Exam 12: Relevant Costs for Decision Making

Exam 1: Managerial Accounting and the Business Environment48 Questions

Exam 2: Cost Terms, Concepts, and Classifications93 Questions

Exam 3: Systems Design: Job-Order Costing108 Questions

Exam 4: Systems Design: Process Costing162 Questions

Exam 5: Activity-Based Costing: A Tool to Aid Decision Making124 Questions

Exam 6: Cost Behaviour: Analysis and Use107 Questions

Exam 7: Cost-Volume-Profit Relationships141 Questions

Exam 8: Variable Costing: A Tool for Management135 Questions

Exam 9: Budgeting134 Questions

Exam 10: Standard Costs and Overhead Analysis211 Questions

Exam 11: Reporting for Control200 Questions

Exam 12: Relevant Costs for Decision Making139 Questions

Exam 13: Capital Budgeting Decisions180 Questions

Exam 14: Financial Statement Analysis200 Questions

Select questions type

The Hyatt Company is trying to decide whether it should purchase new equipment and continue to make its subassemblies internally or if production should be discontinued and the subassembly purchased from an outside supplier.

New equipment for producing the subassemblies can be purchased at a cost of $400,000.The equipment would have a five-year useful life (the company uses straight-line depreciation)and a $50,000 salvage value.

Alternatively,the subassemblies could be purchased from an outside supplier.The supplier has offered to provide the subassemblies for $9 each under a five-year contract.

Hyatt Company's present costs per unit of producing the subassemblies internally (with the old equipment)are given below.The costs are based on a current activity level of 40,000 subassemblies per year:

Direct Materials Direct Labour Variable Overhead Fixed Overhead ( \ 0.80 supervision, \ 0.90 depreciation, and \ 2 general company overhead) Total Cost per Unit \ 3.00 \ 4.20 \ 0.60 \ 3.70 \ 11.50

The new equipment would be more efficient and would reduce direct labour costs and variable overhead costs by 25%. Supervision cost ($30,000 per year) and direct materials cost per unit would not be affected by the new equipment. The company has no other use for the space now being used to produce the subassemblies. The company's total general company overhead would not be affected by this decision. Assume direct labour is a variable cost.

Required:

Assume that 40,000 subassemblies are needed each year. Prepare an analysis of the two alternatives and make a recommendation to the management of the company of the appropriate course of action.

(Essay)

4.7/5  (41)

(41)

Northern Stores is a retailer in British Columbia.The most recent monthly income statement for Northern Stores is given below:

Total Store 1 Store II Sales \ 2,100,000 \ 1,300,000 \ 800,000 Less variable expense Contribution margin \ 840,000 \ 418,000 \ 422,000 Less traceable fixed expense Segment margin \ 420,000 \ 187,000 \ 233,000 Less common fixed expenses Operating Income \ (23,000) \ 93,000

Northern is considering closing Store I. If Store I is closed, one-fourth of its traceable fixed expenses would continue to be incurred. Also, the closing of Store I would result in a 20% decrease in sales in Store II. Northern allocates common fixed expenses on the basis of sales dollars and none of these costs would be saved if a store were shut down.

Required:

Compute the overall increase or decrease in the operating income of Northern Stores if Store I is closed.

(Essay)

4.8/5 (37)

(Appendix 12A)The markup over cost under the absorption costing approach would increase if the unit product cost increases,holding everything else constant.

(True/False)

5.0/5 (40)

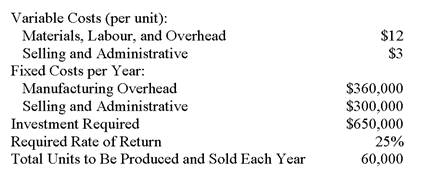

(Appendix 12A) Turnhilm, Inc. is considering adding a small electric mower to its product line. Management believes that in order to be competitive, the mower cannot be priced above $139. The company requires a minimum return of 25% on its investments. Launching the new product would require an investment of $8,000,000. Sales are expected to be 40,000 units of the mower per year.

Required:

a) Compute the target cost of a mower.

b) Suppose the target cost calculated in part (b) above is not attainable using the company's current manufacturing facilities. Specifically, the average cost of producing the 40,000 units is $100 per unit. Besides abandoning the idea, what specific options are available to Turnhilm?

c) Suppose, using the company's current manufacturing facilities the average cost of producing the 40,000 units is only $80. What other specific options are available to Turnhilm?

(Essay)

4.8/5 (39)

Hadley, Inc. makes a line of bathroom accessories. Because of a decline in sales, the company has 10,000 machine hours of idle capacity available each year. This idle capacity could be used by the company to make, rather than buy, one of the components used in its production process. Hadley needs 5,000 units of this component each year. At present, the component is being purchased from an outside supplier at $7.50 per unit. Variable production cost for the component would be $4.10 per unit, and additional supervisory costs would be $18,000 per year. Already existing fixed costs, which would be allocated to this part, amount to $300,000 per year.

-What would be the change in the company's overall annual operating income that would result from making the component,rather than buying it?

(Multiple Choice)

4.9/5 (40)

Using the profitability index,it is easy to decide which product is less profitable and should be de-emphasized.

(True/False)

4.8/5 (48)

The following are the Wyeth Company's unit costs of making and selling an item at a volume of 10,000 units per month, which represents the company's capacity:

Present sales amount to 9,000 units per month. An order has been received from a customer in a foreign market for 1,000 units. The order would not affect current sales. Fixed costs, both manufacturing and selling and administrative, are constant within the relevant range between 8,000 and 10,000 units per month. The variable selling and administrative costs would have to be incurred for this special order as well as all other sales. Assume direct labour is a variable cost.

-Assume the company has 50 units left over from last year that have small defects and which will have to be sold at a reduced price as scrap.This would have no effect on the company's other sales.What cost is relevant as a guide for setting a minimum price on these defective units?

Present sales amount to 9,000 units per month. An order has been received from a customer in a foreign market for 1,000 units. The order would not affect current sales. Fixed costs, both manufacturing and selling and administrative, are constant within the relevant range between 8,000 and 10,000 units per month. The variable selling and administrative costs would have to be incurred for this special order as well as all other sales. Assume direct labour is a variable cost.

-Assume the company has 50 units left over from last year that have small defects and which will have to be sold at a reduced price as scrap.This would have no effect on the company's other sales.What cost is relevant as a guide for setting a minimum price on these defective units?

(Multiple Choice)

4.9/5 (33)

Future costs that do NOT differ among the alternatives are NOT relevant in a decision.

(True/False)

4.7/5 (41)

Gildersleeve Corporation manufactures a product that has the following costs:

Per unit Per year Direct materials \6 .00 Direct labour 5.00 Variable manufacturing overhead 4.00 Fixed manufacturing overhead \ 360,000 Variable SG\&A expenses 5.00 Fixed SG\&A expenses 120,000

The company uses the absorption costing approach to cost-plus pricing. The pricing calculations are based on budgeted production and sales of 30,000 units per year.

The company has invested $600,000 in this product and expects a return on investment of 15%.

Required:

a) Compute the markup on absorption cost.

b) Compute the target selling price of the product using the absorption costing approach.

(Essay)

4.8/5 (38)

Redner,Inc.produces three products.Data concerning the selling prices and unit costs of the three products appear below:

Product Selling price \ 80 \ 60 \ 90 Variable costs 50 40 55 Fixed costs 25 8 22 Grinding machine time 10. 5 7.

Fixed costs are applied to the products on the basis of direct labour hours.

Demand for the three products exceeds the company's productive capacity. The grinding machine is the constraint, with only 2,400 minutes of grinding machine time available this week.

Required:

a) Given the grinding machine constraint, which product should be emphasized? Support your answer with appropriate calculations.

b) If there is still unfilled demand for the product that the company should emphasize in part a) above, up to how much should the company be willing to pay for an additional hour of grinding machine time?

(Essay)

4.8/5 (34)

What should a firm faced with a production constraint do to maximize total contribution margin?

(Multiple Choice)

4.8/5 (35)

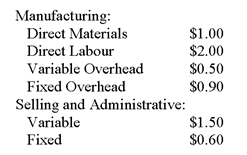

Mercer Company is planning the introduction of a new product. The following information relating to the product has been assembled:

The company uses the absorption costing approach to pricing.

-(Appendix 12A)The target selling price for one unit of the new product is closest to which of the following?

The company uses the absorption costing approach to pricing.

-(Appendix 12A)The target selling price for one unit of the new product is closest to which of the following?

(Multiple Choice)

4.8/5 (35)

(Appendix 12A)Kircher,Inc.manufactures a product with the following costs:

Per unit Per year Direct materials \ 24.90 Direct labour 13.90 Variable manufacturing overhead 2.10 Fixed manufacturing overhead \ 1,182,600 Variable SG\&A expenses 2.00 Fixed SG\&A expenses 1,166,400

The company uses the absorption costing approach to cost-plus pricing.The pricing calculations are based on budgeted production and sales of 81,000 units per year.The company has invested $220,000 in this product and expects a return on investment of 15%.The target selling price based on the absorption costing approach would be closest to which of the following?

(Multiple Choice)

4.9/5 (38)

(Appendix 12A)Under time and material pricing,the material loading charge includes which of the following items? Cost of Ordering. Invoice Cost Handling, and Desired Profit of Materials Storing Materials on Materials A) Yes Yes Yes B) No Yes Yes C) No No Yes D) Yes Yes No

(Multiple Choice)

4.9/5 (27)

The following standard costs pertain to a component part manufactured by Ashby Company:

Direct Materials Direct Labour Manufacturing Overhead Standard Cost per Unit \ 2 \ 5 \ 20 \ 27

The company can purchase the part from an outside supplier for $25 per unit.The manufacturing overhead is 60% fixed,and this fixed portion would not be affected by this decision.Assume that direct labour is an avoidable cost in this decision.What would be the relevant amount of the standard cost per unit in a decision of whether to make the part internally or buy it from the external supplier?

(Multiple Choice)

4.8/5 (43)

The Lantern Corporation has 1,000 obsolete lanterns that are carried in inventory at a manufacturing cost of $20,000.If the lanterns are re-machined for $5,000,they could be sold for $9,000.Alternatively,the lanterns could be sold for scrap for $1,000.Which alternative is more desirable,and what are the total relevant costs for that alternative?

(Multiple Choice)

4.8/5 (38)

Dowchow Company makes two products from a common input. Joint processing costs up to the split-off point total $38,400 a year. The company allocates these costs to the joint products on the basis of their total sales values at the split-off point. Each product may be sold at the split-off point or processed further. Data concerning these products appear below:

-What is the minimum amount the company should accept for Product X if it is to be sold at the split-off point?

-What is the minimum amount the company should accept for Product X if it is to be sold at the split-off point?

(Multiple Choice)

4.8/5 (34)

Kramer Company makes 4,000 units per year of a part called an axial tap for use in one of its products.Data concerning the unit production costs of the axial tap follow:

Direct Materials Direct Labour Variable Manufacturing Overhead Fixed Manufacturing Overhead Total Manufacturing Cost per Unit \ 35 \ 10 \ 8 \ 20 \ \ 73

An outside supplier has offered to sell Kramer Company all of the axial taps it requires. If Kramer Company decided to discontinue making the axial taps, 40% of the above fixed manufacturing overhead costs could be avoided. Assume that direct labour is a variable cost.

Required:

a) Assume Kramer Company has no alternative use for the facilities presently devoted to production of the axial taps. If the outside supplier offers to sell the axial taps for $65 each, should Kramer Company accept the offer? Fully support your answer with appropriate calculations.

b) Assume that Kramer Company could use the facilities presently devoted to production of the axial taps to expand production of another product that would yield an additional contribution margin of $80,000 annually. What is the maximum price Kramer Company should be willing to pay the outside supplier for axial taps?

(Essay)

4.8/5 (37)

The Tolar Company has 400 obsolete desk calculators that are carried in inventory at a total cost of $26,800. If these calculators are upgraded at a total cost of $10,000, they can be sold for a total of $30,000. As an alternative, the calculators can be sold in their present condition for $11,200.

-What is the sunk cost in this situation?

(Multiple Choice)

4.9/5 (35)

(Appendix 12A)Lacy Corporation uses the absorption costing approach to cost-plus pricing to set prices for its products.Based on budgeted sales of 86,000 units next year,the unit product cost of a particular product is $81.60.The company's selling,general,and administrative expenses for this product are budgeted to be $1,247,000 in total for the year.The company has invested $360,000 in this product and expects a return on investment of 12%.The markup on absorption cost for this product would be closest to which of the following?

(Multiple Choice)

4.7/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)