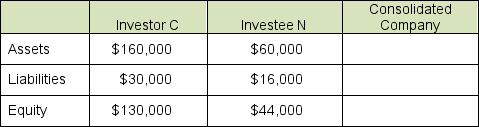

Consider companies with the pre-acquisition balance sheets presented below. Macro Investor Company purchases 100% of Micro Investee Company's stock at book value by exchanging newly issued common stock. Complete the columns for Investor's post-acquisition balance sheet and the Consolidated Company post-acquisition balance sheet.

Companies are required to disclose both qualitative and quantitative information about the potential risks underlying derivatives.

A. In general, what types of qualitative information must be disclosed?

B. Explain the reporting of quantitative information in financial statements that relates to derivatives.

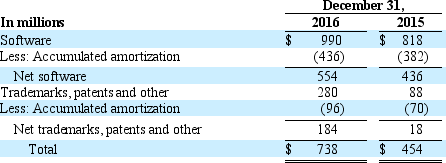

The following is from footnotes from the Mega Power, Inc. 2016 annual report (in millions):

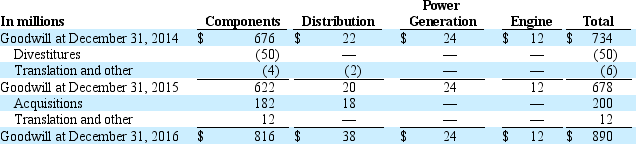

The following table summarizes the changes in the carrying amount of goodwill for 2016 and 2015:

Intangible assets that have finite useful lives are amortized over their estimated useful lives. The following table summarizes our other intangible assets with finite useful lives that are subject to amortization:

Intangible assets that have finite useful lives are amortized over their estimated useful lives. The following table summarizes our other intangible assets with finite useful lives that are subject to amortization:

Amortization expense for software and other intangibles totaled $128 million, $114 million and $138 million for the years ended December 31, 2016, 2015, and 2014, respectively. Internal and external software costs (excluding those related to research, re-engineering and training), trademarks and patents are amortized generally over a three to 12 year period. The following table represents the projected amortization expense of our intangible assets, assuming no further acquisitions or dispositions.

Amortization expense for software and other intangibles totaled $128 million, $114 million and $138 million for the years ended December 31, 2016, 2015, and 2014, respectively. Internal and external software costs (excluding those related to research, re-engineering and training), trademarks and patents are amortized generally over a three to 12 year period. The following table represents the projected amortization expense of our intangible assets, assuming no further acquisitions or dispositions.

Under GAAP for goodwill, we have the option to first assess qualitative factors to determine whether it is more likely than not that the fair value of a reporting unit is less than its carrying value as a basis for determining whether it is necessary to perform an annual two-step goodwill impairment test. The two-step impairment test is now only required if an entity determines through this qualitative analysis that it is more likely than not that the fair value of the reporting unit is less than its carrying value. In addition, carrying value of goodwill must be tested for impairment on an interim basis in certain circumstances where impairment may be indicated. When we are required or opt to perform the two-step impairment test, the fair value of each reporting unit is estimated by discounting the after tax future cash flows less requirements for working capital and fixed asset additions. Our reporting units are generally defined as one level below an operating segment. However, there were two situations where we have aggregated two or more components which share similar economic characteristics and thus are aggregated into a single reporting unit for testing purposes. These two situations are described further below. This analysis has resulted in the following reporting units for our goodwill testing:

●Within our Components segment, emission solutions and filtration have been aggregated into a single reporting unit.

●Also within our Components segment, our turbo technologies business is considered a separate reporting unit.

●Within our Power Generation segment, our generator technologies business is considered a separate reporting unit.

●Within our Engine segment, our new and recon parts business is considered a separate reporting unit. This reporting unit is in the business of selling new parts and remanufacturing and reconditioning engines and certain engine components.

●Our Distribution segment is considered a single reporting unit as it is managed geographically and all regions share similar economic characteristics and provide similar products and services.

No other reporting units have goodwill. Our valuation method requires us to make projections of revenue, operating expenses, working capital investment and fixed asset additions for the reporting units over a multi-year period. Additionally, management must estimate a weighted-average cost of capital, which reflects a market rate, for each reporting unit for use as a discount rate. The discounted cash flows are compared to the carrying value of the reporting unit and, if less than the carrying value, a separate valuation of the goodwill is required to determine if an impairment loss has occurred. In addition, we also perform a sensitivity analysis to determine how much our forecasts can fluctuate before the fair value of a reporting unit would be lower than its carrying amount. We performed the required procedures as of the end of our fiscal third quarter and determined that our goodwill was not impaired. At December 31, 2016, our recorded goodwill was $890 million, approximately 90 percent of which resided in the emission solutions plus filtration reporting unit. For this reporting unit, the fair value of the reporting unit exceeded its carrying value by a substantial margin. Changes in our projections or estimates, a deterioration of our operating results and the related cash flow effect or a significant increase in the discount rate could decrease the estimated fair value of our reporting units and result in a future impairment of goodwill.

A. How much goodwill did Mega Power, Inc. report on its 2016 balance sheet? How much accumulated amortization was included in that amount? Explain.

B. How much impairment charge relating to goodwill did Mega Power, Inc. report in 2016 and what was the reason for this?

C. What was the value of intangible assets on Mega Power, Inc.'s 2016 balance sheet? How much accumulated amortization was included in that amount?

Under GAAP for goodwill, we have the option to first assess qualitative factors to determine whether it is more likely than not that the fair value of a reporting unit is less than its carrying value as a basis for determining whether it is necessary to perform an annual two-step goodwill impairment test. The two-step impairment test is now only required if an entity determines through this qualitative analysis that it is more likely than not that the fair value of the reporting unit is less than its carrying value. In addition, carrying value of goodwill must be tested for impairment on an interim basis in certain circumstances where impairment may be indicated. When we are required or opt to perform the two-step impairment test, the fair value of each reporting unit is estimated by discounting the after tax future cash flows less requirements for working capital and fixed asset additions. Our reporting units are generally defined as one level below an operating segment. However, there were two situations where we have aggregated two or more components which share similar economic characteristics and thus are aggregated into a single reporting unit for testing purposes. These two situations are described further below. This analysis has resulted in the following reporting units for our goodwill testing:

●Within our Components segment, emission solutions and filtration have been aggregated into a single reporting unit.

●Also within our Components segment, our turbo technologies business is considered a separate reporting unit.

●Within our Power Generation segment, our generator technologies business is considered a separate reporting unit.

●Within our Engine segment, our new and recon parts business is considered a separate reporting unit. This reporting unit is in the business of selling new parts and remanufacturing and reconditioning engines and certain engine components.

●Our Distribution segment is considered a single reporting unit as it is managed geographically and all regions share similar economic characteristics and provide similar products and services.

No other reporting units have goodwill. Our valuation method requires us to make projections of revenue, operating expenses, working capital investment and fixed asset additions for the reporting units over a multi-year period. Additionally, management must estimate a weighted-average cost of capital, which reflects a market rate, for each reporting unit for use as a discount rate. The discounted cash flows are compared to the carrying value of the reporting unit and, if less than the carrying value, a separate valuation of the goodwill is required to determine if an impairment loss has occurred. In addition, we also perform a sensitivity analysis to determine how much our forecasts can fluctuate before the fair value of a reporting unit would be lower than its carrying amount. We performed the required procedures as of the end of our fiscal third quarter and determined that our goodwill was not impaired. At December 31, 2016, our recorded goodwill was $890 million, approximately 90 percent of which resided in the emission solutions plus filtration reporting unit. For this reporting unit, the fair value of the reporting unit exceeded its carrying value by a substantial margin. Changes in our projections or estimates, a deterioration of our operating results and the related cash flow effect or a significant increase in the discount rate could decrease the estimated fair value of our reporting units and result in a future impairment of goodwill.

A. How much goodwill did Mega Power, Inc. report on its 2016 balance sheet? How much accumulated amortization was included in that amount? Explain.

B. How much impairment charge relating to goodwill did Mega Power, Inc. report in 2016 and what was the reason for this?

C. What was the value of intangible assets on Mega Power, Inc.'s 2016 balance sheet? How much accumulated amortization was included in that amount?

Truck Company purchases an investment in Equipment Products, Inc. at a purchase price of $900,000, representing 15% of the book value of Equipment Products. During the year, Equipment Products reports a net income of $300,000 and pays cash dividends of $80,000. The fair value of Truck Company's investment at the end of the year is $1,600,000.

A. Using the fair value method, at what amount is the investment account reported at the end of the year?

B. How would fair value changes be treated if the marketable securities are classified as available-for-sale investments?

C. How would fair value changes be treated if the marketable securities are classified as trading investments?

D. How are dividends and gains/losses on security sales treated for trading and available-for-sale securities?

Which of the following statements is not correct concerning the effects on the components of return on equity (ROE) under equity method accounting?

On January 1, Barnyard Corporation acquired common stock of Fresh Hay Corporation. At the time of acquisition, the book value and the fair value of Fresh Hay Corporation's net assets were $1 billion. During the year, Fresh Hay Corporation earned $480 million and declared dividends of $160 million. The fair value of the shares increased by 10 percent during the year.

How much income would Barnyard Corporation report for the year related to its investment under the assumption that it:

A. Paid $150 million for 15 percent of the common stock and uses the fair value method (classified as available-for-sale) to account for its investment in Fresh Hay Corporation.

B. Paid $300 million for 30 percent of the common stock and uses the equity method to account for its investment in Fresh Hay Corporation.

Investor C has $160,000 in assets (including the investment in Investee N), $30,000 in liabilities, and $130,000 in equity. Investor C purchased 100% of Investee N, which has $60,000 in assets, $16,000 in liabilities, and $44,000 in equity on the date of acquisition.

What will the assets, liabilities, and equity be on the consolidated balance sheet immediately following the acquisition?

Brahtz Brothers owns 100% of Schweinfurt Company. At year-end, Schweinfurt owes Brahtz Brothers $52,000. If a consolidated balance sheet is prepared at year-end, how is the $52,000 handled?

Which of the following is not an example of the ability to exercise significant influence over an investee?

Which of the following statements is true in regards to the cost method?

Which of the following is correct about goodwill impairment?

Refuse Disposal Inc. reports the following in the 2016 Form 10-K (in millions):

A. Why does Refuse Disposal's income statement deduct its share of net losses of the unconsolidated entities?

B. Explain the reconciling item on Refuse Disposal's statement of cash flow that adds back equity in net losses of unconsolidated entities.

A. Why does Refuse Disposal's income statement deduct its share of net losses of the unconsolidated entities?

B. Explain the reconciling item on Refuse Disposal's statement of cash flow that adds back equity in net losses of unconsolidated entities.

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)