Exam 7: Cost Allocation: Departments, Joint Products, and By-Products

Exam 1: Cost Management and Strategy79 Questions

Exam 2: Implementing Strategy: the Value Chain, the Balanced Scorecard, and the Strategy Map70 Questions

Exam 3: Basic Cost Management Concepts98 Questions

Exam 4: Job Costing118 Questions

Exam 5: Activity-Based Costing and Customer Profitability Analysis149 Questions

Exam 6: Process Costing106 Questions

Exam 7: Cost Allocation: Departments, Joint Products, and By-Products96 Questions

Exam 8: Cost Estimation120 Questions

Exam 9: Short-Term Profit Planning: Cost-Volume-Profit Cvp Analysis105 Questions

Exam 10: Strategy and the Master Budget146 Questions

Exam 11: Decision Making With a Strategic Emphasis137 Questions

Exam 12: Strategy and the Analysis of Capital Investments167 Questions

Exam 13: Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing94 Questions

Exam 14: Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures178 Questions

Exam 15: Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management167 Questions

Exam 16: Operational Performance Measurement: Further Analysis of Productivity and Sales134 Questions

Exam 17: The Management and Control of Quality147 Questions

Exam 18: Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard133 Questions

Exam 19: Strategic Performance Measurement: Investment Centers and Transfer Pricing151 Questions

Exam 20: Management Compensation, Business Analysis, and Business Valuation108 Questions

Select questions type

Which of the following is not one of the objectives of cost allocation?

(Multiple Choice)

4.8/5  (36)

(36)

The amount of joint costs allocated to product DBB-2 using the net realizable value method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

(Multiple Choice)

4.8/5 (32)

An alternative concept of fairness in cost allocation, absent the cause-and-effect basis, includes:

(Multiple Choice)

4.8/5 (31)

A key disincentive effect of departmental cost allocation can occur when:

(Multiple Choice)

4.8/5 (46)

The amount of joint costs allocated to product N using the net realizable value method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

(Multiple Choice)

4.7/5 (29)

An overhead cost that can be traced directly to either a service or production department:

(Multiple Choice)

4.9/5 (34)

"What's the big fuss about learning three different methods of cost allocation for joint products? The total cost doesn't change, and the real question that needs answering is whether to further process joint products or sell right away. Besides, our firm uses JIT inventory, so there aren't any ending inventories to cost."

Required:

Comment on these ideas.

(Essay)

4.9/5 (33)

If a budgeted activity base is used as the base in cost allocation, each department's cost allocation will be predictable, and not influenced by the:

(Multiple Choice)

4.7/5 (42)

Relative sales value at split-off is used to allocate: Cost Beyond

(Multiple Choice)

4.8/5 (29)

The amount of joint costs allocated to product Z using the net realizable value method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

(Multiple Choice)

4.8/5 (35)

A concept which is commonly employed with allocation bases related to size is:

(Multiple Choice)

4.7/5 (36)

The amount of joint costs allocated to product DBB-2 using the sales value at split-off method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

(Multiple Choice)

4.8/5 (28)

The total cost accumulated in the finishing department using the step method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

(Multiple Choice)

4.7/5 (44)

The amount of joint costs allocated to product M using the net realizable value method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

(Multiple Choice)

4.7/5 (39)

When significant differences exist in costs allocated to production departments, cost management should use what method to find a more accurate cost allocation?

(Multiple Choice)

4.9/5 (28)

Revenue methods of by-product cost allocation are justified on financial accounting concepts of:

(Multiple Choice)

4.8/5 (31)

Cost allocation provides a service firm a basis for evaluating the:

(Multiple Choice)

4.8/5 (43)

By-product costing that uses the asset recognition method(s) creates:

(Multiple Choice)

4.8/5 (43)

The amount of joint costs allocated to product DBB-3 using the net realizable value method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

(Multiple Choice)

4.8/5 (41)

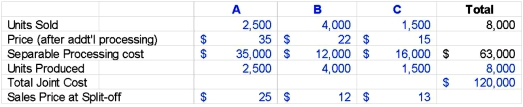

Stulce Inc. produces joint products A, B, and C from a joint process. Information concerning a batch produced in May at a joint cost of $120,000 was as follows:  Required(calculate all ratios, percentages, and unit costs to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

1. Allocate the joint costs to the joint products using the physical measures method.

2. Calculate the gross margin for each of the three products using the cost allocation for the physical unit method in part (1) above.

3. Allocate the joint costs to the joint products using the net realizable method.

4. Calculate the gross margin for each of the three products using the cost allocation for the net realizable value method in part (3) above.

Required(calculate all ratios, percentages, and unit costs to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

1. Allocate the joint costs to the joint products using the physical measures method.

2. Calculate the gross margin for each of the three products using the cost allocation for the physical unit method in part (1) above.

3. Allocate the joint costs to the joint products using the net realizable method.

4. Calculate the gross margin for each of the three products using the cost allocation for the net realizable value method in part (3) above.

(Essay)

4.8/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)