Exam 3: Basic Cost Management Concepts

A portion of the costs incurred by business organizations is designated as direct labor cost. As used in practice, the term direct labor cost has a wide variety of meanings. Unless the meaning intended in a given context is clear, misunderstanding and confusion are likely to ensue. If a user does not understand the elements included in direct labor cost, erroneous interpretations of the numbers might occur and could result in poor management decisions. Measurement of direct labor costs has two aspects: (1) the quantity of labor effort that is to be included, that is, the types of hours or other units of time that are to be counted; and (2) the unit price by which each of these quantities is multiplied to arrive at a monetary cost.

Required:

1) Distinguish between direct labor and indirect labor.

2) Presented below are labor cost elements that a company has been classified as direct labor, factory overhead, or either direct labor or factory overhead depending upon the situation.

Direct labor-Included in the company's direct labor are cost production efficiency bonuses and certain benefits for direct labor workers such as FICA (employer's portion), group life insurance, vacation pay, and workers' compensation insurance.

Factory overhead-The company's calculation of manufacturing overhead includes the cost of the following: wage continuation plans, the company sponsored cafeteria, the personnel department, and recreational facilities.

Direct labor or factory overhead-The costs that the company includes in this category are maintenance expense, overtime premiums, and shift premiums.

Explain the reasoning used by the company in classifying the cost elements in each of the three categories.

Answer may vary

Feedback: (1) Direct labor can be traced in an economically feasible manner to each output, while indirect labor cannot.

(2) Some types of labor costs (e.g., breaks and personal time) are considered common expectations (normal and unavoidable) for employees, and as such are included as costs of direct labor. In contrast, downtime, overtime, training, and the like are considered activities chosen by or managed by the company, and not normal expectations of the employee, and are thus considered indirect, or overhead. Also, many times downtime and overtime and training cannot be effectively traced to hours worked. For example, the cost of overtime due to rush orders or scheduling problems is the responsibility of management, and therefore is considered overhead (indirect) rather than a direct cost of labor. Moreover, it cannot be easily traced to output.

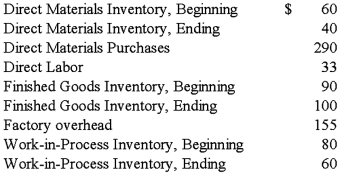

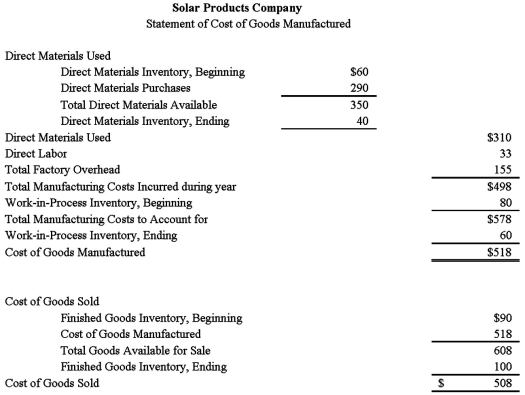

The following data relates to the Solar Products Company:  Required:

Prepare a statement of cost of goods manufactured and cost of goods sold.

Required:

Prepare a statement of cost of goods manufactured and cost of goods sold.

Answer may vary

Feedback:

Direct materials and direct labor costs total $40,000 and factory overhead costs total $100 per machine hour. If 200 machine hours were used for Job #202, what is the total manufacturing cost for Job #202?

D

What should be the amount in the finished goods inventory at the beginning of the year?

Which of the following is normally considered to be a product cost?

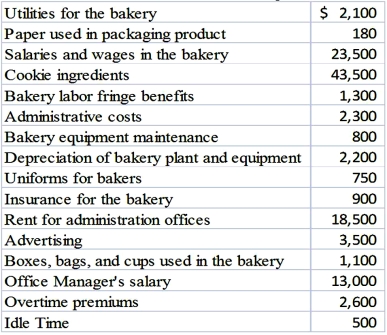

Choco Chocolata is a cookie company in Juarez, Mexico that produces and sells American-style chocolate chip cookies with extremely high quality and service. The owner would like to identify the various costs incurred during each year in order to plan and control the costs in the business. Chocolata's costs are the following (in thousands of pesos):  Required:

(1) What is the total amount of product costs?

(2) What is the total amount of period costs?

Required:

(1) What is the total amount of product costs?

(2) What is the total amount of period costs?

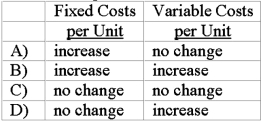

When production levels are expected to decline within a relevant range, what effects would be anticipated with respect to each of the following?

Direct materials and direct labor costs total $70,000 and factory overhead costs total $100 per machine hour. If 200 machine hours were used for Job #333, what is the total manufacturing cost for Job #333?

Since indirect cost cannot be conveniently or economically traced directly to a cost pool or cost object, the management accountant will:

Manufacturing firms use which of the following three inventory accounts?

The following information pertains to the Petrie Company:  Required: Determine the cost of goods manufactured.

Required: Determine the cost of goods manufactured.

The Gray Company has a staff of five clerks in its general accounting department. Three clerks who work during the day perform sundry accounting tasks; the two clerks who work in the evening are responsible for (1) collecting the cost data for the various jobs in process, (2) verifying manufacturing material and labor reports, and (3) supplying production reports to the supervisors by the next morning. The salaries of these two clerks who work at night should be classified as:

Complete the inventory formula: Beginning Inventory + ______ = ________ + Ending Inventory

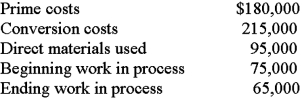

Prime cost and conversion cost share what common element of total cost?

Advanced Technical Services, Ltd. has many products and services in the medical field. The Clinical Division of the company does research and testing of consumer products on human participants in controlled clinical studies.

Required:

Determine for each cost below whether it is best classified as a fixed, variable, or step-fixed cost.

(1) Director's salary

(2) Part-time help

(3) Payment on purchase of medical equipment

(4) Allocation of company-wide advertising

(5) Patches used on participants' arms during the study

(6) Stipends paid to participants

When cost relationships are linear, total variable costs will vary in proportion to changes in:

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)