Exam 9: Accounting for Special-Purpose Entities, Including Public Colleges and Universities

Exam 1: Introduction to Accounting and Financial Reporting for Governmental and Not-For-Profit Organizations134 Questions

Exam 2: Overview of Financial Reporting for State and Local Governments135 Questions

Exam 3: Modified Accrual Accounting: Including the Role of Fund Balances and Budgetary Authority143 Questions

Exam 4: Accounting for the General and Special Revenue Funds125 Questions

Exam 5: Accounting for Other Governmental Fund Types: Capital Projects, Debt Service, and Permanent152 Questions

Exam 6: Proprietary Funds130 Questions

Exam 7: Fiduciary Trustfunds154 Questions

Exam 8: Government-Wide Statements, Capital Assets, Long-Term Debt143 Questions

Exam 9: Accounting for Special-Purpose Entities, Including Public Colleges and Universities105 Questions

Exam 10: Accounting for Private Not-For-Profit Organizations151 Questions

Exam 11: College and University Accounting Private Institutions125 Questions

Exam 12: Accounting for Hospitals and Other Health Care Providers100 Questions

Exam 13: Auditing, Tax-Exempt Organizations, and Evaluating Performance151 Questions

Exam 14: Financial Reporting by the Federal Government66 Questions

Select questions type

Financial reporting for a special-purpose local government depends on whether that government is engaged in governmental-type,business-type or fiduciary-type activities.

(True/False)

4.9/5  (31)

(31)

Which of the following is true regarding the Statement of Cash Flows for a public college?

(Multiple Choice)

4.9/5 (36)

With respect to public colleges engaged in business-type activities,which of the following is not correct?

(Multiple Choice)

4.8/5 (34)

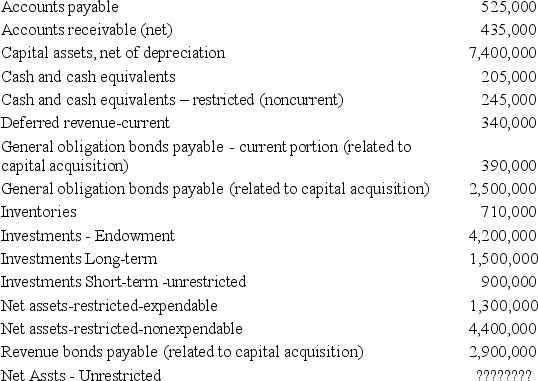

Northwest State University had the following account balances as of June 30,2014.Debits are not distinguished from credits,so assume all accounts have a "normal" balance (i.e.cash is a debit and accounts payable a credit)

Required:

Prepare,in good form,a Statement of Net Assets for Northwest State University as of June 30,2014.

Required:

Prepare,in good form,a Statement of Net Assets for Northwest State University as of June 30,2014.

(Essay)

4.9/5 (33)

City and county governments are typically classified as special purpose governments.

(True/False)

4.8/5 (42)

For financial reporting purposes,governmental health care entities,public school systems,other not-for-profit entities and public colleges and universities may be considered to be special-purpose entities.

(True/False)

4.7/5 (33)

GASB standards permit exercise of judgment when determining whether a government is general-purpose or special-purpose.

(True/False)

4.8/5 (42)

The following information applies to the next three questions:

Tuition and fees for the Northern University was assessed at $21,000,000. Scholarship allowances, for which no services are required, were $1,700,000 and graduate assistantships, for which services are required, were $900,000.

-What is the journal entry to record the scholarship allowances?

(Multiple Choice)

4.8/5 (40)

Public higher education institutions that report as special-purpose entities engaged in business-type activities only are still required to prepare a Management's Discussion and Analysis.

(True/False)

4.9/5 (32)

A special-purpose government engaged in business-type activities financed in whole or part by fees charged to external parties are usually reported in fiduciary funds.

(True/False)

4.7/5 (36)

Which of the following groups would not be considered a component unit of a special-purpose government,for the purposes of applying GASB Statement 39: Determining Whether Certain Organizations Are Component Units?

(Multiple Choice)

4.7/5 (35)

List three examples (types)of general-purpose state or local governments and three special-purpose local governments.

(Essay)

4.8/5 (30)

The following information applies to the next three questions:

Tuition and fees for the Northern University was assessed at $21,000,000. Scholarship allowances, for which no services are required, were $1,700,000 and graduate assistantships, for which services are required, were $900,000.

-What is the journal entry to record tuition revenue?

(Multiple Choice)

4.9/5 (26)

Assume a government is a special-purpose government engaged in only one governmental activity.Which financial statements would be required?

(Multiple Choice)

4.9/5 (38)

Sometimes,but not always public colleges are included as component units in the state CAFR

(True/False)

4.7/5 (32)

Assume a government is determined to be a special-purpose government engaged in business-type activities only.Which of the following financial statements would be required?

(Multiple Choice)

4.9/5 (32)

Public colleges typically report as special-purpose entities engaged only in business-type activities.

(True/False)

4.8/5 (33)

Tuition waived for academic and athletic scholarships is deducted from student fee revenue when preparing a Statement of Revenues,Expenses,and Changes in Net Assets.

(True/False)

4.9/5 (38)

Special-purpose governmental entities that are engaged in a single governmental-type activity only are required to prepare only the statements required for governmental fund basis financial statements.

(True/False)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)