Exam 33: Aggregate Demand and Aggregate Supply

Exam 1: Ten Principles of Economics281 Questions

Exam 2: Thinking Like an Economist451 Questions

Exam 3: Interdependence and the Gains From Trade353 Questions

Exam 4: The Market Forces of Supply and Demand467 Questions

Exam 5: Elasticity and Its Application409 Questions

Exam 6: Supply, Demand, and Government Policies459 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets363 Questions

Exam 8: Application: The Costs of Taxation353 Questions

Exam 9: Application: International Trade333 Questions

Exam 10: Externalities352 Questions

Exam 11: Public Goods and Common Resources270 Questions

Exam 12: The Design of the Tax System397 Questions

Exam 13: The Costs of Production434 Questions

Exam 14: Firms in Competitive Markets381 Questions

Exam 15: Monopoly427 Questions

Exam 16: Monopolistic Competition416 Questions

Exam 17: Oligopoly325 Questions

Exam 18: The Markets for the Factors of Production361 Questions

Exam 19: Earnings and Discrimination335 Questions

Exam 20: Income Inequality and Poverty312 Questions

Exam 21: The Theory of Consumer Choice354 Questions

Exam 22: Frontiers of Microeconomics262 Questions

Exam 23: Measuring a Nations Income343 Questions

Exam 24: Measuring the Cost of Living358 Questions

Exam 25: Production and Growth335 Questions

Exam 26: Saving, investment, and the Financial System381 Questions

Exam 27: The Basic Tools of Finance336 Questions

Exam 28: Unemployment533 Questions

Exam 29: The Monetary System366 Questions

Exam 30: Money Growth and Inflation312 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts346 Questions

Exam 32: A Macroeconomic Theory of the Open Economy300 Questions

Exam 33: Aggregate Demand and Aggregate Supply386 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand334 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment306 Questions

Exam 36: Five Debates Over Macroeconomic Policy179 Questions

Select questions type

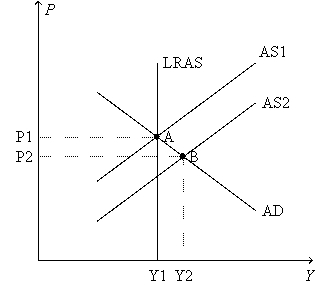

Figure 33-2.  -Refer to Figure 33-2.Starting from point B and assuming that aggregate demand is held constant,in the long run the economy is likely to experience

-Refer to Figure 33-2.Starting from point B and assuming that aggregate demand is held constant,in the long run the economy is likely to experience

(Multiple Choice)

4.8/5  (36)

(36)

Other things the same,as the price level rises,the real value of a dollar

(Multiple Choice)

4.9/5 (24)

The sticky-wage theory of the short-run aggregate supply curve says that the quantity of output firms supply will increase if

(Multiple Choice)

4.8/5 (37)

Most economists use the aggregate demand and aggregate supply model primarily to analyze

(Multiple Choice)

4.9/5 (34)

The equation: quantity of output supplied = natural rate of output + a(actual price level - expected price level),where a is a positive number,represents

(Multiple Choice)

4.8/5 (28)

An increase in the expected price level shifts short-run aggregate supply to the

(Multiple Choice)

4.8/5 (37)

All explanations for the upward slope of the short-run aggregate supply curve suppose that the quantity of output supplied increases when the actual price level exceeds the expected price level.

(True/False)

4.9/5 (38)

Which of the following shifts both short-run and long-run aggregate supply left?

(Multiple Choice)

4.7/5 (30)

The model of aggregate demand and aggregate supply explains the relationship between

(Multiple Choice)

5.0/5 (30)

Other things the same,if the long-run aggregate supply curve shifts left,prices

(Multiple Choice)

4.8/5 (39)

Suppose that a decrease in the demand for goods and services pushes the economy into recession.What happens to the price level? If the government does nothing,what ensures that the economy still eventually gets back to the natural rate of output?

(Essay)

4.9/5 (37)

During World War II government expenditures increased almost five-fold and output almost doubled.

(True/False)

5.0/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)