Exam 4: Consolidated Financial Statements Subsequent to Acquisition

Exam 1: Intercorporate Investments: An Overview110 Questions

Exam 2: Mergers and Acquisitions115 Questions

Exam 3: Consolidated Financial Statements: Date of Acquisition110 Questions

Exam 4: Consolidated Financial Statements Subsequent to Acquisition115 Questions

Exam 5: Consolidated Financial Statements: Outside Interests114 Questions

Exam 6: Consolidated Financial Statements: Intercompany Transactions109 Questions

Exam 7: Consolidating Foreign Currency Financial Statements110 Questions

Exam 8: Foreign Currency Transactions and Hedging110 Questions

Exam 9: Futures, Options and Interest Rate Swaps110 Questions

Exam 10: State and Local Governments: Introduction and General Fund Transactions190 Questions

Exam 11: State and Local Governments: Other Transactions110 Questions

Exam 12: State and Local Governments: External Financial Reporting144 Questions

Exam 13: Private Not-For-Profit Organizations128 Questions

Exam 14: Partnership Accounting and Reporting109 Questions

Exam 15: Bankruptcy and Reorganization110 Questions

Exam 16: The Sec and Financial Reporting114 Questions

Select questions type

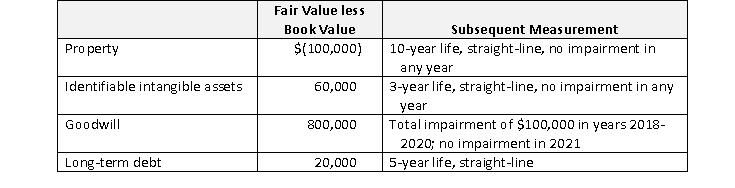

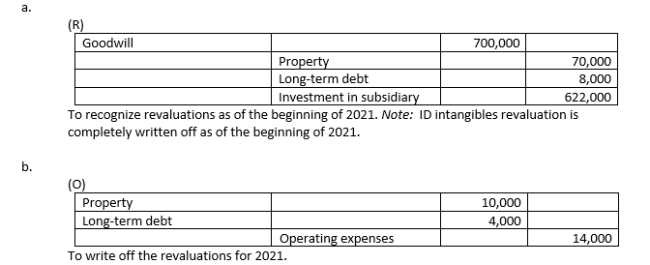

A parent acquired the voting stock of its subsidiary on January 1, 2018. The excess of acquisition cost over the subsidiary's book value was allocated as indicated in the table below.

It is now December 31, 2021, the fourth year since acquisition.

Required

a. Prepare eliminating entry (R) on the December 31, 2021 consolidation working paper.

b. Prepare eliminating entry (O) on the December 31, 2021 consolidation working paper. Use "operating expenses" for any adjustments to depreciation, amortization, impairment losses, or interest expense.

It is now December 31, 2021, the fourth year since acquisition.

Required

a. Prepare eliminating entry (R) on the December 31, 2021 consolidation working paper.

b. Prepare eliminating entry (O) on the December 31, 2021 consolidation working paper. Use "operating expenses" for any adjustments to depreciation, amortization, impairment losses, or interest expense.

Free

(Essay)

4.7/5  (41)

(41)

Correct Answer: Verified

Verified

An acquisition requires revaluation of a subsidiary's date-of-acquisition plant assets from a book value of $40 million to a fair value of $25 million. The plant assets have a 10-year remaining life at the date of acquisition. Which statement is true concerning the eliminating entries for this revaluation?

Free

(Multiple Choice)

4.9/5 (29)

Correct Answer:Verified

A

Use the following information to answer bellow Questions:

A subsidiary is acquired on January 1, 2019 for $10,000. The subsidiary's book value at the date of acquisition was $2,000. Following is revaluation information for the subsidiary's identifiable net assets at the date of acquisition:

Fair Value - Book Value \cline 2-3 Inventories \ (200\} FIFO, sold in 2019 Identifiable int angibles 5,000 Straight-line, 5 years Long term debt 300 Straight-line, 2 years Goodwill recognized in the acquisition was unimpaired in 2019 but became fully impaired during 2020. The subsidiary did not declare any dividends during this period and reported no other comprehensive income. The subsidiary reported net income as follows:

Year Net Income 2019 \ 1,500 2020 5,000 2021 2,000 The parent uses the complete equity method to report its investment on its own books.

-Equity in net income (loss) for 2020, reported on the parent's books, is:

Free

(Multiple Choice)

4.8/5 (42)

Correct Answer:Verified

A

Prism Corporation acquires the voting stock of Streetspace Inc. on January 1, 2020, for $100,000 in cash. Streetspace's book value at the date of acquisition was:

All of Streetspace's recorded assets and liabilities are carried at fair value, but it has previously unrecorded customer-related intangible assets valued at $28,000 that are capitalizable under the requirements of ASC Topic 805. These intangibles have an estimated life of 5 years, straight-line. Streetspace reports net income of $8,400 and other comprehensive income of $25 for 2020, and declares and pays dividends of $1,000. It is determined through impairment testing that acquired goodwill is impaired by $500 and the customer-related intangible assets are not impaired. Prism uses the complete equity method to account for its investment in Streetspace on its own books.

Required

a. Calculate the amount Prism reports for 2020 as equity in net income of Streetspace on its own books.

b. Present, in journal entry form, the four eliminating entries needed to consolidate the trial balances of Prism and Streetspace at December 31, 2020. Revaluation write-offs are adjustments to operating expenses.

All of Streetspace's recorded assets and liabilities are carried at fair value, but it has previously unrecorded customer-related intangible assets valued at $28,000 that are capitalizable under the requirements of ASC Topic 805. These intangibles have an estimated life of 5 years, straight-line. Streetspace reports net income of $8,400 and other comprehensive income of $25 for 2020, and declares and pays dividends of $1,000. It is determined through impairment testing that acquired goodwill is impaired by $500 and the customer-related intangible assets are not impaired. Prism uses the complete equity method to account for its investment in Streetspace on its own books.

Required

a. Calculate the amount Prism reports for 2020 as equity in net income of Streetspace on its own books.

b. Present, in journal entry form, the four eliminating entries needed to consolidate the trial balances of Prism and Streetspace at December 31, 2020. Revaluation write-offs are adjustments to operating expenses.

(Essay)

4.8/5 (37)

A company reports total goodwill of $4,000. On December 31, 2020, the following information is available for the reporting units of a company:

North American Division International Division Book value of goodwill \ 1,000 \ 3,000 Fair value of division 8,000 6,000 Book value of division 8,700 5,800 Required

a. Management determines that it is more likely than not that book value exceeds fair value for both reporting units. What is the amount of goodwill impairment loss for 2020, following U.S. GAAP?

b. Now assume the company follows IFRS and allocates the $4,000 in goodwill to the following cash generating units.

(Essay)

4.9/5 (41)

Use the following information to answer Questions bellow.

Potash Corporation acquired the voting stock of Safestyle Company on January 1, 2019 for $50 million. Safestyle's book value at the time was $10 million, consisting of $2 million of capital stock and $8 million of retained earnings. The $40 million difference between fair and book value was attributed to goodwill. It is now December 31, 2020, the end of the accounting year and two years after the acquisition. Safestyle's January 1, 2020 retained earnings balance is $11 million, and it reports net income of $1.8 million for 2020. Safestyle declares no dividends and has no other comprehensive income. Goodwill from the acquisition was impaired by $1 million in 2019 and $500,000 in 2020. Potash uses the complete equity method to report its investment in Safestyle on its own books.

-What is the December 31, 2020 balance for Investment in Safestyle, reported on Potash's books?

(Multiple Choice)

4.7/5 (34)

A parent company acquires all of a subsidiary's voting stock at the beginning of 2018. At the date of acquisition, the subsidiary's equipment had a book value of $40 million and a fair value of $25 million. The equipment had a 10-year remaining life, straight-line. Consolidation eliminating entry (R), on the consolidation working paper for 2021, reduces the net equipment account by what amount?

(Multiple Choice)

4.8/5 (36)

Use the following information to answer bellow Questions:

On January 1, 2018, Pearson Company acquired all of Sundisk Company's voting stock for $20,000 in cash. Sundisk's total shareholders' equity at January 1, 2018 was $5,000. Some of Sundisk's assets and liabilities at the date of acquisition had fair values that were different from reported values, as follows:

Book Value Fair Value Plant assets, net (10 years, straight-line) \ 15,000 \ 10,000 Identifiable intangibles (indefinite life) 0 9,000

It is now December 31, 2020 (3 years later). Impairment of recognized identifiable intangibles totals $400 for 2018 and 2019, and there is no impairment in 2020. There is no goodwill impairment as of the beginning of 2020, but goodwill impairment for 2020 is $1,200. Pearson uses the complete equity method to account for its investment. December 31, 2020 trial balances for Pearson and Sundisk follow:

Pearson Sund isk Dr () Dr () Current assets \ 5,000 \ 2,500 Plant assets, net 28,700 22,000 Identifiable intangibles - - Investment in Sundisk 28,400 - Goodwill - - Liabilities \{20,300\} \{11,000\} Capital stock \{15,000\} \{2,000\} Retained earnings, beginning \{25,000\} \{10,000\} Sales revenue \{25,000\} \{14,000\} Equity in net income of Sundisk \{800\} - Cost of goods sold 20,000 9,000 Operating expenses 4,000 3,500 \0 \0 The following questions relate to consolidation eliminating entries for 2020.

-Eliminating entry (R):

(Multiple Choice)

4.7/5 (32)

An IFRS company reports $25,000 in goodwill and decides to quantitatively test it for impairment at the end of 2020. The following information is collected:

CGU 1 CGU 2 CGU 3 Book value of goodwill \ 2,000 \ 9,000 \ 14,000 Fair value of CGU 10,000 25,000 55,000 Book value of CGU 8,500 30,000 75,000 Which statement is true, following IFRS?

(Multiple Choice)

4.9/5 (33)

A subsidiary has plant assets with a fair value of $70 million and book value of $60 million at the date of acquisition. The plant assets have a remaining life, as of the date of acquisition, of 20 years, straight-line. You are consolidating the accounts at the end of the third year since acquisition, and the subsidiary still owns the plant assets. The amount by which the plant assets are revalued in eliminating entry (R) is:

(Multiple Choice)

4.9/5 (40)

On consolidated financial statements, where does the parent's equity in the net income of the subsidiary account appear?

(Multiple Choice)

4.7/5 (28)

When consolidating the accounts of a parent and subsidiary in subsequent years, eliminating entry (O) recognizes total write-offs of subsidiary revaluations:

(Multiple Choice)

4.7/5 (31)

A subsidiary is acquired on January 1, 2020 for $20 million in cash. The subsidiary's book value at the date of acquisition was $3 million. Following is revaluation information for the subsidiary's identifiable net assets at the date of acquisition:

Fair Value - Book Value Identifiable intangibles \ 1,000,000 Straight-line, 5 years Long-term debt (100,000) Straight-line, 4 years During 2020, the subsidiary reported net income of $1.2 million, and other comprehensive income of $25,000. There are no revaluation impairments in 2020. The parent uses the complete equity method to report its investment on its own books.

Required

a. Calculate equity in net income for 2020, reported on the parent's books.

b. Prepare the parent's entries to account for the investment during 2020.

c. What is the December 31, 2020 balance in the investment account, reported on the parent's books?

(Essay)

4.9/5 (47)

Use the following information to answer Questions bellow.

Potash Corporation acquired the voting stock of Safestyle Company on January 1, 2019 for $50 million. Safestyle's book value at the time was $10 million, consisting of $2 million of capital stock and $8 million of retained earnings. The $40 million difference between fair and book value was attributed to goodwill. It is now December 31, 2020, the end of the accounting year and two years after the acquisition. Safestyle's January 1, 2020 retained earnings balance is $11 million, and it reports net income of $1.8 million for 2020. Safestyle declares no dividends and has no other comprehensive income. Goodwill from the acquisition was impaired by $1 million in 2019 and $500,000 in 2020. Potash uses the complete equity method to report its investment in Safestyle on its own books.

-On the December 31, 2020 consolidation working paper, eliminating entry (E) credits the Investment in Safestyle account by:

(Multiple Choice)

4.9/5 (36)

Photec Corporation acquires the voting stock of Solarcentury Inc. on January 1, 2020. In preparing to consolidate the trial balances of Photec and Solarcentury at December 31, 2021 (two years after the acquisition), you assemble the following information:

Date-of-acquisition information:

1) Value of stock issued to Solarcentury shareholders: $99,000.

2) Direct merger costs: $800 and stock registration fees, $350, all paid in cash.

3) Solarcentury shareholders' equity: $23,500, consisting of capital stock, $5,000; retained earnings, $18,000; accumulated other comprehensive income, $500.

4) Fair value of earnings contingency agreement to be paid in cash: $1,000.

5) Fair value of previously unrecorded identifiable intangibles (5-year life): $25,000. There are no revaluations of Solarcentury's reported net assets.

Information for 2020 and 2021:

6) Solarcentury's reported net income for 2020: $8,000; for 2021: $6,500.

7) Solarcentury's reported other comprehensive income for 2020: $75 gain; for 2021: $125 loss.

8) Solarcentury declared and paid dividends of $300 each year.

9) Goodwill and identifiable intangibles are not impaired in 2020; goodwill is impaired by $700 in 2021.

Required

a. Prepare the 2020 and 2021 journal entries made by Photec to record its investment, using the complete equity method.

b. Prepare the consolidation eliminating entries made at December 31, 2021.

(Essay)

4.8/5 (35)

Powerplan Industries bought Springfield Inc.'s voting stock on January 1, 2019 for $42,000, when Springfield's book value was $8,000. Fair value information on Springfield's assets and liabilities at the date of acquisition is as follows:

•Property and equipment is overvalued by $7,000. P&E has a 10-year remaining life, straight-line.

•Previously unreported identifiable intangibles are valued at $8,000. These intangibles have indefinite lives, but testing reveals impairment of $2,000 in 2019 and $1,000 impairment in 2020.

•Goodwill reported for this acquisition is not impaired in 2019, but is impaired by $3,000 in 2020.

Powerplan uses the complete equity method to account for its investment in Springfield on its own books. It is now December 31, 2020, two years since the acquisition. The consolidation working paper at December 31, 2020, with the separate trial balances of Powerplan and Springfield, follows.

Powerplan Dr (Cr) Springfield Dr () Dr Consol () Current assets \ 15,000 \ 10,000 Property \& equipment, net 90,000 63,000 Identifiable intangibles - Investment in Springfield 44,900 - Goodwill - - Liabilities (76,200) (57,500) Capital stock (40,000) (5,000) Retained earnings, Jan. 1 (30,000) (6,100) Treasury stock 2,000 100 Dividends - 500 Sales revenue (84,000) (50,000) Equity in NI of Springfield (1,700) - Cost of goods sold 55,000 30,000 Operating expenses 25,000 15,000 Total \0 \0

Required

a. Prepare a schedule calculating the initial value of goodwill for this acquisition.

b. Calculate Powerplan's equity in net income of Springfield for 2020.

c. Fill in the consolidation working paper as necessary to consolidate the trial balances of the two companies at December 31, 2020.

(Essay)

4.7/5 (41)

A subsidiary is acquired on January 1, 2019 at an acquisition cost of $100 million. The subsidiary's book value at the date of acquisition was $25 million, consisting of these accounts:

Capital stock \ 8,000,000 Retained earnings 18,000,000 Accumulated other comprehensive loss (1,000,000) Following is revaluation information for the subsidiary's identifiable net assets at the date of acquisition:

Fair Value Book Value Plant assets, net \ 25,000,000 \ 40,000,000 Straight-line, 5 years Identifiable intangible assets 60,000,000 0 Straight-line, 6 years It is now December 31, 2021, three years since the acquisition. The subsidiary reported the following amounts during the period 2019 - 2021:

Net income \ 12,000,000 \ 10,000,000 \ 15,000,000 Other comprehensive income( loss) 300,000 \{160,000\} 125,000 The subsidiary did not declare any dividends during this period. Goodwill for this acquisition is not impaired as of the end of 2021. The parent uses the complete equity method to report its investment on its own books.

Required

a. Calculate equity in net income, reported on the parent's books, for 2021.

b. Prepare the parent's entry or entries to account for the investment during 2021.

c. What is the December 31, 2021 balance in the investment account, reported on the parent's books?

(Essay)

4.9/5 (38)

Assume a U.S. company decides to quantitatively test its goodwill for impairment. A division's book value exceeds its fair value by $8 million, and its goodwill has a book value of $6 million. The division's goodwill impairment loss is

(Multiple Choice)

4.7/5 (36)

Following U.S. GAAP, goodwill acquired in a merger must be allocated to business units before it can be tested for impairment. How are these "business units" defined?

(Multiple Choice)

4.9/5 (33)

P Corporation acquires all of S Company's voting stock. At the date of acquisition, the fair value of S Company's long-term debt is $100 greater than its book value. The debt has a 5-year remaining life at the date of acquisition. When consolidating S Company's financial statements for the first year following acquisition, how will eliminating entry (O) affect long-term debt and interest expense?

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)