Exam 17: The Management and Control of Quality

A Cost-of-Quality (COQ) reporting format may be applicable to help support the sustainability goals of organizations. Indeed, the development of such a reporting framework would likely be viewed as a significant improvement to an organization's management accounting and control system.

Required:

1. Use your knowledge of COQ reporting to speculate on an "environmental assessment" reporting framework. This tool should identify each aspect of the organization's activities that affect the environment, in terms of both living and non-living natural systems (ecosystems), including land, water, and air. (That is, what are some of the environmental impacts that the management accounting system could assess and monitor?)

2. In the past, management accountants focused on a traditional approach to environmental risk management, wherein the focus was on ensuring regulatory compliance (EPA, etc.) in order to minimize fines, penalties, and legal costs). In today's business climate, however, more will likely be expected of the management accountant. What type of opportunities, associated with environmental performance, might the management accountant suggest to management?

No set solution to the above questions is anticipated. The following notes were taken from Statement of Management Accounting No. 67, "The Evolution of Accountability—Sustainability Reporting for Accountants," Institute of Management Accountants (2008).

(1) Examples might include the following:

● selection of raw materials, including issues such as impact of extraction and production, availability of supply, and operational impact of use (e.g., hazardous materials)

● creation of all planned waste streams, whether from manufacturing or support services, and their associated internal and external disposal costs

● creation of unplanned waste and by-products, such as emissions into the air and water

● impact of processes and indirect materials being used, on employee health and the workplace

● transportation costs of all types at all levels of both the supply stream and the output (sales and distribution streams)

● impact of design and operation of the organization's products and services on those who buy and use them and third parties.

(2) Examples might include the following opportunities:

● limiting the impact of (mandatory and voluntary) noncompliance, where such results would cause a loss in reputation and brand value

● cost avoidance in areas such as the internal costs of handling and managing toxic materials, hazardous waste, and other supplies

● minimizing healthcare costs through elimination of negative workplace consequences of environmental impacts

● reducing waste levels (scrap, excess by-products, etc.) through implementing quality initiatives, and extending this to reduction in printing costs and other support areas

● reducing (escalating) waste-disposal costs (both external, such as transportation and disposal fees, and internal, such as materials handling labor costs) through recycling initiatives (and including the creation of new business opportunities through using by-products)

● reducing product liability risks (and possible insurance coverage and legal costs) by focusing on environmental impact from the products or services produced, as part of the product-design management process

● reducing indirect costs through capital investments in areas such as waste-water reduction, electrical reduction (lights, motors, controls, improved housekeeping), oil and gas reduction, and others

● implementation of modified working practices, such as allowing employees to work at home (reduces transportation costs), using technology instead of traveling, and creating and transmitting documents electronically to avoid use of paper and power

● facilitating changes through better space utilization and implementation of passive heating and other improved facility-management approaches.

Cari and Jeremy just bought a bed and breakfast inn at a very attractive price. The business had been doing poorly. Before they reopened the inn for business, they attended a seminar on operating a high-quality business. Now that they are ready to open the inn, they need some advice on quality costs and the management and control of quality.

Required:

1. Identify and define each of the four categories in a typical Cost-of-Quality (COQ) reporting system.

2. For the identified business (bed and breakfast) provide three examples of costs within each of the four COQ categories.

1. Prevention costs are incurred to keep quality defects from occurring; Appraisal (detection) costs are costs devoted to the measurement and analysis of data to determine conformity of outputs to specification(s); Internal failure costs are all costs associated with defective processes or defective products detected before delivery to customers; External failure costs are all costs associated with defective/poor-quality outputs detected after being delivered to the customer.

2. Examples of each of the four COQ categories:

Prevention:

● Hiring employees with good references.

● Training of owners and employees.

● Good security.

● Good reservation system.

● Purchasing quality furniture.

Appraisal:

● Verifying accuracy of reservation and registration procedures.

● Inspecting rooms, facilities, building and grounds regularly.

● Observing activities of employees.

● Testing furniture and fixtures.

● Taste testing food.

Internal failure:

● Re-cleaning rooms and facilities.

● Restocking rooms with linens, glasses, etc.

● Out of stock supplies.

● Re-inspection.

● Failure to bill on a timely basis.

External failure:

● Responding to complaints about rooms and food.

● Responding to complaints about reservations.

● Emergency cleaning of rooms when not ready on time.

● Customer refunds because of unsatisfactory conditions.

● Opportunity cost of lost revenue resulting from unhappy customers.

Verizon Manufacturing Company spent $400,000 in 2019 to inspect incoming components. Of the $400,000, $240,000 is fixed appraisal costs. The variable inspection cost is $0.20 per component. It takes two components for each finished product. Internal failure costs average $80 per failed unit of finished goods. In 2019, five percent of all completed items had to be reworked. External failure costs average $200 per failed unit. The company's average external failures are one percent of units sold. The company manufactures all units as ordered and carries no materials inventories. Seeking to decrease its total cost of quality (COQ), Verizon contracted Quality-is-Free Consultants, Inc. (QIFC) to study ways to improve product quality and to reduce costs. Upon completion of the study, QIFC recommended automatic inspection equipment that requires a $60,000 annual cost for training related to the inspection/appraisal process and $150,000 for inspection equipment rental and maintenance. The new equipment will eliminate $40,000 of the fixed appraisal costs, reduce the amount of unacceptable product units in the manufacturing process by 10 percent, and cut product failures by half. The company paid the consulting firm $100,000 in early January 2020 for the project. Verizon expects no changes in its operating level in the foreseeable future.

What effect does the new equipment have on total appraisal costs?

C

As noted in the text, a comprehensive framework for managing and controlling quality contains both financial and non-financial performance indicators (metrics). Provide four (4) examples of internal quality metrics, and four (4) examples of external (i.e., customer-based) non-financial quality metrics.

Which of the following is not a point of difference between lean manufacturing and traditional manufacturing processes?

Over the last few months, Ithaca Precision Instruments (IPI) obtained the following measurements on a key quality characteristic of its product: Observed Quality Characteristic Probability 0.46 0.05 0.47 0.10 0.48 0.12 0.49 0.15 0.50 0.30 0.51 0.12 0.52 0.10 0.53 0.05 0.54 0.01 The company's experience has been that a customer will reject a product that deviates from the target quality characteristic of 0.50 by more than 0.004. Each rejection costs the firm an estimated $5.00. Determine the expected total quality loss of the observed quality characteristic for IPI. Round final steps of calculation to 4 decimal places (e.g., $18.89568 becomes $18.8957).

Pandra Manufacturing obtained the following measurements on the quality characteristic of the product from its operations in the last few months:

Observed Quality Characteristic, x Probability 0.46 0.05 0.47 0.10 0.48 0.12 0.49 0.15 0.50 0.30 0.51 0.12 0.52 0.10 0.53 0.05 0.54 0.01 The company has determined that no customer will accept any unit that deviates more than 0.04 from the target quality characteristic, T, of 0.5. The company estimates that each rejection would cost the company $500.

Required:

1. Calculate (to the nearest dollar) the cost coefficient, k, for the Taguchi Quality Loss Function (QLF) based on the above information.

2. Determine (to two decimal places) the estimated quality loss, L(x), for each of the observed values of the quality characteristic, x, presented in the above table.

3. Based on the data you generate in response to Requirement 2 above, determine the expected loss, EL(x), given the probabilities presented in the above table. Round final answer to three decimal places.

4. Use the formula EL(x) = k (σ2 + D2) to verify your answer in (3), where σ2=∑(x-x̄)f(x) ,and D = the deviation of the mean value of the quality characteristic from the target value =(x̄-T). Round the calculation for D to four decimal places, and the calculation of EL(x) to three decimal places.

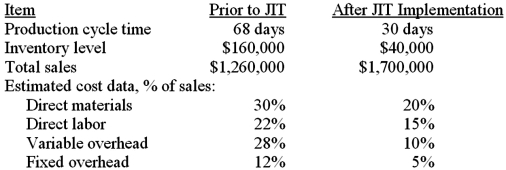

In an effort to improve its competitive position, J.J.Borden Company recently introduced Just-in-Time (JIT) production techniques.Its management accountant assembled the following data regarding the recent change:

Inventory carrying cost is estimated as 15.0% per year.

Required:

1. Estimate the net financial benefit (expressed in terms of the change in operating income) that the company realized from the switch to JIT manufacturing. Round your answer to nearest dollar.

2. List four (4) nonfinancial benefits the company might expect as a result to its move to JIT.

3. List two (2) expected costs of implementing a JIT system?

Inventory carrying cost is estimated as 15.0% per year.

Required:

1. Estimate the net financial benefit (expressed in terms of the change in operating income) that the company realized from the switch to JIT manufacturing. Round your answer to nearest dollar.

2. List four (4) nonfinancial benefits the company might expect as a result to its move to JIT.

3. List two (2) expected costs of implementing a JIT system?

In a Cost of Quality (COQ) report, sales returns and allowances due to quality deficiency would be classified as:

Ladder Manufacturing specifies the quality characteristic of one of its popular products to be 0.400" ± 0.010. An analysis of company records for the last two years suggests that the average cost for warranty repair or replacement is $100.00 per unit. The customer service manager believes that the product is likely to fail during the warranty period when the quality characteristic exceeds on either side of the target of 0.400, by the tolerance of 0.010.

What is the amount of the estimated loss, L(x), using a Taguchi Quality Loss Function (QLF), when the actual quality characteristic, x, is 0.405? (Round final answer to nearest dollar.)

Value stream costing attempts to do all of the following except:

Pandra Manufacturing specifies the quality characteristic of one of its popular products to be 0.500" ± 0.020. An analysis of company records for the last two years suggests that the average cost for warranty repair or replacement is $125.00 per unit. The customer service manager believes that the product is likely to fail during the warranty period when the quality characteristic exceeds on either side of the target of 0.500 the tolerance of 0.020.

What is the amount of the estimated loss (to three decimal places) using a Taguchi quality loss function (QLF) if the actual quality characteristic, x, is 0.510?

Six Sigma, absolute versus goalpost, and Taguchi Quality Loss Functions (QLF) all represent ways to:

A graphical representation of the variation in a given set of data is a(n):

Within a Cost-of-Quality (COQ) system, product liability resulting from a legal action is classified as a(n):

Which of the following is not a likely consequence of investments made to improve quality?

Which of the following is not one of the five principles of lean manufacturing?

In a Cost of Quality (COQ) reporting framework, scrap costs because of a quality failure would be classified as:

An example of an internal failure cost in a Cost-of-Quality (COQ) reporting system is:

An electronic component has an output voltage specification of 138.0 ± 5.0 millivolts. The loss to the firm for a component that is outside of the specifications is estimated as $220. The output voltage for a sample unit, x, is 134.0 millivolts.

Required:

1. Calculate (to two decimal places) the value of k, the cost coefficient in the Taguchi Quality Loss Function (QLF) for the above situation.

2. Calculate (to two decimal places) the amount of the estimated loss, L(x), for x = 134 millivolts.

3. Calculate (to two decimal places) the amount of the estimated loss, L(x), for x = 136 millivolts.

4. Calculate (to two decimal places) the amount of the estimated loss, L(x), for x = 138 millivolts.

5. What is the primary insight revealed by the Taguchi Quality Loss Function (QLF)?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)