Exam 4: Consolidated Financial Statements Subsequent to Acquisition

Exam 1: Intercorporate Investments: An Overview110 Questions

Exam 2: Mergers and Acquisitions115 Questions

Exam 3: Consolidated Financial Statements: Date of Acquisition110 Questions

Exam 4: Consolidated Financial Statements Subsequent to Acquisition115 Questions

Exam 5: Consolidated Financial Statements: Outside Interests114 Questions

Exam 6: Consolidated Financial Statements: Intercompany Transactions109 Questions

Exam 7: Consolidating Foreign Currency Financial Statements110 Questions

Exam 8: Foreign Currency Transactions and Hedging110 Questions

Exam 9: Futures, Options and Interest Rate Swaps110 Questions

Exam 10: State and Local Governments: Introduction and General Fund Transactions190 Questions

Exam 11: State and Local Governments: Other Transactions110 Questions

Exam 12: State and Local Governments: External Financial Reporting144 Questions

Exam 13: Private Not-For-Profit Organizations128 Questions

Exam 14: Partnership Accounting and Reporting109 Questions

Exam 15: Bankruptcy and Reorganization110 Questions

Exam 16: The Sec and Financial Reporting114 Questions

Select questions type

Mojo Corporation acquires all the voting stock of Ninja Company. Ninja has $1,000,000 in bonds payable, issued at par value, on its books. The bonds have a 5-year remaining life at the date of acquisition, and 4% interest is paid annually. The fair value of the bonds at the date of acquisition is $1,020,000. The premium is straight-line amortized. Which statement is true concerning the consolidation of Mojo with Ninja two years after the acquisition?

(Multiple Choice)

4.8/5  (40)

(40)

An acquisition requires revaluation of a subsidiary's date-of-acquisition inventory from a book value of $5 million to fair value of $3 million. The subsidiary uses FIFO and sells the inventory in the first year following acquisition. Which statement is true concerning the consolidation eliminating entries for this revaluation?

(Multiple Choice)

4.8/5 (35)

Which statement is true concerning impairment testing of identifiable intangible assets, following U.S. GAAP?

(Multiple Choice)

4.9/5 (30)

Use the following information to answer bellow Questions:

A subsidiary is acquired on January 1, 2019 for $10,000. The subsidiary's book value at the date of acquisition was $2,000. Following is revaluation information for the subsidiary's identifiable net assets at the date of acquisition:

Fair Value - Book Value \cline 2-3 Inventories \ (200\} FIFO, sold in 2019 Identifiable int angibles 5,000 Straight-line, 5 years Long term debt 300 Straight-line, 2 years Goodwill recognized in the acquisition was unimpaired in 2019 but became fully impaired during 2020. The subsidiary did not declare any dividends during this period and reported no other comprehensive income. The subsidiary reported net income as follows:

Year Net Income 2019 \ 1,500 2020 5,000 2021 2,000 The parent uses the complete equity method to report its investment on its own books.

-Equity in net income for 2019, reported on the parent's books, is:

(Multiple Choice)

4.9/5 (19)

Use the following information to answer bellow Questions:

On January 1, 2018, Pearson Company acquired all of Sundisk Company's voting stock for $20,000 in cash. Sundisk's total shareholders' equity at January 1, 2018 was $5,000. Some of Sundisk's assets and liabilities at the date of acquisition had fair values that were different from reported values, as follows:

Book Value Fair Value Plant assets, net (10 years, straight-line) \ 15,000 \ 10,000 Identifiable intangibles (indefinite life) 0 9,000

It is now December 31, 2020 (3 years later). Impairment of recognized identifiable intangibles totals $400 for 2018 and 2019, and there is no impairment in 2020. There is no goodwill impairment as of the beginning of 2020, but goodwill impairment for 2020 is $1,200. Pearson uses the complete equity method to account for its investment. December 31, 2020 trial balances for Pearson and Sundisk follow:

Pearson Sund isk Dr () Dr () Current assets \ 5,000 \ 2,500 Plant assets, net 28,700 22,000 Identifiable intangibles - - Investment in Sundisk 28,400 - Goodwill - - Liabilities \{20,300\} \{11,000\} Capital stock \{15,000\} \{2,000\} Retained earnings, beginning \{25,000\} \{10,000\} Sales revenue \{25,000\} \{14,000\} Equity in net income of Sundisk \{800\} - Cost of goods sold 20,000 9,000 Operating expenses 4,000 3,500 \0 \0 The following questions relate to consolidation eliminating entries for 2020.

-Eliminating entry (E) credits Investment in Sundisk in the amount of:

(Multiple Choice)

4.7/5 (29)

A wholly-owned subsidiary's revalued net assets at the date of acquisition consist of indefinite life identifiable intangible assets valued at $500,000 at the date of acquisition. Impairment of these intangibles as of the beginning of the current year is $50,000, and impairment testing for the current year reveals $200,000 in additional impairment on these intangibles. Consolidation eliminating entry (O) at the end of the current year reduces identifiable intangible assets by:

(Multiple Choice)

4.9/5 (34)

A subsidiary still holds all net assets revalued at the date of acquisition. Which working paper eliminating entry below is most likely to be the same whether the consolidation takes place at the date of acquisition or in subsequent years?

(Multiple Choice)

4.8/5 (37)

Which of the following is not a possible reason why IFRS companies may report more goodwill impairment losses than U.S. GAAP companies?

(Multiple Choice)

4.9/5 (34)

Use the following information to answer bellow Questions:

Park Corporation acquired the voting stock of Sequoia Company on January 1, 2020 for $25 million in cash and stock. At the date of acquisition, Sequoia's book value totaled $3 million, consisting of $1.6 million in capital stock, $1.8 million in retained earnings, and $400,000 in accumulated other comprehensive losses.

Sequoia's reported net assets at the date of acquisition were carried at amounts approximating fair value, except its inventory was overvalued by $500,000 (sold in 2020), its plant assets (10-year life, straight-line) were overvalued by $3,500,000, and its long-term debt (premium amortized over 10 years, straight-line) is undervalued by $100,000. Sequoia also had previously unreported identifiable intangibles (5-year life, straight-line) valued at $5,000,000.

It is now December 31, 2020. Sequoia reports net income of $1,200,000 and other comprehensive income of $50,000 for 2020 and declares and pays dividends of $200,000. None of the revaluations are impaired in 2020. Park uses the complete equity method to account for its investment.

-The balance for acquired identifiable intangibles on the December 31, 2020 consolidated balance sheet is:

(Multiple Choice)

4.8/5 (43)

A company uses IFRS and chooses to report certain generic intangible assets at fair value. On January 1, 2019, it acquires software for €100,000, with an estimated life of 4 years, straight-line. On December 31, 2019, the intangible has a fair value of €110,000. How is this change in value reported on the 2019 financial statements?

(Multiple Choice)

4.7/5 (45)

A company reports $11.2 million in goodwill and decides to quantitatively test it for impairment at the end of 2020. The following information is collected:

Division 1 Division 2 Division 3 Book value of goodwill \ 7,000,000 \ 200,000 \ 4,000,000 Fair value of division 40,000,000 6,000,000 20,000,000 Book value of division 45,000,000 6,500,000 21,000,000 What is the amount of goodwill impairment loss for 2020, following U.S. GAAP?

(Multiple Choice)

4.9/5 (30)

The interest rate at which an acquired company issued its long-term bonds payable is higher than the current market rate. The bonds have a four-year remaining life at the date of acquisition. Which statement is true concerning the write-off of revaluation of these bonds in the fourth year after acquisition (eliminating entry O)?

(Multiple Choice)

4.9/5 (28)

Which statement is true regarding the U.S. GAAP impairment test for limited life intangibles?

(Multiple Choice)

4.8/5 (38)

At the date of acquisition, a subsidiary's inventory (LIFO, still held by the subsidiary) is overvalued by $600, its plant assets (10-year life, straight-line) are overvalued by $4,000, and it has previously unreported intangibles valued at $1,000 (2-year life, straight-line). Goodwill from the acquisition is not impaired. In the third year following acquisition, the subsidiary reports net income of $2,500. Using the complete equity method, in the third year the parent reports equity in the net income of the subsidiary of:

(Multiple Choice)

4.9/5 (42)

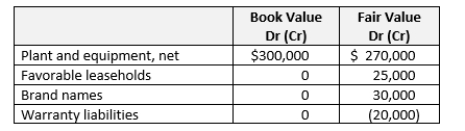

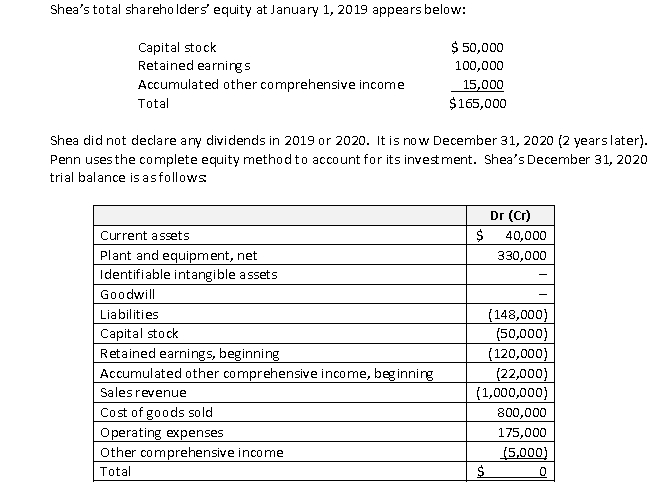

On January 1, 2019, Penn Corporation acquired the voting stock of Shea Company at an acquisition cost of $450,000. Some of Shea's assets and liabilities at the date of acquisition had fair values that were different from reported values, as follows:

At the date of acquisition, the plant and equipment had a 10-year remaining life, and the favorable leases had a 5-year remaining life, straight-line. The brand names are indefinite life assets. They were impaired by $3,000 in 2019, and were not impaired in 2020. Goodwill from this acquisition is not impaired as of the beginning of 2020, but goodwill impairment for 2020 is $1,000. Warranty payments connected with the revaluation liability were $500 in 2019 and $1,500 in 2020.

At the date of acquisition, the plant and equipment had a 10-year remaining life, and the favorable leases had a 5-year remaining life, straight-line. The brand names are indefinite life assets. They were impaired by $3,000 in 2019, and were not impaired in 2020. Goodwill from this acquisition is not impaired as of the beginning of 2020, but goodwill impairment for 2020 is $1,000. Warranty payments connected with the revaluation liability were $500 in 2019 and $1,500 in 2020.

Shea does not pay dividends.

Required

a. Calculate the goodwill recognized with this acquisition.

b. Calculate equity in net income for 2019 and 2020, reported on Penn's books.

c. Calculate the December 31, 2020 balance for Investment in Shea, reported on Penn's books.

d. Present consolidation eliminating entries (C), (E), (R) and (O) to consolidate the December 31, 2020 trial balances of Penn and Shea.

Shea does not pay dividends.

Required

a. Calculate the goodwill recognized with this acquisition.

b. Calculate equity in net income for 2019 and 2020, reported on Penn's books.

c. Calculate the December 31, 2020 balance for Investment in Shea, reported on Penn's books.

d. Present consolidation eliminating entries (C), (E), (R) and (O) to consolidate the December 31, 2020 trial balances of Penn and Shea.

(Essay)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)