Exam 6: Inventory

Exam 1: Business, Accounting, and You121 Questions

Exam 2: Analyzing and Recording Business Transactions133 Questions

Exam 3: Adjusting and Closing Entries127 Questions

Exam 4: Ethics, Internal Control, and Cash134 Questions

Exam 5: Accounting for a Merchandising Business139 Questions

Exam 6: Inventory138 Questions

Exam 7: Sales and Receivables86 Questions

Exam 8: Long-Term Assets161 Questions

Exam 9: Current Liabilities and Long-Term Debt90 Questions

Exam 10: Corporations: Share Capital and Retained Earnings119 Questions

Exam 11: The Cash Flow Statement111 Questions

Exam 12: Financial Statement Analysis112 Questions

Select questions type

After a physical count, the ending inventory is adjusted. Where on the balance sheet is the ending inventory shown?

(Short Answer)

4.7/5  (34)

(34)

Counting inventory on December 31 that was shipped FOB shipping point would not cause any error in the final inventory valuation.

(True/False)

4.9/5 (42)

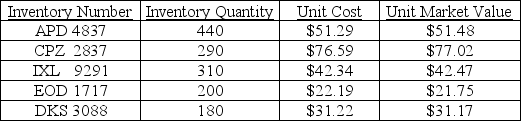

Nicola Company reports the following inventory information:

What is the total value of the merchandise under LNRV M (lower of cost or net realizable value)? Show all your calculations.

What is the total value of the merchandise under LNRV M (lower of cost or net realizable value)? Show all your calculations.

(Essay)

4.8/5 (38)

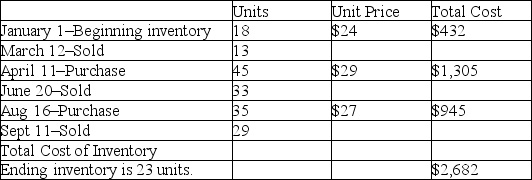

Rick Company's beginning inventory and purchases during the fiscal year ended December 31, 2012 were as follows: (NOTE: The company uses a perpetual system of inventory.)

What is the cost of goods sold for Rick Company for 2012 using FIFO showing detailed calculations.

What is the cost of goods sold for Rick Company for 2012 using FIFO showing detailed calculations.

(Essay)

4.8/5 (37)

The inventory system whereby the merchandise inventory account balance is merely a record of the most recent physical inventory count is called the:

(Short Answer)

4.9/5 (36)

Net sales minus estimated gross profit yields the estimated __________.

(Short Answer)

4.8/5 (36)

The ending inventory of one year becomes the beginning inventory of the next year.

(True/False)

4.7/5 (37)

Which is usually NOT a common practice in taking a physical inventory?

(Multiple Choice)

4.8/5 (39)

Inventory turnover equals the cost of goods sold divided by ending inventory.

(True/False)

4.9/5 (38)

Which method of valuing inventory is based on the average of units?

(Short Answer)

4.8/5 (37)

2012 ending inventory is $25,000; 2013 ending inventory is $19,500; 2014 ending inventory is $22,000; and cost of goods sold is $65,500 for 2014 and $67,900 for 2013. What is the days in inventory for 2013 and 2014? Has it improved?

(Essay)

4.8/5 (39)

The last step in using the gross profit method to estimate ending inventory is to:

(Multiple Choice)

4.9/5 (53)

If the ending inventory in Period 1 is understated, gross profit for Year 1 is __________.

(Short Answer)

4.9/5 (41)

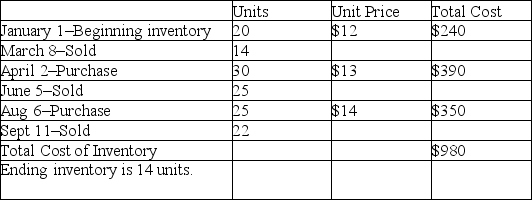

Casey Company's beginning inventory and purchases during the fiscal year ended December 31, 2012 were as follows: (NOTE: The company uses a perpetual system of inventory.)

What is the ending inventory of Casey Company for 2012 using FIFO?

What is the ending inventory of Casey Company for 2012 using FIFO?

(Short Answer)

4.8/5 (40)

If a misstatement of inventory occurs, the net income for __________ periods will be misstated.

(Short Answer)

4.8/5 (37)

Journalize the following transactions for the next three independent situations.

Case 1

Gertrude Enterprises has determined that the replacement cost (current market value) of the December 31, 2014 ending inventory is $32,400.The inventory is recorded on the balance sheet at $33,500. What is the journal entry using the lower of cost or net realizable value rule?

Case 2

Austin's Jewellers carries a line of silver bracelets. Austin's Jewellers uses the FIFO method and a perpetual inventory system. The sales price of each bracelet is $105. Company records indicate the following activity for the bracelets for the month of March: Purchases of 200 units on January 1 at a cost of $30 per unit and purchases of 400 units on February 1 at a cost of $33 per unit. Sold 300 units on account on February 25. Journalize the sale of 300 units.

Case 3

On January 2, 2014, Bright Lights purchased showroom fixtures for $10,000 cash, expecting the fixtures to remain in service for five years. Bright Lights has depreciated the fixtures on a straight-line basis, with zero residual value. On September 30, 2015, Bright Lights sold the fixtures for $5,000 cash. Record both

the depreciation expense on the fixtures for 2015 and the sale of the fixtures on September 30, 2015.

(Essay)

4.9/5 (40)

Goods available for sale are $85,000; beginning inventory is $27,000; ending inventory is $19,000; and cost of goods sold is $63,500. What is the inventory turnover?

(Short Answer)

5.0/5 (36)

What is the method used to estimate the cost of ending inventory?

(Short Answer)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)