Exam 10: Credit Risk I: Individual Loan Risk

By selecting and combining different economic and financial borrower characteristics, an FI manager may be able to improve the pricing of default risk.

True

Explain the major concept of Altman's linear discriminant model. What would you consider to be the major disadvantages of this model?

Discriminant models divide borrowers into high or low default risk classes contingent on their observed characteristics (Xj). Similar to linear probability models, linear discriminant models use past data as inputs into a model to explain repayment experience on old loans. The relative importance of the factors used in explaining past repayment performance then forecasts whether the loan falls into the high or low default class.

In Altman's linear discriminant model, the indicator variable Z is the overall measure of the default risk classification of a borrower.This in turn depends on the values of various financial ratios of the borrower (Xj) and the weighted importance of these ratios based on the past observed experience of defaulting versus non-defaulting borrowers derived from a discriminant analysis model. According to Altman's credit scoring model, a score of less than 1.81 would place the potential borrower into a high default risk category. Any score above 2.99 is regarded as a low default risk, while a score between 1.81 and 2.99 is in the 'zone of ignorance', where a borrower may or may not default.

Several criticisms have been levied against linear discriminant models. First, the models identify only two extreme categories of risk: default or no default. The real world considers several categories of default severity. Second, the relative weights of the variables may change over time. Further, the actual variables to be included in the model may change over time. Third, these models ignore important, hard-to-quantify factors that may play a crucial role in the default or no default decision. For example, the reputation of the borrower and the nature of long-term borrower-lender relationships could be important borrower-specific characteristics, as could macroeconomic factors, such as the phase of the business cycle. Fourth, no centralised database on defaulted business loans for proprietary and other reasons exists. This constrains the ability of many FIs to use traditional credit scoring models (and quantitative models in general) for larger business loans.

The term disintermediation refers to the process in which firms access:

C

Term structure of credit risk approach models are also known as:

Assume the interest rate in the market for one-year zero-coupon government bonds is i = 8 per cent and the rate for one-year zero-coupon grade BBB bonds is k = 10.2 per cent. What is the implied probability of repayment on the corporate bond (round to two decimals)?

Assume that i1 = 11 per cent and i2 = 12 per cent, and that k1 = 14.50 per cent and k2 = 16.50 per cent. What is the expected probability of repayment on the one-year corporate bonds in one year's time (round to two decimals)?

A loan provided by a group of FIs as opposed to a single lender is called:

A borrower's leverage refers to the payment capacity, that is, the 'leverage' the borrower has to service its loans.

Consider the following formula for calculating the contractually promised gross return on a loan k, per dollar lent: (1 + k) = 1 + [f + (BR + m)]/ {1 - [b(1 - R)]}. Which of the following statements is true?

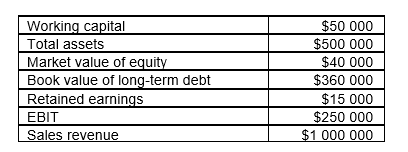

Consider the following data of a prospective borrower.  What is this company's Z score (round to two decimals)?

What is this company's Z score (round to two decimals)?

Moody's KMV Credit Monitor Model compares loans with option payoffs.

Banks have been partially responsible for big corporate collapses such as Enron.

In the context of the KMV Credit Monitor Model, the market value of a risky loan made by a lender to a borrower can be expressed as:

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)