Exam 5: Production and Cost Analysis in the Short Run

Exam 1: Managers and Economics68 Questions

Exam 2: Demand, supply, and Equilibrium Prices94 Questions

Exam 3: Demand Elasticities112 Questions

Exam 4: Techniques for Understanding Consumer Demand and Behavior67 Questions

Exam 5: Production and Cost Analysis in the Short Run101 Questions

Exam 6: Production and Cost Analysis in the Long Run100 Questions

Exam 7: Market Structure: Perfect Competition106 Questions

Exam 8: Market Structure: Monopoly and Monopolistic Competition107 Questions

Exam 9: Market Structure: Oligopoly96 Questions

Exam 10: Pricing Strategies for the Firm67 Questions

Exam 11: Measuring Macroeconomic Activity102 Questions

Exam 12: Spending by Individuals, firms, and Governments on Real Goods and Services103 Questions

Exam 13: The Role of Money in the Macro Economy90 Questions

Exam 14: The Aggregate Model of the Macro Economy98 Questions

Exam 15: International and Balance of Payments Issues in the Macro Economy109 Questions

Exam 16: Combining Micro and Macro Analysis for Managerial Decision Making44 Questions

Select questions type

Because it is a machine,a personal computer should be treated as a fixed input in the typical firm's short-run production function.

Free

(True/False)

4.8/5  (42)

(42)

Correct Answer: Verified

Verified

False

The "long run" is defined as a period of time long enough for the quantities of all of the inputs to production to vary.

Free

(True/False)

4.9/5 (37)

Correct Answer:Verified

True

Which of the following is true of the typical relationship between marginal product (MP)and average product (AP)?

Free

(Multiple Choice)

4.8/5 (29)

Correct Answer:Verified

C

Assume a factory that currently employs 25 workers is considering adding another 5 workers to its payroll.Economists would classify this as:

(Multiple Choice)

4.8/5 (36)

After the former CEO of the Coca-Cola Company began requiring employees to treat the rate of return on shareholder equity as an explicit cost,Coke's profits increased considerably.

(True/False)

4.7/5 (49)

Which of the following inputs is most likely to be "fixed" in the short run?

(Multiple Choice)

4.9/5 (46)

The amount of output a firm can produce with a given quantity of fixed and variable inputs is called:

(Multiple Choice)

4.9/5 (34)

Consider the production function for bottled water.All of the following would be considered variable inputs except:

(Multiple Choice)

4.8/5 (41)

-Refer to Scenario 3.The marginal cost of producing the sixth unit of output is:

-Refer to Scenario 3.The marginal cost of producing the sixth unit of output is:

(Multiple Choice)

4.8/5 (31)

-Refer to Scenario 3.Diminishing marginal returns are incurred when output is increased from:

(Multiple Choice)

4.8/5 (40)

Assume a firm is currently producing 100 units of output,total fixed costs are $10,000,and average variable costs are $8.Based on this information we can conclude,with certainty,that the firm's:

(Multiple Choice)

4.8/5 (39)

If a firm experiences constant returns to the variable input in the short run:

(Multiple Choice)

4.9/5 (41)

Marginal cost is defined as the change in ________ cost when output changes by one unit.In the short run,marginal cost can also be measured by the change in ________ cost when output changes by one unit.

(Multiple Choice)

4.9/5 (30)

A firm's decision to expand the size of its production facility would be considered a short-run decision so long as the expansion can be completed in less than a year.

(True/False)

4.8/5 (33)

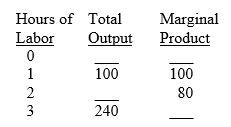

Scenario 1: The following is a hypothetical short-run production function:

-Refer to Scenario 1.What is the average product of the first three hours of labor?

-Refer to Scenario 1.What is the average product of the first three hours of labor?

(Multiple Choice)

4.7/5 (35)

Economic theory provides insights into the range of possibilities for cost relationships.Studies such as those by Blinder et al.provide insights into where,within that range,many firms operate.Thus,there is no real conflict between theory and reality,as some people might try to claim.

(True/False)

4.9/5 (36)

Which of the following is not a determinant of a firm's cost functions?

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)