Exam 11: Diversification and Risky Asset Allocation

Stock X has a standard deviation of 21 percent per year and stock Y has a standard deviation of 6 percent per year.The correlation between stock A and stock B is .38.You have a portfolio of these two stocks wherein stock X has a portfolio weight of 42 percent.What is your portfolio standard deviation?

C

You are advising several individual investors who are interested in investing in portfolios comprised of both stocks and bonds.In preparation for meeting with these various investors,you plot the investment opportunity set for stocks and bonds.Given this information,why might you advise some of the investors to invest in a portfolio other than the minimum variance portfolio?

There are several reasons why I might advise some investors to consider investing in a portfolio other than the minimum variance portfolio.

Firstly, the minimum variance portfolio is designed to minimize risk, but it may not necessarily maximize returns. Some investors may have a higher risk tolerance and are willing to take on more risk in exchange for potentially higher returns. In this case, I would advise them to consider a portfolio that offers a higher expected return, even if it comes with slightly higher risk.

Additionally, the minimum variance portfolio may not align with the specific investment goals and preferences of each individual investor. Some investors may have specific sector preferences or ethical considerations that they want to incorporate into their portfolio. In these cases, I would advise them to consider a portfolio that aligns with their specific investment criteria, even if it deviates from the minimum variance portfolio.

Furthermore, the minimum variance portfolio is based on historical data and assumptions about risk and return. However, these assumptions may not hold true in the future, especially in rapidly changing market conditions. Therefore, I would advise some investors to consider a portfolio that takes into account current market conditions and potential future trends, even if it means deviating from the minimum variance portfolio.

Overall, while the minimum variance portfolio is a valuable tool for managing risk, it may not be the best fit for every investor. By considering individual risk tolerance, investment goals, and market conditions, I would advise some investors to explore portfolios that offer different risk-return trade-offs than the minimum variance portfolio.

An efficient portfolio is a portfolio that does which one of the following?

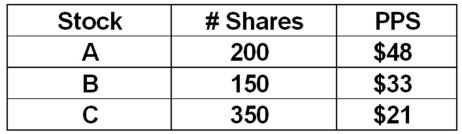

A portfolio consists of the following securities.What is the portfolio weight of stock B?

Which of the following affect the expected rate of return for a portfolio?

I.weight of each security held in the portfolio

II.the probability of various economic states occurring

III.the variance of each individual security

IV.the expected rate of return of each security given each economic state

What is the correlation coefficient of two assets that are uncorrelated?

You have a portfolio which is comprised of 48 percent of stock A and 52 percent of stock B.What is the standard deviation of this portfolio?

The value of an individual security divided by the portfolio value is referred to as the portfolio:

A stock fund has a standard deviation of 16 percent and a bond fund has a standard deviation of 4 percent.The correlation of the two funds is .11.What is the weight of the stock fund in the minimum variance portfolio?

Roger has a portfolio comprised of $8,000 of stock A and $12,000 of stock B.What is the standard deviation of this portfolio?

You have a portfolio which is comprised of 75 percent of stock A and 25 percent of stock B.What is the expected rate of return on this portfolio?

Which one of the following correlation relationships has the potential to completely eliminate risk?

Which one of the following statements is correct concerning asset allocation?

A stock fund has a standard deviation of 17 percent and a bond fund has a standard deviation of 8 percent.The correlation of the two funds is .24.What is the approximate weight of the stock fund in the minimum variance portfolio?

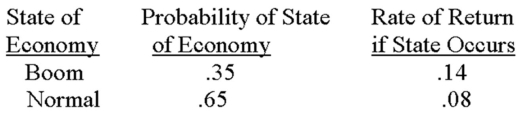

The risk-free rate is 4.15 percent.What is the expected risk premium on this stock given the following information?

Foreign securities are generally considered to be more risky than domestic securities.Given this assumption,explain how adding foreign securities into a domestic portfolio can affect the Markowitz efficient portfolios.

You are graphing the investment opportunity set for a portfolio of two securities with the expected return on the vertical axis and the standard deviation on the horizontal axis.If the correlation coefficient of the two securities is +1,the opportunity set will appear as which one of the following shapes?

To reduce risk as much as possible,you should combine assets which have one of the following correlation relationships?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)