Exam 9: Assessing the Risk of Material Misstatement

Exam 1: The Demand for Audit and Other Assurance Services80 Questions

Exam 2: The CPA Profession101 Questions

Exam 3: Audit Reports170 Questions

Exam 4: Professional Ethics149 Questions

Exam 5: Legal Liability149 Questions

Exam 6: Audit Responsibilities and Objectives181 Questions

Exam 7: Audit Evidence166 Questions

Exam 8: Audit Planning and Materiality172 Questions

Exam 9: Assessing the Risk of Material Misstatement110 Questions

Exam 10: Fraud Auditing139 Questions

Exam 11: Internal Control and Coso Framework152 Questions

Exam 12: Assessing Control Risk and Reporting on Internal Controls104 Questions

Exam 13: Overall Audit Strategy and Audit Program119 Questions

Exam 14: Audit of the Sales and Collection Cycle: Tests of Controls140 Questions

Exam 15: Audit Sampling for Tests of Controls and Substantive Tests of Transactions151 Questions

Exam 16: Completing the Tests in the Sales and Collection Cycle: Accounts Receivable131 Questions

Exam 17: Audit Sampling for Tests of Details of Balances130 Questions

Exam 18: Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable146 Questions

Exam 19: Completing the Tests in the Acquisition and Payment Cycle: Verification of Selected Accounts128 Questions

Exam 20: Audit of the Payroll and Personnel Cycle130 Questions

Exam 21: Audit of the Inventory and Warehousing Cycle146 Questions

Exam 22: Audit of the Capital Acquisition and Repayment Cycle110 Questions

Exam 23: Audit of Cash and Financial Instruments146 Questions

Exam 24: Completing the Audit155 Questions

Exam 25: Other Assurance Services123 Questions

Exam 26: Internal and Governmental Financial Auditing and Operational Auditing98 Questions

Select questions type

Inherent risk is often high for an account such as

Free

(Multiple Choice)

4.8/5  (35)

(35)

Correct Answer: Verified

Verified

A

Some risk exists that the financial statements are not fairly stated, even when the auditor's opinion is unmodified.

Free

(True/False)

4.8/5 (38)

Correct Answer:Verified

True

Auditors typically rely on internal controls of their private company clients

Free

(Multiple Choice)

4.7/5 (35)

Correct Answer:Verified

B

Which of the following is true regarding audit risk for segments?

(Multiple Choice)

4.8/5 (41)

The performance of risk assessment procedures is designed to help the auditor obtain an understanding of the entity.

(True/False)

4.9/5 (35)

When management has an adequate level of integrity for the auditor to accept the engagement but cannot be regarded as completely honest in all dealings, auditors normally

(Multiple Choice)

4.8/5 (32)

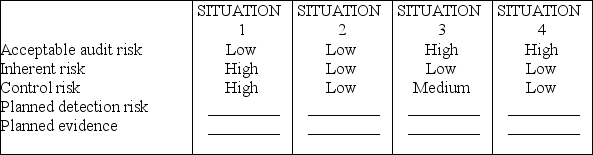

In practice, auditors rarely assign numerical probabilities to inherent risk, control risk, or acceptable audit risk. It is more common to assess these risks as high, medium, or low. For each of the four situations below, fill in the blanks for planned detection risk and the amount of evidence you would plan to gather ("planned evidence") using the terms high, medium, or low.

(Short Answer)

4.9/5 (48)

Which of the following would not increase the risks of material misstatement at the overall financial statement level?

(Multiple Choice)

4.9/5 (37)

There are several factors that affect engagement risk and, therefore, acceptable audit risk. Discuss three of these factors.

(Essay)

4.8/5 (32)

Risk assessment procedures are performed to identify and assess the risk of material misstatement. List three risk assessment procedures.

(Essay)

4.8/5 (43)

Discussions, including exchanges of ideas or brainstorming among the engagement team members about business risks should include the financial statements, but not necessarily the related disclosures.

(True/False)

4.7/5 (43)

A high detection risk equates to a low amount of audit evidence needed.

(True/False)

4.7/5 (31)

Individuals engaged in conducting a fraud will generally not misrepresent information to the auditor.

(True/False)

4.9/5 (38)

Audit reports issued under the PCAOB and the AICPA standards contain two important phrases that are directly related to materiality and to risk: obtain absolute assurance and free of material misstatement.

(True/False)

4.9/5 (23)

The auditor assesses risks at the overall financial statement level but not at the audit objective level for the acquisition and payment cycle.

(True/False)

4.8/5 (34)

When taken together, the concepts of risk and materiality in auditing

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)