Exam 5: The Mathematics of Diversification

Exam 1: The Process of Portfolio Management19 Questions

Exam 2: Valuation, Risk, Return, and Uncertainty70 Questions

Exam 3: Setting Portfolio Objectives39 Questions

Exam 4: Investment Policy27 Questions

Exam 5: The Mathematics of Diversification50 Questions

Exam 6: Why Diversification Is a Good Idea16 Questions

Exam 7: International Investment and Diversification23 Questions

Exam 8: The Capital Markets and Market Efficiency27 Questions

Exam 9: Picking the Equity Players28 Questions

Exam 10: Equity Valuation Tools15 Questions

Exam 11: Security Screening15 Questions

Exam 12: Bond Pricing and Selection80 Questions

Exam 13: The Role of Real Assets25 Questions

Exam 14: Alternative Assets12 Questions

Exam 15: Revision of the Equity Portfolio28 Questions

Exam 16: Revision of the Fixed-Income Portfolio33 Questions

Exam 17: Principles of Options and Option Pricing36 Questions

Exam 18: Option Overwriting41 Questions

Exam 19: Performance Evaluation25 Questions

Exam 20: Fiduciary Duties and Responsibilities16 Questions

Exam 21: Principles of the Futures Market19 Questions

Exam 22: Benching the Equity Players23 Questions

Exam 23: Removing Interest Rate Risk22 Questions

Exam 24: Integrating Derivative Assets and Portfolio Management12 Questions

Exam 25: Contemporary Issues in Portfolio Management11 Questions

Select questions type

A security has a return variance of 16%. The standard deviation of returns is

(Multiple Choice)

4.7/5  (44)

(44)

The variance of a two-security portfolio decreases as the return correlation of the two securities

(Multiple Choice)

4.7/5 (30)

Suppose Stock M has an expected return of 10%, a standard deviation of 15%, and a Beta of 0.6 while Stock N has an expected return of 20%, a standard deviation of 25% and a beta of 1.04, and the correlation between the two stocks is 0.50. What is the beta for a portfolio with 80% invested in Stock M and 20% invested in Stock N?

(Multiple Choice)

4.9/5 (33)

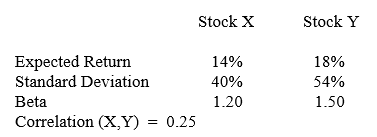

The questions relate to the following table of information:

-What is the beta for a portfolio with 60% invested in X and 40% invested in Y?

-What is the beta for a portfolio with 60% invested in X and 40% invested in Y?

(Multiple Choice)

4.8/5 (33)

As portfolio size increases, the variance of the error term generally

(Multiple Choice)

4.8/5 (30)

The questions relate to the following table of information:

-What is the expected return for a portfolio with 60% invested in X and 40% invested in Y?

(Multiple Choice)

4.9/5 (33)

A security has a return variance of 25%. The standard deviation of returns is

(Multiple Choice)

4.7/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)