Exam 7: Foreign Currency Derivatives and Swaps

Exam 1: Multinational Financial Management: Opportunities and Challenges39 Questions

Exam 2: The International Monetary System61 Questions

Exam 3: The Balance of Payments57 Questions

Exam 4: Financial Goals and Corporate Governance57 Questions

Exam 5: The Foreign Exchange Market61 Questions

Exam 6: International Parity Conditions61 Questions

Exam 7: Foreign Currency Derivatives and Swaps70 Questions

Exam 8: Foreign Exchange Rate Determination58 Questions

Exam 9: Transaction Exposure43 Questions

Exam 10: Translation Exposure37 Questions

Exam 11: Operating Exposure58 Questions

Exam 12: The Global Cost and Availability of Capital63 Questions

Exam 13: Raising Equity and Debt Globally96 Questions

Exam 14: Multinational Tax Management61 Questions

Exam 15: International Trade Finance65 Questions

Exam 16: Foreign Direct Investment and Political Risk58 Questions

Exam 17: Multinational Capital Budgeting and Cross-Border Acquisitions52 Questions

Select questions type

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

• Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

• Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

• Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

-Refer to Instruction 7.1. Choosing strategy #1 will

(Multiple Choice)

4.9/5  (41)

(41)

Which of the following would be considered an example of a currency swap?

(Multiple Choice)

4.9/5 (30)

An option whose exercise price is equal to the spot rate is said to be

(Multiple Choice)

4.7/5 (35)

The time value is asymmetric in value as you move away from the strike price. (i.e., the time value at two cents above the strike price is not necessarily the same as the time value two cents below the strike price.)

(True/False)

4.9/5 (38)

Why are foreign currency futures contracts more popular with individuals and banks while foreign currency forwards are more popular with businesses?

(Essay)

4.9/5 (33)

A foreign currency ________ contract calls for the future delivery of a standard amount of foreign exchange at a fixed time, place, and price.

(Multiple Choice)

4.7/5 (35)

A speculator that has ________ a futures contract has taken a ________ position.

(Multiple Choice)

4.9/5 (48)

Which of the following is NOT a contract specification for currency futures trading on an organized exchange?

(Multiple Choice)

4.7/5 (34)

A foreign currency ________ option gives the holder the right to ________ a foreign currency whereas a foreign currency ________ option gives the holder the right to ________ an option.

(Multiple Choice)

4.8/5 (38)

The price at which an option can be exercised is called the

(Multiple Choice)

4.8/5 (31)

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

• Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

• Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

• Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

-Refer to Instruction 7.1. The risk of strategy #1 is that interest rates might go down or that your credit rating might improve. The risk of strategy #2 is (Assume your firm is borrowing money.)

(Multiple Choice)

4.8/5 (40)

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

• Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

• Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

• Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

-Refer to Instruction 7.1. The risk of strategy #1 is that interest rates might go down or that your credit rating might improve. What is the risk of strategy #3? (Assume your firm is borrowing money.)

(Multiple Choice)

5.0/5 (36)

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

• Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

• Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

• Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

-Refer to Instruction 7.1. Choosing strategy #3 will

(Multiple Choice)

4.8/5 (31)

A call option whose exercise price is less than the spot rate is said to be

(Multiple Choice)

4.8/5 (34)

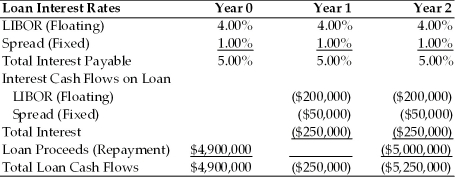

TABLE 7.2

Use the information for Polaris Corporation to answer the following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer to Table 7.2. What portion of the cost of the loan is at risk of changing?

-Refer to Table 7.2. What portion of the cost of the loan is at risk of changing?

(Multiple Choice)

4.8/5 (48)

Futures contracts require that the purchaser deposit an initial sum as collateral. This deposit is called a

(Multiple Choice)

4.7/5 (33)

About ________ of all futures contracts are settled by physical delivery of foreign exchange between buyer and seller.

(Multiple Choice)

4.8/5 (30)

TABLE 7.2

Use the information for Polaris Corporation to answer the following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer to Table 7.2. If the LIBOR rate jumps to 5.00% after the first year what will be the all-in-cost (i.e. the internal rate of return) for Polaris for the entire loan?

(Multiple Choice)

4.7/5 (33)

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

• Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

• Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

• Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

-Refer to Instruction 7.1. Which strategy (strategies) will eliminate credit risk?

(Multiple Choice)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)