Exam 1: Securities Markets, Efficient Diversification, Risk and Return: Past and Prologue

Exam 1: Securities Markets, Efficient Diversification, Risk and Return: Past and Prologue11 Questions

Exam 2: Capital Pricing, Arbitrage Pricing Theory, Bond Prices, Yields, Efficient Market Hypothesis and Behavioral Finance11 Questions

Exam 3: Equity Valuation, Managing Bond Portfolios, Macroeconomic and Industry Analysis9 Questions

Exam 4: Financial Statement Analysis, Options and Risk Management15 Questions

Exam 5: Hedge Funds, Futures, Risk Management, Investors and the Investment Process7 Questions

Exam 6: Portfolio Performance Evaluation9 Questions

Select questions type

You are considering investing $1000 in a complete portfolio. The complete portfolio is composed of Treasury notes that pay 5% and a risky portfolio, P, constructed with two risky securities X and Y. The optimal weights of X and Y in P are 60% and 40% respectively. X has an expected rate of return of 14% and Y has an expected rate of return of 10%. To form a complete portfolio with an expected rate of return of 8%, you should invest approximately ________ in the risky portfolio. This will mean you will also invest approximately ________ and ________ of your complete portfolio in security X and Y respectively.

Free

(Multiple Choice)

4.8/5  (30)

(30)

Correct Answer: Verified

Verified

C

You have an APR of 7.5% with continuous compounding. The EAR is ________.

Free

(Multiple Choice)

4.8/5 (40)

Correct Answer:Verified

C

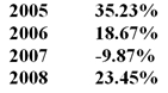

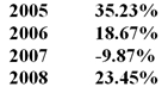

You have the following rates of return for a risky portfolio for several recent years: If you invested $1 000 at the beginning of 2005 your investment at the end of 2008 would be worth ________.

Free

(Multiple Choice)

4.8/5 (31)

Correct Answer:Verified

B

Based on the outcomes in the table below choose which of the statements is/are correct:

I. The covariance of Security A and Security B is zero

II. The correlation coefficient between Security A and C is negative

III. The correlation coefficient between Security B and C is positive

I. The covariance of Security A and Security B is zero

II. The correlation coefficient between Security A and C is negative

III. The correlation coefficient between Security B and C is positive

(Multiple Choice)

4.9/5 (32)

Consider the following limit order book of a specialist. The last trade in the share occurred at a price of $40.  If a market buy order for 100 shares comes in, at what price will it be filled?

If a market buy order for 100 shares comes in, at what price will it be filled?

(Multiple Choice)

4.9/5 (48)

Security A has a higher standard deviation of returns than Security B We would expect that ________.

I. Security A would have a higher risk premium than Security B

II. the likely range of returns for Security A in any given year would be higher than the likely range of returns for Security B

III. the Sharpe measure of A will be higher than the Sharpe measure of B.

(Multiple Choice)

4.8/5 (37)

If the bid price is $15.12 and the ask price is $15.14, the bid-ask spread is ________.

(Multiple Choice)

4.8/5 (41)

You have the following rates of return for a risky portfolio for several recent years: The annualised average return on this investment is ________.

(Multiple Choice)

4.8/5 (41)

Two assets have the following expected returns and standard deviations when the risk-free rate is 5%: An investor with a risk aversion of A = 3 would find that ________ on a risk-return basis.

(Multiple Choice)

4.9/5 (47)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)