Exam 12: An Alternative View of Risk and Return: The Arbitrage Pricing Theory

Exam 1: Introduction to Corporate Finance67 Questions

Exam 2: Financial Statements and Cash Flow94 Questions

Exam 3: Financial Statements Analysis and Financial Models120 Questions

Exam 4: Discounted Cash Flow Valuation134 Questions

Exam 5: Net Present Value and Other Investment Rules105 Questions

Exam 6: Making Capital Investment Decisions101 Questions

Exam 7: Risk Analysis, Real Options, and Capital Budgeting99 Questions

Exam 8: Interest Rates and Bond Valuation69 Questions

Exam 9: Stock Valuation77 Questions

Exam 10: Risk and Return: Lessons From Market History84 Questions

Exam 11: Return and Risk: the Capital Asset Pricing Model Capm136 Questions

Exam 12: An Alternative View of Risk and Return: The Arbitrage Pricing Theory51 Questions

Exam 13: Risk, Cost of Capital, and Valuation59 Questions

Exam 14: Efficient Capital Markets and Behavioral Challenges65 Questions

Exam 15: Long-Term Financing46 Questions

Exam 16: Capital Structure: Basic Concepts91 Questions

Exam 17: Capital Structure: Limits to the Use of Debt74 Questions

Exam 18: Valuation and Capital Budgeting for the Levered Firm57 Questions

Exam 19: Dividends and Other Payouts90 Questions

Exam 20: Raising Capital73 Questions

Exam 21: Leasing55 Questions

Exam 22: Options and Corporate Finance95 Questions

Exam 23: Options and Corporate Finance: Extensions and Applications46 Questions

Exam 24: Warrants and Convertibles58 Questions

Exam 25: Derivatives and Hedging Risk66 Questions

Exam 26: Short-Term Finance and Planning124 Questions

Exam 27: Cash Management59 Questions

Exam 28: Credit and Inventory Management61 Questions

Exam 29: Mergers, Acquisitions, and Divestitures83 Questions

Exam 30: Financial Distress52 Questions

Exam 31: International Corporate Finance95 Questions

Select questions type

Shareholders discount many corporate announcements because of their prior expectations. If an announcement causes the price to change it will mostly be driven by:

(Multiple Choice)

4.8/5  (42)

(42)

If the expected rate of inflation was 3% and the actual rate was 6.2%; the systematic response coefficient from inflation,βI,would result in a change in any security return of ___ βI.

(Multiple Choice)

4.8/5 (35)

Suppose that we have identified three important systematic risk factors given by exports,inflation,and industrial production. In the beginning of the year,growth in these three factors is estimated at -1%,2.5%,and 3.5% respectively. However,actual growth in these factors turns out to be 1%,-2%,and 2%. The factor betas are given by βEX = 1.8,βI = 0.7,and βIP = 1.0. If the expected return on the stock is 6%,and no unexpected news concerning the stock surfaces,calculate the stock's total return.

(Multiple Choice)

4.7/5 (39)

For a diversified portfolio including a large number of stocks,the:

(Multiple Choice)

4.8/5 (34)

Both the APT and the CAPM imply a positive relationship between expected return and risk. The APT views risk:

(Multiple Choice)

4.8/5 (35)

Discuss the Fama-French three factor model; both what it means and the factors of the model.

(Essay)

4.8/5 (36)

Suppose that we have identified three important systematic risk factors given by exports,inflation,and industrial production. In the beginning of the year,growth in these three factors is estimated at -1%,2.5%,and 3.5% respectively. However,actual growth in these factors turns out to be 1%,-2%,and 2%. The factor betas are given by βEX = 1.8,βI = 0.7,and βIP = 1.0. Calculate the stock's total return if the company announces that they had an industrial accident and the operating facilities will close down for some time thus resulting in a loss by the company of 7% in return.

(Multiple Choice)

4.9/5 (37)

The single factor APT model that resembles the market model uses _________ as the single factor.

(Multiple Choice)

4.8/5 (33)

The systematic response coefficient for productivity,βp,would produce an unexpected change in any security return of ____ βP if the expected rate of productivity was 1.5% and the actual rate was 2.25%.

(Multiple Choice)

4.9/5 (35)

You have a 3 factor model to explain returns. Explain what a factor represents in the context of the APT?

Each factor is multiplied by a beta. What do these represent and how do they relate to the actual return?

(Essay)

4.8/5 (41)

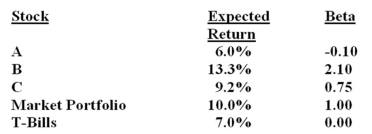

An investor is considering the three stocks given below:

Calculate the expected return and beta of a portfolio equally weighted between stocks B and C. Demonstrate that holding stock A actually reduces risk by comparing the risk of a portfolio equally weighted between stock B and T-Bills with a portfolio equally weighted between stocks B and A.

Calculate the expected return and beta of a portfolio equally weighted between stocks B and C. Demonstrate that holding stock A actually reduces risk by comparing the risk of a portfolio equally weighted between stock B and T-Bills with a portfolio equally weighted between stocks B and A.

(Essay)

4.9/5 (31)

Assume that the single factor APT model applies and a portfolio exists such that 1/2 of the funds are invested in Security Q and the rest in the risk-free asset. Security Q has a beta of 1.8. The portfolio has a beta of:

(Multiple Choice)

4.7/5 (38)

A growth stock portfolio and a value portfolio might be characterized:

(Multiple Choice)

4.7/5 (32)

Assuming that the single factor APT model applies,the beta for the market portfolio is:

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)