Exam 5: Interest Rate Risk Measurement: The Repricing Model

Exam 1: Why Are Financial Institutions Special67 Questions

Exam 2: The Financial Services Industry: Depository Institutions66 Questions

Exam 3: The Financial Services Industry: Other Financial Institutions56 Questions

Exam 4: Risk of Financial Institutions67 Questions

Exam 5: Interest Rate Risk Measurement: The Repricing Model69 Questions

Exam 6: Interest Rate Risk Measurement: the Duration Model65 Questions

Exam 7: Managing Interest Rate Risk Using Off Balance Sheet Instruments62 Questions

Exam 8: Credit Risk I: Individual Loan Risk65 Questions

Exam 9: Market Risk55 Questions

Exam 10: Credit Risk I: Individual Loan Risk65 Questions

Exam 11: Credit Risk II: Loan Portfolio and Concentration Risk50 Questions

Exam 12: Sovereign Risk65 Questions

Exam 13: Foreign Exchange Risk64 Questions

Exam 14: Liquidity Risk64 Questions

Exam 15: Liability and Liquidity Management65 Questions

Exam 16: Off-Balance-Sheet Activities65 Questions

Exam 17: Technology and Other Operational Risk67 Questions

Exam 18: Capital Management and Adequacy66 Questions

Select questions type

Which of the following is a weakness of the repricing model to measure interest rate risk?

Free

(Multiple Choice)

4.8/5  (33)

(33)

Correct Answer: Verified

Verified

D

The repricing gap considers the timing and size of cash flows.

Free

(True/False)

4.8/5 (26)

Correct Answer:Verified

False

Outline what is meant by the CGAP effect and explain the relationship between interest rate changes and changes in net interest income. Specifically indicate whether a FI would wish to hold a negative or positive CGAP and under which interest rate conditions.

(Essay)

4.8/5 (37)

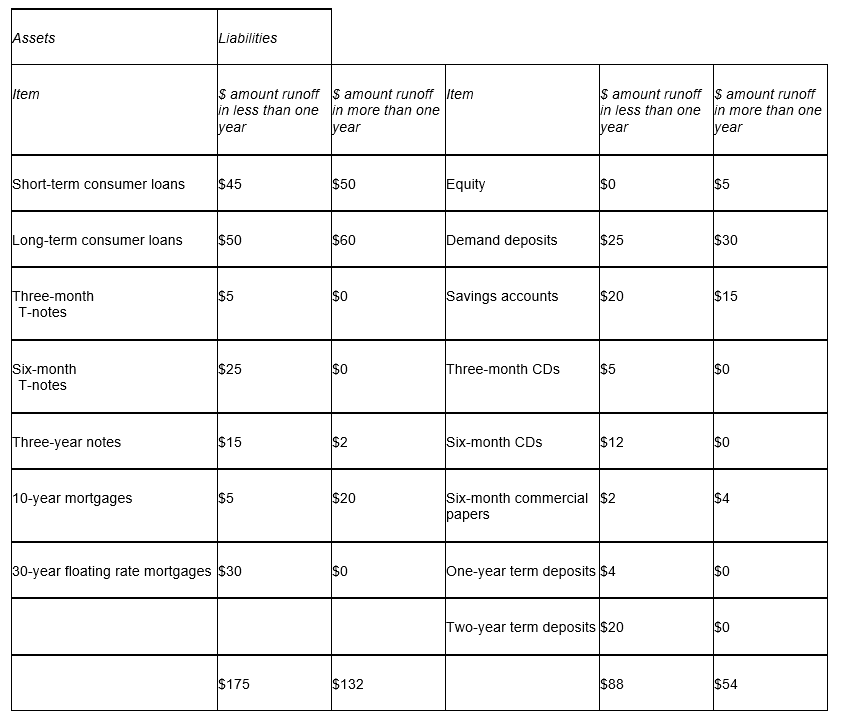

Consider the following table:  How does a decrease in the average one-year interest rate of 50 basis points affect the FI's future net interest income?

How does a decrease in the average one-year interest rate of 50 basis points affect the FI's future net interest income?

(Multiple Choice)

4.8/5 (34)

The liquidity premium theory of the term structure of interest rates:

(Multiple Choice)

4.9/5 (27)

The market segmentation theory of the term structure of interest rates:

(Multiple Choice)

4.8/5 (35)

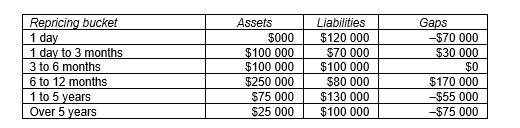

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the overnight interest rate decreased by 100 basis points?

What is the annualised change in the bank's future net interest income if the overnight interest rate decreased by 100 basis points?

(Multiple Choice)

4.8/5 (40)

The cumulative gap over the whole balance sheet by definition:

(Multiple Choice)

4.8/5 (38)

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced over five years is an increase of 50 basis points?

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced over five years is an increase of 50 basis points?

(Multiple Choice)

4.9/5 (40)

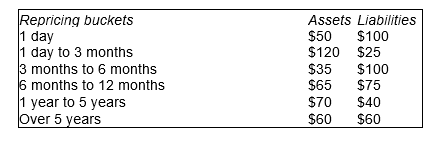

In the last quarter ABC Bank reported the following repricing buckets:

Calculate the repricing gaps for each maturity bucket and the cumulative gaps.

Calculate the repricing gaps for each maturity bucket and the cumulative gaps.

(Essay)

4.8/5 (29)

An FI with a positive repricing gap expects interest rates to decrease.

(True/False)

5.0/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)