Exam 15: Cost Allocation: Joint Products and Byproducts

Exam 1: The Accountants Vital Role in Decision Making33 Questions

Exam 2: An Introduction to Cost Terms and Purposes60 Questions

Exam 3: Cost-Volume-Profit Analysis41 Questions

Exam 4: Job Costing49 Questions

Exam 5: Activity-Based Costing and Management40 Questions

Exam 6: Master Budget and Responsibility Accounting50 Questions

Exam 7: Flexible Budgets, Variances, and Management Control: I47 Questions

Exam 8: Flexible Budgets, Variances, and Management Control: II35 Questions

Exam 9: Income Effects of Denominator Level on Inventory Valuation52 Questions

Exam 10: Analysis of Cost Behaviour80 Questions

Exam 11: Decision Making and Relevant Information54 Questions

Exam 12: Pricing Decisions, Product Profitability Decisions, and Cost Management36 Questions

Exam 13: Strategy, Balanced Scorecard, and Profitability Analysis43 Questions

Exam 14: Period Cost Allocation38 Questions

Exam 15: Cost Allocation: Joint Products and Byproducts57 Questions

Exam 16: Revenue and Customer Profitability Analysis29 Questions

Exam 17: Process Costing50 Questions

Exam 18: Spoilage, Rework, and Scrap62 Questions

Exam 19: Inventory Cost Management Strategies46 Questions

Exam 20: Capital Budgeting: Methods of Investment Analysis42 Questions

Exam 21: Transfer Pricing and Multinational Management Control Systems45 Questions

Exam 22: Multinational Performance Measurement and Compensation62 Questions

Select questions type

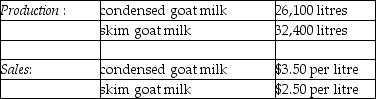

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

Direct Materials processed: 65,000 litres (shrinkage was 10%)

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-Using estimated net realizable value, what amount of the $72,240 of joint costs would be allocated Xyla and the skim goat ice cream?

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-Using estimated net realizable value, what amount of the $72,240 of joint costs would be allocated Xyla and the skim goat ice cream?

Free

(Multiple Choice)

4.7/5  (37)

(37)

Correct Answer: Verified

Verified

B

The Arvid Corporation manufactures widgets, gizmos, and turnbols from a joint process. May production is 4,000 widgets; 7,000 gizmos; and 8,000 turnbols. Respective per unit selling prices at splitoff are $15, $10, and $5. Joint costs up to the splitoff point are $75,000. If joint costs are allocated based upon the sales value at splitoff, what amount of joint costs will be allocated to the widgets?

Free

(Multiple Choice)

5.0/5 (30)

Correct Answer:Verified

B

Land and Sea Corporation processes frozen chicken. The company has not been pleased with its profit margin per product because it appears that the high value items have too few costs assigned to them while the low value items have too many costs assigned to them. The processing results in several products, the primary one of which is frozen small hens. Other products include frozen parts such as wings and legs, byproducts such as skin and bones, and unused scrap items.

Required:

What may be the cost assignment problem if a key consideration is the value of the products being sold?

Free

(Essay)

4.9/5 (36)

Correct Answer:Verified

First, the company needs to consider whether the byproducts are being treated as products, rather than byproducts. For the most part, byproducts should not be assigned costs. The revenue from the byproducts should be used as either minor sales categories or else as offsets to processing costs. A second consideration is the method used to assign the costs. It is possible that some physical measure (weight) is being used, in which case the parts items and the byproducts may weigh as much as the primary product. It may be necessary to evaluate the various methods of allocation and select the one with which management feels is best for decision making.

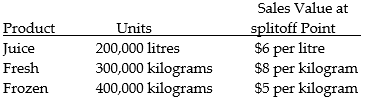

Peachland Fruit Ltd. harvests blueberries. After harvest, the company sells some berries fresh, freezes others, and processes some into juice. During the summer the joint costs of processing the berry products were $620,000. Any separable costs for each product are negligible and are not traced. There were no beginning or ending inventories for the summer. Production and sales value information for the summer were as follows:

Required:

Determine the amount allocated to each product if the sales value at splitoff method is used and compute the cost per case for each product.

Required:

Determine the amount allocated to each product if the sales value at splitoff method is used and compute the cost per case for each product.

(Essay)

4.9/5 (43)

Match each of the following costs with the appropriate joint production process cost classification.

-Skim milk from dairy processing

(Multiple Choice)

4.8/5 (38)

Use the information below to answer the following question(s).

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the NRV method, the amount of joint costs allocated to Kraxton is

(Multiple Choice)

4.9/5 (38)

Use the information below to answer the following question(s).

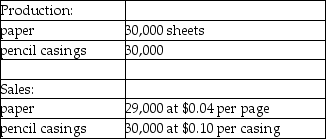

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the splitoff point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.

Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What are the paper's and the pencil's approximate weighted cost proportions using the sales value at splitoff method, respectively?

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.

Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What are the paper's and the pencil's approximate weighted cost proportions using the sales value at splitoff method, respectively?

(Multiple Choice)

4.9/5 (37)

Use the information below to answer the following questions:

Argon Manufacturing Company processes direct materials up to the splitoff point where two products (U and V) are obtained and sold. The following information was collected for last quarter of the calendar year:

The cost of purchasing 20,000 gallons of direct materials and processing it up to the splitoff point to yield a total of 19,000 gallons of good products was $1,950,000.

Beginning inventories totaled 100 gallons for U and 50 gallons for V. Ending inventory amounts reflected 600 gallons of Product U and 1,050 gallons of Product V. October costs per unit were the same as November.

-What are the physical-volume proportions for products U and V, respectively?

The cost of purchasing 20,000 gallons of direct materials and processing it up to the splitoff point to yield a total of 19,000 gallons of good products was $1,950,000.

Beginning inventories totaled 100 gallons for U and 50 gallons for V. Ending inventory amounts reflected 600 gallons of Product U and 1,050 gallons of Product V. October costs per unit were the same as November.

-What are the physical-volume proportions for products U and V, respectively?

(Multiple Choice)

4.8/5 (34)

Use the information below to answer the following question(s).

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the physical measures method, the joint costs allocated to Kharton would be

(Multiple Choice)

4.8/5 (37)

Which of the following is TRUE regarding the costs of toxic waste disposal, reclamation, and remediation that result from joint production processing?

(Multiple Choice)

4.7/5 (44)

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

Direct Materials processed: 65,000 litres (shrinkage was 10%)

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-What is the estimated net realizable value of Xyla at the splitoff point?

(Multiple Choice)

4.8/5 (30)

Match each of the following costs with the appropriate joint production process cost classification.

-Broth from cooking food

(Multiple Choice)

4.8/5 (42)

North York Statue Company makes miniature Mountie statues from cast iron. Sales total 40,000 units a year and the company is operating at full capacity. The statues are finished either rough or polished, with an average demand of 60 percent rough and 40 percent polished. Iron ingots, the direct material, costs $6 per kilogram. Processing costs are $200 to convert 20 kilograms into 40 statues; polishing adds $3 per statue. Rough statues are sold for $15 each and polished statues can be sold for $18 or engraved for an additional cost of $5. Engraved statues can then be sold for $30.

Required:

Determine if the engraving process is cost effective.

(Essay)

4.9/5 (33)

Match each of the following costs with the appropriate joint production process cost classification.

-Fuel oil from petroleum processing

(Multiple Choice)

4.9/5 (29)

Use the information below to answer the following question(s).

Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y) are obtained and sold. The following information was collected for the month of November.

Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What are the respective physical volume proportions for products X and Y?

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What are the respective physical volume proportions for products X and Y?

(Multiple Choice)

4.7/5 (38)

Use the information below to answer the following question(s).

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the physical measures method, the weightings for joint cost allocations for Jarlon and Kharton respectively are

(Multiple Choice)

4.8/5 (32)

Red Paper Company processes wood pulp into two products. During March the joint costs of processing were $144,000. Production and sales value information for the month were as follows:

Paper sells for $2.75 a kilogram and cardboard sells for $3.50 a kilogram.

There were no beginning inventories for March but ending inventories totalled 10,000 kilograms for paper and 12,000 kilograms for cardboard.

Required:

Prepare a product line income statement assuming that joint costs are allocated on the constant gross margin percentage method based on total production. Present production costs and separable costs individually.

Paper sells for $2.75 a kilogram and cardboard sells for $3.50 a kilogram.

There were no beginning inventories for March but ending inventories totalled 10,000 kilograms for paper and 12,000 kilograms for cardboard.

Required:

Prepare a product line income statement assuming that joint costs are allocated on the constant gross margin percentage method based on total production. Present production costs and separable costs individually.

(Essay)

4.9/5 (42)

BC Lumber Company prepares lumber for companies who manufacture furniture. The main product is finished lumber with a byproduct of wood shavings. The byproduct is sold to plywood manufacturers. For July, the manufacturing process incurred $332,000 in total costs. Eighty thousand board feet of lumber were produced and sold along with 6,800 pounds of shavings. The finished lumber sold for $6.00 per board foot and the shavings sold for $0.60 a pound. There were no beginning or ending inventories.

Required:

Prepare an income statement showing the byproduct (1) as a cost reduction during production, and (2) as a revenue item when sold.

(Essay)

4.8/5 (30)

Purple Paper Company processes wood pulp into two products. During July the joint costs of processing were $50,000. Production and sales value information for the month were as follows:

Paper sells for $2.71 a kilogram and cardboard sells for $3.10 a kilogram.

There were no beginning or ending inventories for July.

Required:

1. Determine the amounts to be allocated to each product using the:

a. constant gross margin percentage of NRV method

b. physical measure method

2. Should management process these products beyond the splitoff point? Justify your answer. Also comment on how this decision would be affected by the results of the expected profits using the constant gross margin percentage of NRV and physical measure methods.

Paper sells for $2.71 a kilogram and cardboard sells for $3.10 a kilogram.

There were no beginning or ending inventories for July.

Required:

1. Determine the amounts to be allocated to each product using the:

a. constant gross margin percentage of NRV method

b. physical measure method

2. Should management process these products beyond the splitoff point? Justify your answer. Also comment on how this decision would be affected by the results of the expected profits using the constant gross margin percentage of NRV and physical measure methods.

(Essay)

5.0/5 (43)

Match each of the following costs with the appropriate joint production process cost classification.

-Sawdust from a furniture manufacturer

(Multiple Choice)

4.8/5 (25)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)