Exam 9: A: Price Takers and the Competitive Process

Exam 1: The Economic Approach210 Questions

Exam 2: A: Some Tools of the Economist224 Questions

Exam 2: B: Some Tools of the Economist33 Questions

Exam 3: A: Supply, Demand, and the Market Process225 Questions

Exam 3: B: Supply, Demand, and the Market Process180 Questions

Exam 4: A: Supply and Demand: Applications and Extensions233 Questions

Exam 4: B: Supply and Demand: Applications and Extensions98 Questions

Exam 5: Difficult Cases for the Market and the Role of Government168 Questions

Exam 6: The Economics of Collective Decision-Making180 Questions

Exam 7: Consumer Choice and Elasticity223 Questions

Exam 8: A: Costs and the Supply of Goods223 Questions

Exam 8: B: Costs and the Supply of Goods8 Questions

Exam 9: A: Price Takers and the Competitive Process237 Questions

Exam 9: B: Price Takers and the Competitive Process23 Questions

Exam 10: Price-Searcher Markets With Low Entry Barriers216 Questions

Exam 11: A: Price-Searcher Markets With High Entry Barriers229 Questions

Exam 11: B: Price-Searcher Markets With High Entry Barriers25 Questions

Exam 12: The Supply of and Demand for Productive Resources200 Questions

Exam 13: Earnings, Productivity, and the Job Market109 Questions

Exam 14: Investment, the Capital Market, and the Wealth of Nations129 Questions

Exam 15: Income Inequality and Poverty136 Questions

Exam 16: Appendix: Government Spending and Taxation79 Questions

Exam 17: Appendix: the Economics of Social Security54 Questions

Exam 18: Appendix: the Stock Market: Its Function, Performance, and Potential As an Investment Opportunity70 Questions

Exam 19: Appendix: Great Debates in Economics: Keynes Versus Hayek8 Questions

Exam 20: Appendix: the Crisis of 2008: Causes and Lessons for the Future64 Questions

Exam 21: Appendix: Lessons From the Great Depression60 Questions

Exam 22: Appendix: the Economics of Healthcare68 Questions

Exam 23: Appendix:education: Problems and Performance60 Questions

Exam 24: Appendix: Earnings Differences Between Men and Women47 Questions

Exam 26: Appendix: the Question of Resource Exhaustion61 Questions

Exam 25: Appendix: Do Labor Unions Increase the Wages of Workers74 Questions

Exam 27: Appendix: Difficult Environmental Cases and the Role of Government63 Questions

Select questions type

If long-run equilibrium is present in a competitive market, the typical firm in the market will be

Free

(Multiple Choice)

4.9/5  (37)

(37)

Correct Answer: Verified

Verified

B

The exit of existing firms from a competitive market will

Free

(Multiple Choice)

4.9/5 (32)

Correct Answer:Verified

C

When profits occur in a competitive market, this indicates that

Free

(Multiple Choice)

5.0/5 (29)

Correct Answer:Verified

A

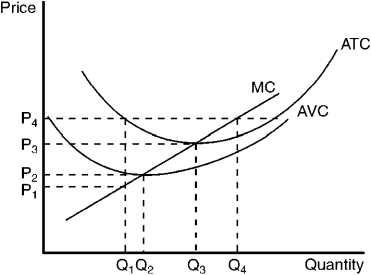

Figure 9-13

-Refer to Figure 9-13. When price falls from P₃ to P₁, the firm finds that

-Refer to Figure 9-13. When price falls from P₃ to P₁, the firm finds that

(Multiple Choice)

4.9/5 (29)

Which of the following is true for a constant cost industry?

(Multiple Choice)

4.9/5 (35)

Which one of the following factors is not an explanation of the positive relationship between market price and quantity supplied?

(Multiple Choice)

4.9/5 (39)

If the demand and marginal revenue curves confronting firm A are identical, it may be concluded that firm A is a

(Multiple Choice)

4.9/5 (34)

If the demand for a product increases in an increasing-cost industry, as the market adjusts in the long run, production costs for all firms will

(Multiple Choice)

5.0/5 (34)

Figure 9-8

-At the market price of $3 in Figure 9-8, indicate the firm's total revenue and total cost at its profit-maximizing level of output.

-At the market price of $3 in Figure 9-8, indicate the firm's total revenue and total cost at its profit-maximizing level of output.

(Multiple Choice)

4.8/5 (34)

Which of the following is a reason to study the decisions of price takers?

(Multiple Choice)

4.9/5 (36)

If consumers suddenly began desiring more apples and fewer oranges,

(Multiple Choice)

4.9/5 (37)

If a single firm in a price-taker market lowers its price below the market equilibrium price,

(Multiple Choice)

4.8/5 (35)

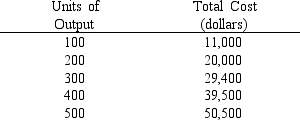

The schedule of total costs for a chair-manufacturing firm is presented in the table below. If the market price of chairs is $100, which output should this price-taker firm produce to maximize profit?

(Multiple Choice)

4.9/5 (32)

Claude's Copper Clappers sells clappers for $40 each in a competitive price-taker market. At its present rate of output, Claude's marginal cost is $40, average variable cost is $45, and average total cost is $60. Claude should

(Multiple Choice)

4.8/5 (29)

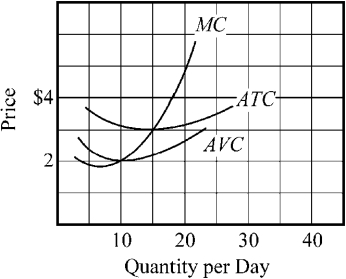

Figure 9-7

-The average total cost (ATC) and marginal costs (MC) of a firm producing in a price-taker industry are depicted in Figure 9-7. If the current market price of the firm's product is $3, what output should this firm produce per week?

-The average total cost (ATC) and marginal costs (MC) of a firm producing in a price-taker industry are depicted in Figure 9-7. If the current market price of the firm's product is $3, what output should this firm produce per week?

(Multiple Choice)

4.8/5 (36)

If a competitive price-taking firm is operating in long-run equilibrium and market demand suddenly falls, the short-run result will be

(Multiple Choice)

4.8/5 (26)

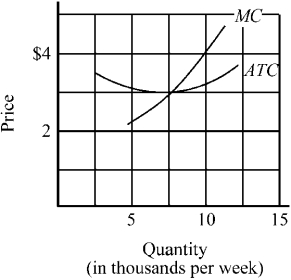

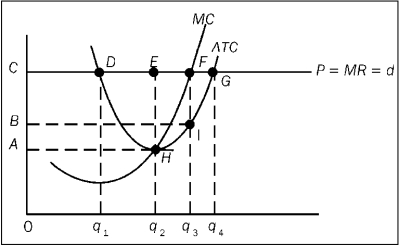

Figure 9-18

-Refer to Figure 9-18. To maximize profit, the firm should produce an output level of

-Refer to Figure 9-18. To maximize profit, the firm should produce an output level of

(Multiple Choice)

4.8/5 (35)

If price is above average variable cost and below average total cost, a profit-maximizing price taker should

(Multiple Choice)

4.8/5 (34)

When new firms have an incentive to enter a competitive price-taker market, their entry will

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)