Exam 7: Efficiency, Exchange, and the Invisible Hand in Action

Exam 1: Thinking Like an Economist142 Questions

Exam 2: Comparative Advantage163 Questions

Exam 3: Supply and Demand181 Questions

Exam 4: Elasticity154 Questions

Exam 5: Demand144 Questions

Exam 6: Perfectly Competitive Supply159 Questions

Exam 7: Efficiency, Exchange, and the Invisible Hand in Action159 Questions

Exam 8: Monopoly, Oligopoly, and Monopolistic Competition147 Questions

Exam 9: Games and Strategic Behavior150 Questions

Exam 10: An Introduction to Behavioral Economics111 Questions

Exam 11: Externalities, Property Rights, and the Environment184 Questions

Exam 12: The Economics of Information127 Questions

Exam 13: Labor Markets, Poverty, and Income Distribution138 Questions

Exam 14: Public Goods and Tax Policy142 Questions

Exam 15: International Trade and Trade Policy164 Questions

Exam 16: Macroeconomics: The Birds Eye View of the Economy154 Questions

Exam 17: Measuring Economic Activity: GDP and Unemployment210 Questions

Exam 18: Measuring the Price Level and Inflation160 Questions

Exam 19: Economic Growth, Productivity, and Living Standards158 Questions

Exam 20: The Labor Market: Workers, Wages, and Unemployment121 Questions

Exam 21: Saving and Capital Formation144 Questions

Exam 22: Money Prices and the Federal Reserve107 Questions

Exam 23: Financial Markets and International Capital Flows104 Questions

Exam 24: Short-Term Economic Fluctuations: An Introduction124 Questions

Exam 25: Spending and Output in the Short Run146 Questions

Exam 26: Stabilizing the Economy: The Role of the Fed162 Questions

Exam 27: Aggregate Demand, Aggregate Supply, and Inflation159 Questions

Exam 28: Exchange Rates and the Open Economy157 Questions

Select questions type

The statement, "If a deal is too good to be true, then it probably is not true," is most closely related to which core economic principle?

(Multiple Choice)

4.9/5  (30)

(30)

If the market supply curve does not capture all of the costs to society of producing an additional unit of good, then:

(Multiple Choice)

4.9/5 (36)

The role that prices play in directing resources away from overcrowded markets and towards markets that are underserved is known as the ________ function of price.

(Multiple Choice)

4.7/5 (36)

Suppose a market is in equilibrium. The area below the market price and above the supply curve is:

(Multiple Choice)

4.9/5 (36)

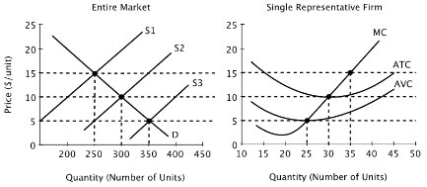

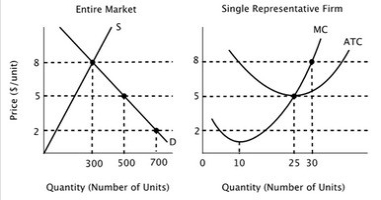

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If the market supply curve is given by S1, then in the long run firms will:

If the market supply curve is given by S1, then in the long run firms will:

(Multiple Choice)

4.9/5 (33)

If you were to start your own business, your implicit costs would include the:

(Multiple Choice)

4.9/5 (48)

Consider a perfectly competitive industry in a long-run equilibrium. If a single firm in that industry discovers a significant cost-saving production technology, then:

(Multiple Choice)

4.9/5 (41)

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  In the long run, there will be ________ firms in this market.

In the long run, there will be ________ firms in this market.

(Multiple Choice)

4.8/5 (37)

Suppose the market for coffee is in equilibrium at a price of $5 per pound. This means that:

(Multiple Choice)

4.9/5 (43)

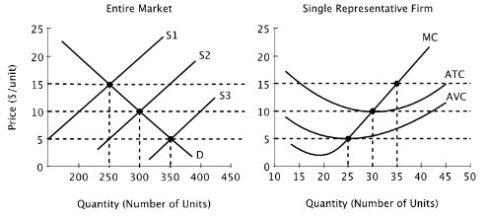

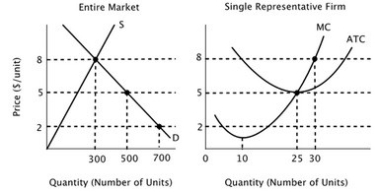

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves.  Given that the current equilibrium price is $8, what will happen to the number of firms in this market in the long run?

Given that the current equilibrium price is $8, what will happen to the number of firms in this market in the long run?

(Multiple Choice)

4.9/5 (37)

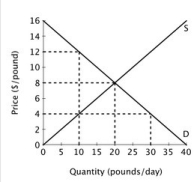

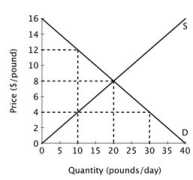

The figure below shows the supply and demand curves for oranges in Smallville.  At a price of $4 per pound there will be an excess ________ of ________ pounds of oranges per day.

At a price of $4 per pound there will be an excess ________ of ________ pounds of oranges per day.

(Multiple Choice)

4.7/5 (38)

If a firm is earning zero economic profit, then its accounting profit will:

(Multiple Choice)

4.9/5 (41)

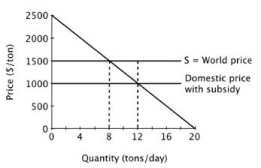

Suppose a small island nation imports sugar for its population at the world price of $1,500 per ton. The domestic market for sugar is shown below.  If the government provides a subsidy of $500 per ton, then the cost of subsidy, which must be borne by taxpayers, will be ________ per day.

If the government provides a subsidy of $500 per ton, then the cost of subsidy, which must be borne by taxpayers, will be ________ per day.

(Multiple Choice)

4.9/5 (34)

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves.  In the long run equilibrium in this market:

In the long run equilibrium in this market:

(Multiple Choice)

4.7/5 (35)

The fact that price subsidies reduce economic surplus implies that:

(Multiple Choice)

4.9/5 (31)

A cost-saving innovation in a perfectly competitive industry will lead to:

(Multiple Choice)

5.0/5 (37)

The figure below shows the supply and demand curves for oranges in Smallville.  When this market is in equilibrium, total economic surplus is ________ per day.

When this market is in equilibrium, total economic surplus is ________ per day.

(Multiple Choice)

4.7/5 (34)

In a free market economy, the decisions of buyers and sellers are:

(Multiple Choice)

4.8/5 (38)

Which of the following best describes how a perfectly competitive industry would respond to a sudden increase in popularity of the product? The market demand curve would shift to the right, leading to:

(Multiple Choice)

4.7/5 (39)

If an individual consumer is willing to pay $11 for one unit of a good but is able to purchase it for $7, then his or her consumer surplus from the purchase of that unit would be:

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)