Exam 7: Efficiency, Exchange, and the Invisible Hand in Action

Exam 1: Thinking Like an Economist142 Questions

Exam 2: Comparative Advantage163 Questions

Exam 3: Supply and Demand181 Questions

Exam 4: Elasticity154 Questions

Exam 5: Demand144 Questions

Exam 6: Perfectly Competitive Supply159 Questions

Exam 7: Efficiency, Exchange, and the Invisible Hand in Action159 Questions

Exam 8: Monopoly, Oligopoly, and Monopolistic Competition147 Questions

Exam 9: Games and Strategic Behavior150 Questions

Exam 10: An Introduction to Behavioral Economics111 Questions

Exam 11: Externalities, Property Rights, and the Environment184 Questions

Exam 12: The Economics of Information127 Questions

Exam 13: Labor Markets, Poverty, and Income Distribution138 Questions

Exam 14: Public Goods and Tax Policy142 Questions

Exam 15: International Trade and Trade Policy164 Questions

Exam 16: Macroeconomics: The Birds Eye View of the Economy154 Questions

Exam 17: Measuring Economic Activity: GDP and Unemployment210 Questions

Exam 18: Measuring the Price Level and Inflation160 Questions

Exam 19: Economic Growth, Productivity, and Living Standards158 Questions

Exam 20: The Labor Market: Workers, Wages, and Unemployment121 Questions

Exam 21: Saving and Capital Formation144 Questions

Exam 22: Money Prices and the Federal Reserve107 Questions

Exam 23: Financial Markets and International Capital Flows104 Questions

Exam 24: Short-Term Economic Fluctuations: An Introduction124 Questions

Exam 25: Spending and Output in the Short Run146 Questions

Exam 26: Stabilizing the Economy: The Role of the Fed162 Questions

Exam 27: Aggregate Demand, Aggregate Supply, and Inflation159 Questions

Exam 28: Exchange Rates and the Open Economy157 Questions

Select questions type

If all firms in a perfectly competitive industry are earning a normal profit, then:

(Multiple Choice)

4.9/5  (35)

(35)

Which of the following is an example of the rationing function of price?

(Multiple Choice)

4.9/5 (40)

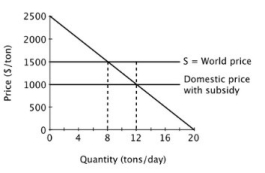

Suppose a small island nation imports sugar for its population at the world price of $1,500 per ton. The domestic market for sugar is shown below.

If the government provides a subsidy of $500 per ton, then consumer surplus will be ________ per day.

If the government provides a subsidy of $500 per ton, then consumer surplus will be ________ per day.

(Multiple Choice)

4.9/5 (35)

Last year Christine worked as a consultant. She hired an administrative assistant for $15,000 per year and rented office space (utilities included)for $3,000 per month. Her total revenue for the year was $100,000. If Christine hadn't worked as a consultant, she would have worked at a real estate firm earning $40,000 a year. Christine's opportunity cost of working as a consultant last year was ________.

(Multiple Choice)

4.7/5 (41)

Which of the following is NOT necessarily true in a market equilibrium?

(Multiple Choice)

4.8/5 (34)

If all firms in a perfectly competitive industry are experiencing economic losses, then:

(Multiple Choice)

4.8/5 (36)

In perfectly competitive markets, an implication of entry and exit in response to economic profit and loss is that:

(Multiple Choice)

4.8/5 (35)

Suppose a small island nation imports sugar for its population at the world price of $1,500 per ton. The domestic market for sugar is shown below.  With no subsidy, what is consumer surplus?

With no subsidy, what is consumer surplus?

(Multiple Choice)

4.9/5 (34)

If resources are misallocated in a perfectly competitive market, then, in the long run, profit opportunities will:

(Multiple Choice)

4.9/5 (39)

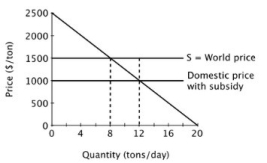

Refer to the figure below.  If this market is unregulated, the economic surplus received by consumers is:

If this market is unregulated, the economic surplus received by consumers is:

(Multiple Choice)

4.8/5 (37)

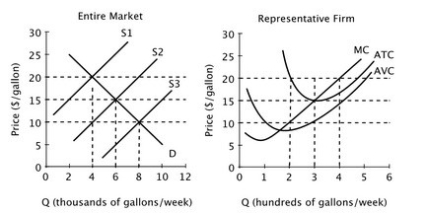

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If the market supply curve is given by S3, then what will happen to the market supply curve in the long run?

If the market supply curve is given by S3, then what will happen to the market supply curve in the long run?

(Multiple Choice)

4.7/5 (40)

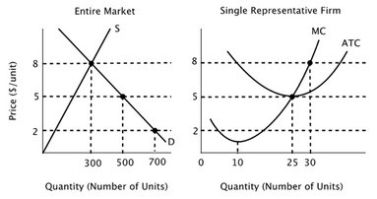

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves.  The long-run market equilibrium quantity in this industry is:

The long-run market equilibrium quantity in this industry is:

(Multiple Choice)

4.8/5 (40)

In an industry with free entry and exit, positive economic profit:

(Multiple Choice)

4.8/5 (34)

Refer to the figure below.  If a price ceiling were imposed at $4, producer surplus would be:

If a price ceiling were imposed at $4, producer surplus would be:

(Multiple Choice)

4.9/5 (36)

One assumption of the perfectly competitive model is free entry and exit. This assumption most directly leads to the implication that:

(Multiple Choice)

4.7/5 (35)

If the demand curve fails to capture all of the benefits of consumption, then the:

(Multiple Choice)

4.9/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)