Exam 15: Perfect Competition

Exam 1: Getting Started337 Questions

Exam 2: The Usand Global Economies201 Questions

Exam 3: The Economic Problem273 Questions

Exam 4: Demand and Supply322 Questions

Exam 5: Elasticities of Demand and Supply335 Questions

Exam 6: Efficiency and Fairness of Markets352 Questions

Exam 7: Government Actions in Markets239 Questions

Exam 8: Taxes267 Questions

Exam 9: Global Markets in Action276 Questions

Exam 10: Externalities300 Questions

Exam 11: Public Goods and Common Resources177 Questions

Exam 12: Markets With Private Information101 Questions

Exam 13: Consumer Choice and Demand287 Questions

Exam 14: Production and Cost266 Questions

Exam 15: Perfect Competition275 Questions

Exam 16: Monopoly377 Questions

Exam 17: Monopolistic Competition213 Questions

Exam 18: Oligopoly222 Questions

Exam 19: Markets for Factors of Production178 Questions

Exam 20: Economic Inequality155 Questions

Select questions type

If perfectly competitive firms are making an economic profit, then

Free

(Multiple Choice)

4.8/5  (36)

(36)

Correct Answer: Verified

Verified

C

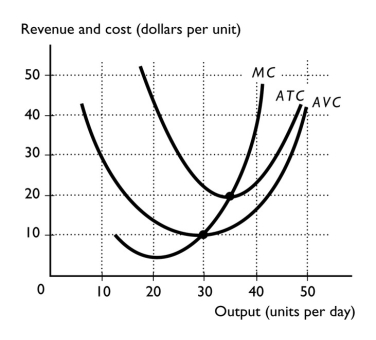

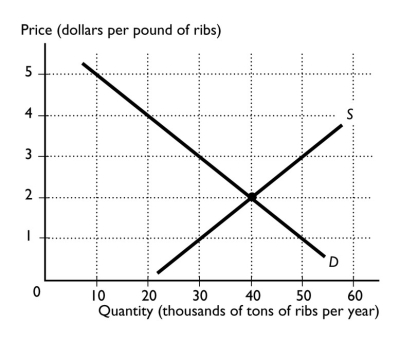

-The above figure shows a perfectly competitive firm.If the market price is more than $20 per unit, the firm

-The above figure shows a perfectly competitive firm.If the market price is more than $20 per unit, the firm

Free

(Multiple Choice)

4.8/5 (38)

Correct Answer:Verified

D

A perfectly competitive firm's short-run supply curve is

Free

(Multiple Choice)

4.7/5 (24)

Correct Answer:Verified

D

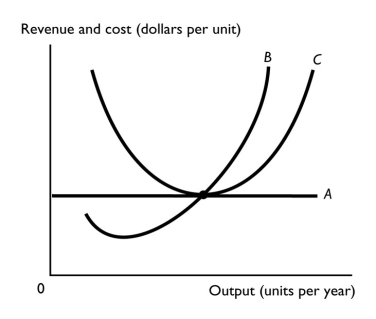

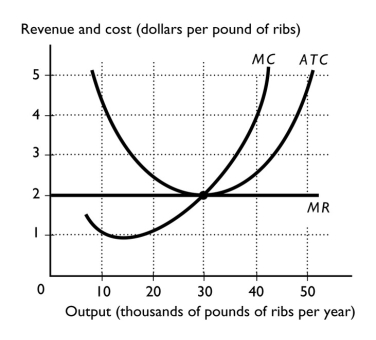

-The above figure illustrates a perfectly competitive firm.Curve C represents the

-The above figure illustrates a perfectly competitive firm.Curve C represents the

(Multiple Choice)

4.9/5 (27)

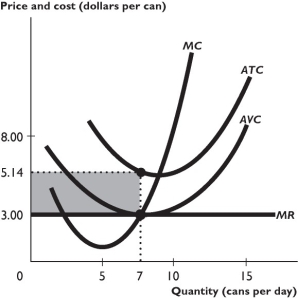

The above figure shows some a firm's cost curves and its marginal revenue curve.

-Based on the figure above, if the firm produces 7 cans per day, the firm ________ maximizing its profit and is ________.

The above figure shows some a firm's cost curves and its marginal revenue curve.

-Based on the figure above, if the firm produces 7 cans per day, the firm ________ maximizing its profit and is ________.

(Multiple Choice)

4.8/5 (38)

If the market price of a product is $14 and all sellers are price takers, then which of the following is correct?

(Multiple Choice)

4.7/5 (25)

Entry by competitive firms decreases the market price, while exit by competitive firms increases the market price.Explain why firms enter or exit an industry and why these price changes occur.

(Essay)

4.8/5 (34)

If a perfectly competitive firm's marginal revenue is greater than its marginal cost, as it increases its output, its profit ________ and the price it can charge for its product ________.

(Multiple Choice)

5.0/5 (25)

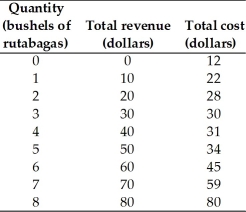

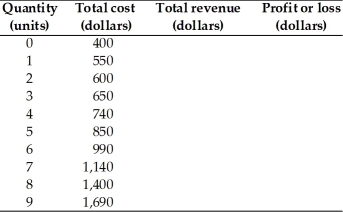

-The above table has the total revenue and total cost schedule for Omar, a perfectly competitive grower of rutabagas.Omar's total profit is maximized when he produces ________ bushels of rutabagas.

-The above table has the total revenue and total cost schedule for Omar, a perfectly competitive grower of rutabagas.Omar's total profit is maximized when he produces ________ bushels of rutabagas.

(Multiple Choice)

4.8/5 (36)

-Suppose the bobby pin industry is perfectly competitive.The price of a packet of bobby pins is $2.00.Pins and Needles, Inc.is a firm in this industry and is producing 1,000 packets of bobby pins per day at the point where the MC = MR.The average cost of production at this output level is $1.50 per packet.

a∙What is the marginal cost of the 1,000th packet?

b∙Is this firm making an economic profit, zero economic profit, or an economic loss? How much?

c∙Is the firm in long-run equilibrium? Why or why not?

-Suppose the bobby pin industry is perfectly competitive.The price of a packet of bobby pins is $2.00.Pins and Needles, Inc.is a firm in this industry and is producing 1,000 packets of bobby pins per day at the point where the MC = MR.The average cost of production at this output level is $1.50 per packet.

a∙What is the marginal cost of the 1,000th packet?

b∙Is this firm making an economic profit, zero economic profit, or an economic loss? How much?

c∙Is the firm in long-run equilibrium? Why or why not?

(Essay)

4.8/5 (30)

Elsie is a perfectly competitive dairy farmer.The market price of milk was $2.40 but just fell to $2.20 a gallon.Elsie

(Multiple Choice)

4.8/5 (39)

If demand for a seller's product is perfectly elastic, which of the following is true?

I∙The firm will sell no output if it sets the price its product above the market price.

Ii∙There are many perfect substitutes for the seller's product.

Iii∙The firm will sell no output if it sets the price its product below the market price.

(Multiple Choice)

4.8/5 (27)

The U-pick berry market is perfectly competitive.Suppose that all U-pick blueberry farms have the same cost curves and all are making an economic profit.What happens as time passes? What is the long-run equilibrium outcome?

(Essay)

4.7/5 (38)

The table below shows the total cost schedule for a perfectly competitive firm.The market price is $250 per unit.Complete the table.

(Essay)

4.9/5 (33)

Firms exit a competitive market when they incur an economic loss.In the long run, this exit means that the economic losses of the surviving firms

(Multiple Choice)

4.9/5 (34)

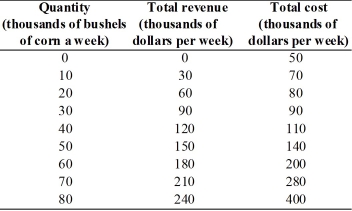

-Jimmy grows corn.His total revenue and total cost are in the above table.What quantity of corn maximizes his profit and what is his profit? What is the marginal revenue and marginal cost at this quantity?

-Jimmy grows corn.His total revenue and total cost are in the above table.What quantity of corn maximizes his profit and what is his profit? What is the marginal revenue and marginal cost at this quantity?

(Essay)

4.8/5 (28)

If a struggling perfectly competitive furniture store in Detroit shuts down, it incurs an economic loss equal to its

(Multiple Choice)

4.9/5 (32)

A firm maximizes its profit by producing the amount of output such that

(Multiple Choice)

4.8/5 (40)

-The above table has the total revenue and total cost schedule for Omar, a perfectly competitive grower of rutabagas.When Omar maximizes his profit, Omar's profit equals

(Multiple Choice)

4.7/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)