Exam 8: Foreign Currency Derivatives and Swaps

Exam 1: Current Multinational Challenges and the Global Economy33 Questions

Exam 2: Financial Goals and Corporate Governance54 Questions

Exam 3: The International Monetary System54 Questions

Exam 4: The Balance of Payments57 Questions

Exam 5: Current Multinational Financial Challenges: the Credit Crisis of 2007 - 200946 Questions

Exam 6: The Foreign Exchange Market57 Questions

Exam 7: International Parity Conditions56 Questions

Exam 8: Foreign Currency Derivatives and Swaps65 Questions

Exam 9: Foreign Exchange Rate Determination and Forecasting53 Questions

Exam 10: Transaction and Translation Exposure69 Questions

Exam 11: Operating Exposure54 Questions

Exam 12: The Global Cost and Availability of Capital57 Questions

Exam 13: Sourcing Equity and Debt Globally80 Questions

Exam 14: Multinational Tax Management57 Questions

Exam 15: Foreign Direct Investment and Political Risk55 Questions

Exam 16: Multinational Capital Budgeting and Cross-Border Acquisitions56 Questions

Exam 17: International Portfolio Theory and Diversification57 Questions

Exam 18: Working Capital Management63 Questions

Exam 19: International Trade Finance61 Questions

Select questions type

An agreement to exchange interest payments based on a fixed payment for those based on a variable rate (or vice versa)is known as a/an ________.

Free

(Multiple Choice)

4.8/5  (38)

(38)

Correct Answer: Verified

Verified

C

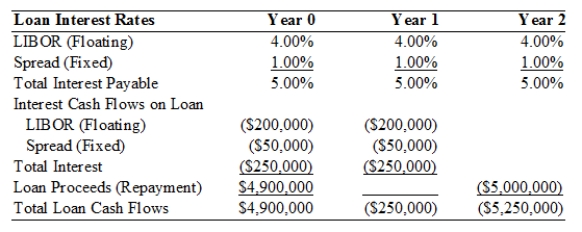

TABLE 8.2

Use the information for Polaris Corporation to answer the following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer to Table 8.2.What portion of the cost of the loan is at risk of changing?

-Refer to Table 8.2.What portion of the cost of the loan is at risk of changing?

Free

(Multiple Choice)

4.9/5 (38)

Correct Answer:Verified

A

TABLE 8.2

Use the information for Polaris Corporation to answer the following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer to Table 8.2.If the LIBOR rate jumps to 5.00% after the first year what will be the all-in-cost (i.e.the internal rate of return)for Polaris for the entire loan?

Free

(Multiple Choice)

4.9/5 (41)

Correct Answer:Verified

D

Instruction 8.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 8.1.The risk of strategy #1 is that interest rates might go down or that your credit rating might improve.The risk of strategy #2 is (Assume your firm is borrowing money.)

(Multiple Choice)

4.8/5 (41)

TABLE 8.2

Use the information for Polaris Corporation to answer the following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer to Table 8.2.What is the all-in-cost (i.e.,the internal rate of return)of the Polaris loan including the LIBOR rate,fixed spread and upfront fee?

(Multiple Choice)

4.9/5 (46)

Which of the following would be considered an example of a currency swap?

(Multiple Choice)

4.8/5 (33)

A foreign currency ________ gives the purchaser the right,not the obligation,to buy a given amount of foreign exchange at a fixed price per unit for a specified period.

(Multiple Choice)

4.8/5 (44)

Peter Simpson thinks that the U.K.pound will cost $1.43/£ in six months.A 6-month currency futures contract is available today at a rate of $1.44/£.If Peter was to speculate in the currency futures market,and his expectations are correct,which of the following strategies would earn him a profit?

(Multiple Choice)

4.9/5 (38)

All exchange-traded options are settled through a clearing house but over-the-counter options are not and are thus subject to greater ________ risk.

(Multiple Choice)

4.9/5 (38)

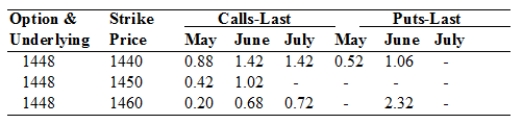

TABLE 8.1

Use the below mentioned table to answer the following question(s).

April 19, 2010, British Pound Option Prices (cents per pound, 62,500 pound contracts).

-Refer to Table 8.1.The May call option on pounds with a strike price of 1440 means ________.

-Refer to Table 8.1.The May call option on pounds with a strike price of 1440 means ________.

(Multiple Choice)

4.8/5 (32)

As a general statement,it is safe to say that businesses generally use the ________ for foreign currency option contracts,and individuals and financial institutions typically use the ________.

(Multiple Choice)

4.8/5 (35)

Jack Hemmings bought a 3-month British pound futures contract for $1.4400/£ only to see the dollar appreciate to a value of $1.4250 at which time he sold the pound futures.If each pound futures contract is for an amount of £62,500,how much money did Jack gain or lose from his speculation with pound futures?

(Multiple Choice)

4.7/5 (34)

Why are foreign currency futures contracts more popular with individuals and banks while foreign currency forwards are more popular with businesses?

(Essay)

4.9/5 (39)

A foreign currency ________ option gives the holder the right to ________ a foreign currency whereas a foreign currency ________ option gives the holder the right to ________ an option.

(Multiple Choice)

4.8/5 (38)

Instruction 8.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 8.1.Choosing strategy #2 will

(Multiple Choice)

4.7/5 (38)

Futures contracts require that the purchaser deposit an initial sum as collateral.This deposit is called a

(Multiple Choice)

4.9/5 (48)

The most widely used reference rate for standardized quotations,loan agreements,or financial derivative valuations is the ________.

(Multiple Choice)

4.8/5 (44)

A firm with fixed-rate debt that expects interest rates to fall may engage in a swap agreement to

(Multiple Choice)

4.8/5 (41)

Instruction 8.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 8.1.After the fact,under which set of circumstances would you prefer strategy #1? (Assume your firm is borrowing money.)

(Multiple Choice)

4.7/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)