Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis

Exam 1: What Is Economics232 Questions

Exam 2: The Economy: Myth and Reality155 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice255 Questions

Exam 4: Supply and Demand: an Initial Look313 Questions

Exam 5: Consumer Choice: Individual and Market Demand206 Questions

Exam 6: Demand and Elasticity214 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis221 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis194 Questions

Exam 9: Securities: Business Finance and the Economy: the Tail That Wags the Dog203 Questions

Exam 10: The Firm and the Industry Under Perfect Competition212 Questions

Exam 11: Monopoly208 Questions

Exam 12: Between Competition and Monopoly230 Questions

Exam 13: Limiting Market Power: Regulation and Antitrust155 Questions

Exam 14: The Case for Free Markets: the Price System225 Questions

Exam 15: The Shortcomings of Free Markets219 Questions

Exam 16: Externalities, the Environment, and Natural Resources222 Questions

Exam 17: Taxation and Resource Allocation221 Questions

Exam 18: Pricing the Factors of Production233 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs271 Questions

Exam 20: Poverty, Inequality, and Discrimination172 Questions

Exam 21: Is Useconomic Leadership Threatened75 Questions

Exam 22: An Introduction to Macroeconomics216 Questions

Exam 23: The Goals of Macroeconomic Policy212 Questions

Exam 24: Economic Growth: Theory and Policy228 Questions

Exam 25: Aggregate Demand and the Powerful Consumer219 Questions

Exam 26: Demand-Side Equilibrium: Unemployment or Inflation216 Questions

Exam 27: Bringing in the Supply Side: Unemployment and Inflation228 Questions

Exam 28: Managing Aggregate Demand: Fiscal Policy210 Questions

Exam 29: Money and the Banking System224 Questions

Exam 30: Monetary Policy: Conventional and Unconventional210 Questions

Exam 31: He Financial Crisis and the Great Recession66 Questions

Exam 32: The Debate Over Monetary and Fiscal Policy219 Questions

Exam 33: Budget Deficits in the Short and Long Run215 Questions

Exam 34: The Trade-Off Between Inflation and Unemployment219 Questions

Exam 35: International Trade and Comparative Advantage223 Questions

Exam 36: The International Monetary System: Order or Disorder218 Questions

Exam 37: Exchange Rates and the Macroeconomy219 Questions

Select questions type

Marginal profit is the slope of the total profit curve.

Free

(True/False)

4.7/5  (37)

(37)

Correct Answer: Verified

Verified

True

If a firm's fixed cost (overhead) increases, what happens to its profit-maximizing price and output?

Free

(Essay)

4.8/5 (31)

Correct Answer:Verified

Nothing.Whatever output was most profitable before the increase in fixed costs must still be most profitable because total profit is reduced by the same amount at each and every output level and marginal cost has not changed.

If marginal cost of an additional unit of output is greater than average cost, then average cost will rise.

Free

(True/False)

4.8/5 (39)

Correct Answer:Verified

True

Economists assume that business firms have many goals, and profit maximization is just one of them.

(True/False)

4.8/5 (44)

Management gets two numbers (price and quantity) from one decision because

(Multiple Choice)

4.8/5 (31)

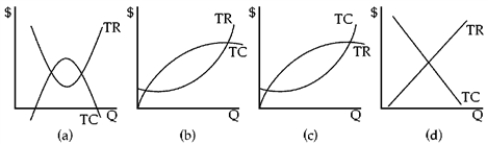

Figure 8-1

-Which graph in Figure 8-1 shows a typical firm's total revenue and total cost curves?

-Which graph in Figure 8-1 shows a typical firm's total revenue and total cost curves?

(Multiple Choice)

4.7/5 (40)

Average cost equals total cost multiplied by the number of units of output.

(True/False)

4.9/5 (34)

Thomas Edison once said that he began making real profit on light bulbs when he dumped his surplus on the European market at less than the "cost of production." From this we can deduce Edison

(Multiple Choice)

4.8/5 (40)

Herbert Simon has concluded that decision making in industry is often best described as

(Multiple Choice)

4.9/5 (38)

Most consumers in stores use marginal analysis to make their buying decisions.

(True/False)

4.8/5 (37)

The typical total profit graphical presentation is shown as

(Multiple Choice)

4.9/5 (39)

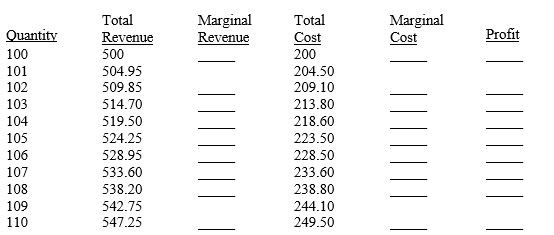

Complete the following table and determine the point of profit maximization.

(Essay)

4.9/5 (36)

Marginal cost is defined by the slope of the total revenue curve.

(True/False)

4.8/5 (43)

If the marginal profit from increasing output by one unit is negative, then to attain an optimum the firm should

(Multiple Choice)

4.9/5 (25)

If a person who weighs 100 lbs.is riding in an elevator and is joined by a person weighing 120 lbs., what happens to the average weight of persons on the elevator?

(Multiple Choice)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)