Exam 2: Principles of Accounting and Financial Reporting for State and Local Governments

Exam 1: Introduction to Accounting and Financial Reporting for Government and Not-for-Profit Entities62 Questions

Exam 2: Principles of Accounting and Financial Reporting for State and Local Governments73 Questions

Exam 3: Governmental Operating Statement Accounts; Budgetary Accounting91 Questions

Exam 4: Accounting for Governmental Operating Activities–Illustrative Transactions and Financial Statements91 Questions

Exam 5: Accounting for General Capital Assets and Capital Projects83 Questions

Exam 6: Accounting for General Long-Term Liabilities and Debt Service75 Questions

Exam 7: Accounting for the Business-type Activities of State and Local Governments75 Questions

Exam 8: Accounting for Fiduciary Activities—Custodial and Trust Funds72 Questions

Exam 9: Financial Reporting of State and Local Governments66 Questions

Exam 10: Analysis of Government Financial Performance60 Questions

Exam 11: Auditing of Government and Not-for-Profit Organizations65 Questions

Exam 12: Budgeting and Performance Measurement60 Questions

Exam 13: Not-for-Profit Organizations—Regulatory, Taxation, and Performance Issues59 Questions

Exam 14: Accounting for Not-for-Profit Organizations77 Questions

Exam 15: Accounting for Colleges and Universities63 Questions

Exam 16: Accounting for Health Care Organizations63 Questions

Exam 17: Accounting and Reporting for the Federal Government66 Questions

Select questions type

There are four major activity categories reported by state and local governments: governmental, government-wide, proprietary, and fiduciary.

(True/False)

4.7/5  (35)

(35)

A deferred inflow of resources is defined as "an acquisition of net assets by the government that is applicable to a future reporting period."

(True/False)

4.8/5 (31)

The positive fund balance in a special revenue fund must at a minimum be reported as assigned.

(True/False)

4.9/5 (30)

Which of the following is not a characteristic of a fund as defined by GASB standards?

(Multiple Choice)

4.9/5 (31)

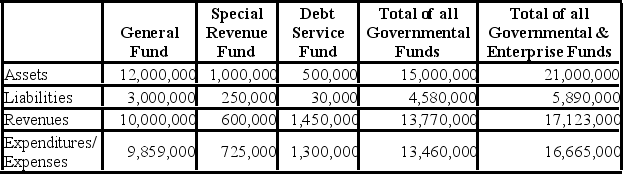

Use the following information to determine whether the Development Special Revenue and the Debt Service Funds should be reported as major funds based on asset amounts provided. Development Special Revenue Fund Assets \ 740,000 Debt Service Fund Assets \ 150,000 Total Governmental Fund Assets \ 7,500,000 Total Governmental Fund and Enterprise Fund Assets \ 8,750,000

(Multiple Choice)

5.0/5 (35)

According to GASB Concepts Statement 1 a primary objective of financial reports is to provide information useful in determining the accountability of the government.

(True/False)

4.9/5 (38)

Revenues is an example of what the GASB terms an inflow of resources.

(True/False)

4.9/5 (35)

Which of the following is not one of the seven elements defined by the GASB concept statements?

(Multiple Choice)

4.8/5 (34)

Because budgetary accounts are used by governments, government financial statements can never be said to be in accord with generally accepted accounting principles.

(True/False)

4.9/5 (41)

Following are some of the county's governmental funds. The county has asked you to determine is any of the funds listed should be classified as major funds based on the GASB size criteria. Clearly indicate which fund(s) you believe should be classified as major and provide support for your choice(s).

(Essay)

4.8/5 (40)

According to the GASB, information that is essential and useful to placing information in the correct context should be reported as which of the following?

(Multiple Choice)

4.8/5 (34)

The governmental funds category includes the General Fund, special revenue funds, debt service funds, capital projects funds, and internal service funds.

(True/False)

4.8/5 (40)

Economic resources are cash or items expected to be converted into cash during the current period, or soon enough thereafter to pay current period liabilities.

(True/False)

5.0/5 (36)

Which of the following would be reported as a nonspendable fund balance?

(Multiple Choice)

4.8/5 (41)

Explain the nature of the three major activity categories of a state or local government: governmental activities, business-type activities, and fiduciary activities. Provide examples of each.

(Essay)

4.9/5 (33)

A debt service fund is used to account for financial resources segregated for the purpose of making principal and interest payments on general long-term debt.

(True/False)

4.9/5 (48)

Which of the following governmental funds must be reported as a major fund?

(Multiple Choice)

4.9/5 (31)

Which of the following is not one of the methods recommended by the GASB Concepts Statement 3 for communicating information to external users of government financial reports?

(Multiple Choice)

4.7/5 (36)

According to the guidance of GASB Concepts Statement 3, financial information can be communicated by recognition in the financial statements, disclosure in the notes to the financial statements, presentation as required supplementary information, or presentation as supplementary information.

(True/False)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)