Exam 8: Foreign Currency Derivatives and Swaps

Exam 1: Current Multinational Challenges and the Global Economy33 Questions

Exam 2: Financial Goals and Corporate Governance54 Questions

Exam 3: The International Monetary System54 Questions

Exam 4: The Balance of Payments57 Questions

Exam 5: Current Multinational Financial Challenges: the Credit Crisis of 2007 - 200946 Questions

Exam 6: The Foreign Exchange Market57 Questions

Exam 7: International Parity Conditions56 Questions

Exam 8: Foreign Currency Derivatives and Swaps65 Questions

Exam 9: Foreign Exchange Rate Determination and Forecasting53 Questions

Exam 10: Transaction and Translation Exposure69 Questions

Exam 11: Operating Exposure54 Questions

Exam 12: The Global Cost and Availability of Capital57 Questions

Exam 13: Sourcing Equity and Debt Globally80 Questions

Exam 14: Multinational Tax Management57 Questions

Exam 15: Foreign Direct Investment and Political Risk55 Questions

Exam 16: Multinational Capital Budgeting and Cross-Border Acquisitions56 Questions

Exam 17: International Portfolio Theory and Diversification57 Questions

Exam 18: Working Capital Management63 Questions

Exam 19: International Trade Finance61 Questions

Select questions type

Currency futures contracts have become standard fare and trade readily in the world money centers.

(True/False)

4.8/5  (34)

(34)

The main advantage(s)of over-the-counter foreign currency options over exchange traded options is(are)

(Multiple Choice)

4.8/5 (31)

How does counterparty risk influence a firm's decision to trade exchange-traded derivatives rather than over-the-counter derivatives?

(Essay)

4.9/5 (41)

Which of the following is NOT a difference between a currency futures contract and a forward contract?

(Multiple Choice)

4.7/5 (39)

Compare and contrast foreign currency options and futures.Identify situations when you may prefer one vs.the other when speculating on foreign exchange.

(Essay)

4.9/5 (30)

An agreement to swap a fixed interest payment for a floating interest payment would be considered a/an ________.

(Multiple Choice)

4.9/5 (38)

Which of the following is NOT a factor in determining the price of a currency option?

(Multiple Choice)

4.7/5 (39)

Assume that a call option has an exercise price of $1.50/³.At a spot price of $1.45/³,the call option has ________.

(Multiple Choice)

4.9/5 (35)

A speculator that has ________ a futures contract has taken a ________ position.

(Multiple Choice)

4.9/5 (36)

About ________ of all futures contracts are settled by physical delivery of foreign exchange between buyer and seller.

(Multiple Choice)

4.8/5 (37)

An ________ option can be exercised only on its expiration date,whereas an ________ option can be exercised anytime between the date of writing up to and including the exercise date.

(Multiple Choice)

4.9/5 (39)

Polaris Inc.has a significant amount of bonds outstanding denominated in yen because of the attractive variable rate available to the firm in yen when the loan was made.However,Polaris does not have significant receivables in yen.Options available to Polaris to consider the risk of such a loan include which one of the following?

(Multiple Choice)

4.7/5 (40)

A call option whose exercise price exceeds the spot rate is said to be ________.

(Multiple Choice)

4.7/5 (43)

Financial derivatives are powerful tools that can be used by management for purposes of

(Multiple Choice)

4.8/5 (42)

A/an ________ is a contract to lock in today interest rates over a given period of time.

(Multiple Choice)

4.7/5 (44)

A foreign currency ________ contract calls for the future delivery of a standard amount of foreign exchange at a fixed time,place,and price.

(Multiple Choice)

4.8/5 (45)

Which of the following is NOT a contract specification for currency futures trading on an organized exchange?

(Multiple Choice)

4.8/5 (37)

Instruction 8.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 8.1.If your firm felt very confident that interest rates would fall or,at worst,remain at current levels,and were very confident about the firm's credit rating for the next 10 years,which strategy (strategies)would you likely choose? (Assume your firm is borrowing money.)

(Multiple Choice)

4.9/5 (35)

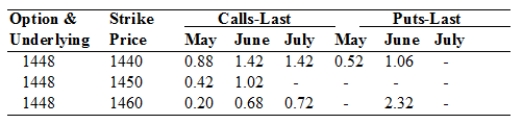

TABLE 8.1

Use the below mentioned table to answer the following question(s).

April 19, 2010, British Pound Option Prices (cents per pound, 62,500 pound contracts).

-Refer to Table 8.1.The exercise price of ________ giving the purchaser the right to sell pounds in June has a cost per pound of ________ for a total price of ________.

-Refer to Table 8.1.The exercise price of ________ giving the purchaser the right to sell pounds in June has a cost per pound of ________ for a total price of ________.

(Multiple Choice)

4.7/5 (32)

TABLE 8.1

Use the below mentioned table to answer the following question(s).

April 19, 2010, British Pound Option Prices (cents per pound, 62,500 pound contracts).

-Refer to Table 8.1.What was the closing price of the British pound on April 18,2010?

(Multiple Choice)

4.7/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)