Exam 5: Production and Cost Analysis in the Short Run

Exam 1: Managers and Economics68 Questions

Exam 2: Demand, supply, and Equilibrium Prices94 Questions

Exam 3: Demand Elasticities112 Questions

Exam 4: Techniques for Understanding Consumer Demand and Behavior67 Questions

Exam 5: Production and Cost Analysis in the Short Run101 Questions

Exam 6: Production and Cost Analysis in the Long Run100 Questions

Exam 7: Market Structure: Perfect Competition106 Questions

Exam 8: Market Structure: Monopoly and Monopolistic Competition107 Questions

Exam 9: Market Structure: Oligopoly96 Questions

Exam 10: Pricing Strategies for the Firm67 Questions

Exam 11: Measuring Macroeconomic Activity102 Questions

Exam 12: Spending by Individuals, firms, and Governments on Real Goods and Services103 Questions

Exam 13: The Role of Money in the Macro Economy90 Questions

Exam 14: The Aggregate Model of the Macro Economy98 Questions

Exam 15: International and Balance of Payments Issues in the Macro Economy109 Questions

Exam 16: Combining Micro and Macro Analysis for Managerial Decision Making44 Questions

Select questions type

Florence is considering going into business for herself and has developed the following estimates of monthly costs and revenues to aid her in her decision-making process.She has decided to house the business in a building that she already owns,although she could rent the building to someone else for $1,000 per month.Estimated payments for utilities (electricity,natural gas,water,and telephone)are $475 per month.She will hire one employee at a total cost of $1,100 per month.Inventory is estimated to cost $2,800 per month.Finally,Florence earns $3,000 a month in her current job.

a.How much monthly revenue would Florence have to take in to earn 0 economic profit?

b.Assume that Florence has estimated her monthly revenue to be $9,000.In this case,Florence would earn an accounting profit (loss)of ________,and an economic profit (loss)of ________.

c.Assume instead that Florence does not own a building,and that she will have to rent a building for $1,000 per month (all other estimates remain the same).In this case (assuming estimated monthly revenue is still $9,000),Florence would earn an accounting profit (loss)of ________,and an economic profit (loss)of ________.

(Essay)

4.8/5  (42)

(42)

A firm's production function is the relationship between the factors of production and the resulting outputs of the production process.

(True/False)

4.8/5 (35)

All else constant,an improvement in technology would cause a firm's marginal,average variable,and average total cost functions to increase (graphically,shift up).

(True/False)

4.9/5 (28)

The text lists all of the following as outcomes of McDonald's experimental adoption of remote order taking except:

(Multiple Choice)

5.0/5 (44)

The amount of money a firm pays to lease a building it uses for office space is called:

(Multiple Choice)

4.8/5 (36)

According to the text,much of the increase in productivity that has occurred more recently in the fast food industry was the result of improvements in capital and technology.

(True/False)

4.8/5 (35)

Use the following information on a hypothetical short-run production function to answer questions a-c.

The price of labor is $20 per day.Ten units of capital are used each day,regardless of output level.The price of capital is $50 per unit.

a.Calculate the marginal and average variable product of each unit of labor input.

b.Calculate total,average total,average variable,and marginal costs.

c.Can you tell where diminishing marginal returns sets in?

The price of labor is $20 per day.Ten units of capital are used each day,regardless of output level.The price of capital is $50 per unit.

a.Calculate the marginal and average variable product of each unit of labor input.

b.Calculate total,average total,average variable,and marginal costs.

c.Can you tell where diminishing marginal returns sets in?

(Essay)

4.8/5 (42)

Once a firm incurs diminishing marginal returns,total product will begin to decline as more of the variable input is employed.

(True/False)

4.8/5 (44)

In the context of a production function,the remote order takers in the fast food industry would be classified as:

(Multiple Choice)

4.8/5 (31)

In the mathematical formulation of the short-run production function:

(Multiple Choice)

4.8/5 (41)

Which of the following statements concerning the relationships among the firm's total cost functions is false?

(Multiple Choice)

4.8/5 (36)

Empirical evidence indicates that most firms operate where marginal and average variable costs are constant.

(True/False)

4.9/5 (37)

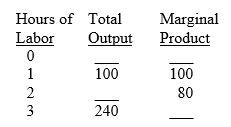

Scenario 1: The following is a hypothetical short-run production function:

-Refer to Scenario 1.The production function illustrated in the table:

-Refer to Scenario 1.The production function illustrated in the table:

(Multiple Choice)

4.9/5 (36)

Which of the following statements regarding historical costs is correct?

(Multiple Choice)

4.8/5 (35)

The term "variable input" is used to refer to inputs that vary in terms of quality and,therefore,productivity.

(True/False)

4.8/5 (34)

If,for a particular short-run production,we observe that marginal product is decreasing we can conclude that average product is decreasing as well.

(True/False)

4.8/5 (31)

For a particular farmer and a single growing season,the amount of seed that is planted would be considered a variable input.

(True/False)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)