Exam 22: An Introduction to Macroeconomics

Exam 1: What Is Economics232 Questions

Exam 2: The Economy: Myth and Reality155 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice255 Questions

Exam 4: Supply and Demand: an Initial Look313 Questions

Exam 5: Consumer Choice: Individual and Market Demand206 Questions

Exam 6: Demand and Elasticity214 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis221 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis194 Questions

Exam 9: Securities: Business Finance and the Economy: the Tail That Wags the Dog203 Questions

Exam 10: The Firm and the Industry Under Perfect Competition212 Questions

Exam 11: Monopoly208 Questions

Exam 12: Between Competition and Monopoly230 Questions

Exam 13: Limiting Market Power: Regulation and Antitrust155 Questions

Exam 14: The Case for Free Markets: the Price System225 Questions

Exam 15: The Shortcomings of Free Markets219 Questions

Exam 16: Externalities, the Environment, and Natural Resources222 Questions

Exam 17: Taxation and Resource Allocation221 Questions

Exam 18: Pricing the Factors of Production233 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs271 Questions

Exam 20: Poverty, Inequality, and Discrimination172 Questions

Exam 21: Is Useconomic Leadership Threatened75 Questions

Exam 22: An Introduction to Macroeconomics216 Questions

Exam 23: The Goals of Macroeconomic Policy212 Questions

Exam 24: Economic Growth: Theory and Policy228 Questions

Exam 25: Aggregate Demand and the Powerful Consumer219 Questions

Exam 26: Demand-Side Equilibrium: Unemployment or Inflation216 Questions

Exam 27: Bringing in the Supply Side: Unemployment and Inflation228 Questions

Exam 28: Managing Aggregate Demand: Fiscal Policy210 Questions

Exam 29: Money and the Banking System224 Questions

Exam 30: Monetary Policy: Conventional and Unconventional210 Questions

Exam 31: He Financial Crisis and the Great Recession66 Questions

Exam 32: The Debate Over Monetary and Fiscal Policy219 Questions

Exam 33: Budget Deficits in the Short and Long Run215 Questions

Exam 34: The Trade-Off Between Inflation and Unemployment219 Questions

Exam 35: International Trade and Comparative Advantage223 Questions

Exam 36: The International Monetary System: Order or Disorder218 Questions

Exam 37: Exchange Rates and the Macroeconomy219 Questions

Select questions type

GDP in 2015 would not include the resale of a house built in 2000.

Free

(True/False)

4.9/5  (32)

(32)

Correct Answer: Verified

Verified

True

Cars produced by General Motors in Mexico would be included in U.S.Gross Domestic Product.

Free

(True/False)

4.7/5 (36)

Correct Answer:Verified

False

A good produced in 2009 and held in inventory until it is sold in 2010 would be included in which measure of GDP?

(Multiple Choice)

4.9/5 (28)

What are intermediate goods?

Why do economists exclude the value of intermediate goods while calculating national income?

(Essay)

4.9/5 (35)

What makes the macroeconomic performance of the 1993 to 1998 period so unusual is the

(Multiple Choice)

4.9/5 (25)

The first year of the Bush administration in 2001 could be represented as a(n)

(Multiple Choice)

4.9/5 (35)

The horizontal axis on the aggregate demand-aggregate supply model measures

(Multiple Choice)

4.7/5 (26)

Economist John Maynard Keynes wrote that the economy naturally gravitates toward smooth growth and high levels of employment.

(True/False)

4.8/5 (32)

Before the Great Depression of the 1930s, most economists believed that

(Multiple Choice)

4.9/5 (45)

The existence of the "underground economy" causes measured GDP to overestimate actual output.

(True/False)

4.8/5 (33)

While their respective subject matters differ greatly, both microeconomists and macroeconomists rely on the same basic tools; that is, both rely on

(Multiple Choice)

4.8/5 (40)

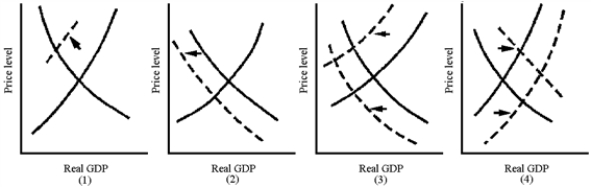

Aggregate demand and supply curves have been widely used to analyze the performance of the macroeconomy.Figure 5-3 shows four diagrams that represent different changes in the macroeconomy.Choose the diagram that best represents the situations described in the following questions.??Figure 5-3

-Which graph in Figure 5-3 best represents the aggregate demand-induced Great Depression of the 1930s?

-Which graph in Figure 5-3 best represents the aggregate demand-induced Great Depression of the 1930s?

(Multiple Choice)

4.9/5 (37)

Stagflation is the simultaneous occurrence of inflation and high unemployment.

(True/False)

4.9/5 (41)

John Maynard Keynes wrote that economies can suffer recession or depression for many years if the government does not intervene.

(True/False)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)