Exam 6: Audit Planning, understanding the Client, assessing Risks, and Responding

Exam 1: The Role of the Public Accountant in the American Economy56 Questions

Exam 2: Professional Standards69 Questions

Exam 3: Professional Ethics76 Questions

Exam 4: Legal Liability of Cpas61 Questions

Exam 5: Audit Evidence and Documentation92 Questions

Exam 6: Audit Planning, understanding the Client, assessing Risks, and Responding84 Questions

Exam 7: Internal Control97 Questions

Exam 8: Consideration of Internal Control in an Information Technology Environment76 Questions

Exam 9: Audit Sampling91 Questions

Exam 10: Cash and Financial Investments69 Questions

Exam 11: Accounts Receivable, notes Receivable, and Revenue73 Questions

Exam 12: Inventories and Cost of Goods Sold64 Questions

Exam 13: Property,plant,and Equipment: Depreciation and Depletion46 Questions

Exam 14: Accounts Payable and Other Liabilities57 Questions

Exam 15: Debt and Equity Capital45 Questions

Exam 16: Auditing Operations and Completing the Audit83 Questions

Exam 17: Auditors Reports73 Questions

Exam 18: Integrated Audits of Public Companies49 Questions

Exam 19: Additional Assurance Services: Historical Financial Information65 Questions

Exam 20: Additional Assurance Services: Other Information55 Questions

Exam 21: Internal, operational, and Compliance Auditing51 Questions

Select questions type

A predecessor auditor will ordinarily initiate communication with the successor auditor: Prior to the Successor's Acceptance of the Engagement Subsequent to the Successor's Acceptance of the Engagement A. Yes Yes B. Yes No C. No Yes D. No No

(Multiple Choice)

4.8/5  (32)

(32)

The auditors' understanding established with a client should be confirmed through a(an):

(Multiple Choice)

4.8/5 (37)

Auditors perform various tasks in planning an audit engagement.Provide an overall description of how each task is performed and its purpose.

a.Obtain an understanding of the client's business.

b.Assess audit risk and materiality for the engagement.

c.Assess fraud risk.

d.Assess the risk of material misstatement of assertions about financial statement accounts and classes of transactions.

(Essay)

4.8/5 (37)

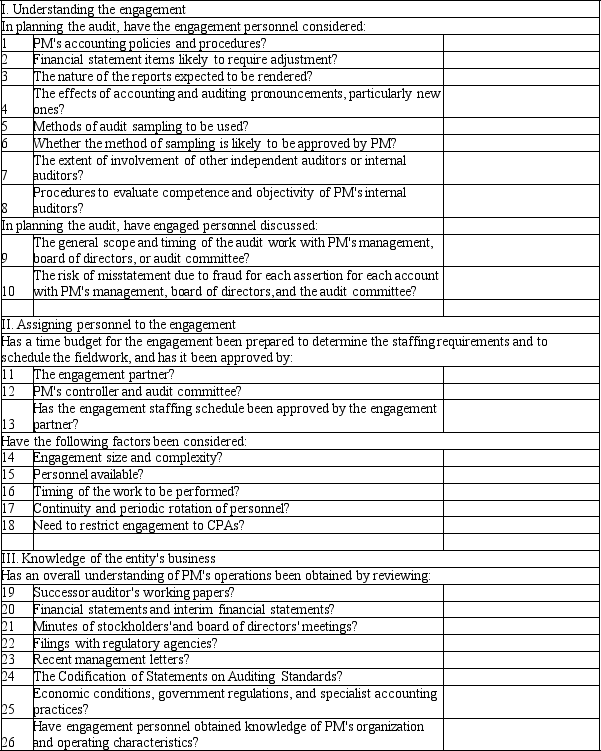

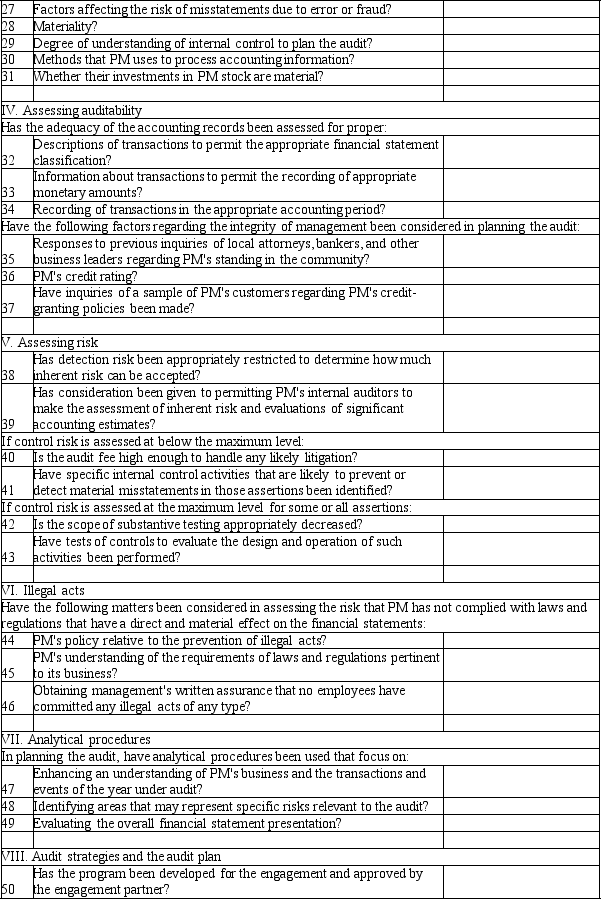

On September 3,20X1,Larkin,CPA,was engaged to audit the financial statements of Precious Metals Co.(PM),for the year ended October 31,20X1.PM purchases precious metals at wholesale prices and resells them to craft clubs at retail.PM is a new client whose common stock was first offered to the public five years ago.PM received an unqualified opinion on its financial statements in each of the prior three years,but changes auditors after each engagement.In accepting the engagement,Larkin completed all of the appropriate client acceptance procedures.

Larkin instructed Johnson,an assistant on the engagement,to draft a planning checklist that would assist Larkin in preparing the audit staff for the fieldwork that is scheduled to begin on October 17,20X1.On October 5,20X1,Johnson prepared the planning checklist below (engagement letter points have been omitted).Indicate the inappropriate points that are included on Johnson's planning checklist.

(Essay)

4.8/5 (40)

Which of the following would be least likely to be considered an audit planning procedure?

(Multiple Choice)

4.8/5 (27)

Auditors must assess fraud risk on every audit and respond to the risks that are identified.Which of the following is not a procedure required to further address the fraud risk of management override of internal control?

(Multiple Choice)

4.8/5 (35)

A successor auditor is required to make an effort to communicate with the predecessor auditor prior to:

(Multiple Choice)

4.9/5 (36)

Analytical procedures are seldom used during the risk assessment stage of an audit engagement because they are substantive procedures.

(True/False)

4.9/5 (37)

Tracing from source documents forward to ledgers is most likely to address which assertion related to posted entries?

(Multiple Choice)

4.8/5 (35)

Audit committee members need not be independent as long as they are financial experts.

(True/False)

4.8/5 (43)

Which of the following procedures is not performed as a part of planning an audit engagement?

(Multiple Choice)

4.8/5 (38)

What is a potential successor auditor's responsibility for communicating with the predecessor auditors when dealing with a prospective new client?

(Multiple Choice)

4.8/5 (39)

An abnormal fluctuation in gross profit suggests the need for extended audit procedures for sales and inventories.This would most likely be identified in the audit risk assessment phase by utilizing:

(Multiple Choice)

4.9/5 (40)

Which of the following statements is correct regarding the auditor's determination of materiality for a public company audit?

(Multiple Choice)

4.8/5 (41)

To test for unsupported entries in the journals,the direction of audit testing should be to the:

(Multiple Choice)

4.9/5 (45)

Which of the following factors would most likely cause a CPA to decide not to accept a new audit engagement?

(Multiple Choice)

4.8/5 (36)

Which of the following situations would cause a CPA to not accept a new audit engagement?

(Multiple Choice)

4.9/5 (36)

Tests for unrecorded assets typically involve tracing from:

(Multiple Choice)

4.8/5 (38)

Vouching the acquisition of assets is an audit procedure that is often performed to establish the existence of the assets.

(True/False)

4.8/5 (34)

Which of the following topics is not normally included in an engagement letter?

(Multiple Choice)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)