Exam 12: Relevant Costs for Decision Making

Exam 1: Managerial Accounting and the Business Environment48 Questions

Exam 2: Cost Terms, Concepts, and Classifications93 Questions

Exam 3: Systems Design: Job-Order Costing108 Questions

Exam 4: Systems Design: Process Costing162 Questions

Exam 5: Activity-Based Costing: A Tool to Aid Decision Making124 Questions

Exam 6: Cost Behaviour: Analysis and Use107 Questions

Exam 7: Cost-Volume-Profit Relationships141 Questions

Exam 8: Variable Costing: A Tool for Management135 Questions

Exam 9: Budgeting134 Questions

Exam 10: Standard Costs and Overhead Analysis211 Questions

Exam 11: Reporting for Control200 Questions

Exam 12: Relevant Costs for Decision Making139 Questions

Exam 13: Capital Budgeting Decisions180 Questions

Exam 14: Financial Statement Analysis200 Questions

Select questions type

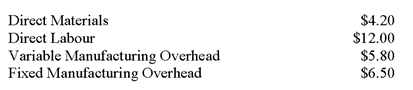

The SP Company makes 40,000 motors to be used in the production of its sewing machines.The average cost per motor at this level of activity consists of:

Direct Materials Direct Labour Variable Manufacturing Overhead Fixed Manufacturing Overhead \ 5.50 \ 5.60 \ 4.75 \ 4.45

An outside supplier recently began producing a comparable motor that could be used in the sewing machine.The price offered to SP Company for this motor is $18.If SP Company decides not to make the motors,there would be no other use for the production facilities,and total fixed factory overhead costs would not change.If SP Company decides to continue making the motor,how much higher or lower would net income be than if the motors are purchased from the outside suppler? Assume that direct labour is a variable cost in this company.

(Multiple Choice)

4.7/5  (35)

(35)

The Rodgers Company makes 27,000 units of a certain component each year for use in one of its products. The cost per unit for the component at this level of activity is as follows:

Rodgers has received an offer from an outside supplier that is willing to provide 27,000 units of this component each year at a price of $25 per component. Assume that direct labour is a variable cost.

-Assume that there is no other use for the capacity now being used to produce the component,and the total fixed manufacturing overhead of the company would not be affected by this decision.If Rodgers Company were to purchase the components rather than making them internally,what would be the impact on the company's annual operating income?

Rodgers has received an offer from an outside supplier that is willing to provide 27,000 units of this component each year at a price of $25 per component. Assume that direct labour is a variable cost.

-Assume that there is no other use for the capacity now being used to produce the component,and the total fixed manufacturing overhead of the company would not be affected by this decision.If Rodgers Company were to purchase the components rather than making them internally,what would be the impact on the company's annual operating income?

(Multiple Choice)

4.8/5 (45)

(Appendix 12A)The time and material approach pricing will result in attaining the company's desired profit only if forecasted billable activity is realized,holding all other things constant.

(True/False)

4.7/5 (37)

Only the variable costs identified with a product are relevant in a decision concerning whether to eliminate the product or not.

(True/False)

4.7/5 (28)

Managers should pay little attention to bottleneck operations because they have limited capacity for producing output.

(True/False)

4.8/5 (35)

(Appendix 12A)The Sloan Company must invest $120,000 to produce and market 16,000 units of Product X each year.Other cost information regarding Product X is as follows: Direct materials \ 7 Direct labour 5 Variable manufacturing overhead 4 Fixed manufacturing overhead. - \ 80,000 Variable selling, general, and administrative expense 3 Fixed selling, general, and administrative expense - \ 72,000

If Sloan Company requires a 15% return on investment,what would be the markup percentage on absorption cost for Product X,rounded to the nearest percent?

(Multiple Choice)

4.8/5 (36)

The Immanuel Company has just obtained a request for a special order of 6,000 jigs to be shipped at the end of the month at a selling price of $7 each. The company has a production capacity of 90,000 jigs per month with total fixed production costs of $144,000. At present, the company is selling 80,000 jigs per month through regular channels at a selling price of $11 each. For these regular sales, the cost for one jig is:

If the special order is accepted, Immanuel will not incur any selling expense; however, it will incur shipping costs of $0.30 per unit.

-Suppose that total regular sales of jigs are 85,000 units per month,and all other conditions remain the same.If Immanuel accepts the special order,what will be the change in monthly operating income?

If the special order is accepted, Immanuel will not incur any selling expense; however, it will incur shipping costs of $0.30 per unit.

-Suppose that total regular sales of jigs are 85,000 units per month,and all other conditions remain the same.If Immanuel accepts the special order,what will be the change in monthly operating income?

(Multiple Choice)

4.8/5 (42)

Bingham Company manufactures and sells Product J. Results for last year for the manufacture and sale of Product J are as follows:

Bingham Company anticipates no change in the operating result for Product J in the foreseeable future if the product is produced. Bingham is re-examining all of its products and is trying to decide whether or not to discontinue the manufacture and sale of Product J. The company's total fixed factory overhead cost would not be affected by this decision.

-Assume that discontinuing the manufacture and sale of Product J will not affect the sale of other products.If the company discontinues Product J,what will be the change in annual operating income due to this decision?

Bingham Company anticipates no change in the operating result for Product J in the foreseeable future if the product is produced. Bingham is re-examining all of its products and is trying to decide whether or not to discontinue the manufacture and sale of Product J. The company's total fixed factory overhead cost would not be affected by this decision.

-Assume that discontinuing the manufacture and sale of Product J will not affect the sale of other products.If the company discontinues Product J,what will be the change in annual operating income due to this decision?

(Multiple Choice)

4.9/5 (35)

Dowchow Company makes two products from a common input. Joint processing costs up to the split-off point total $38,400 a year. The company allocates these costs to the joint products on the basis of their total sales values at the split-off point. Each product may be sold at the split-off point or processed further. Data concerning these products appear below:

-What is the net monetary advantage of processing Product Y beyond the split-off point?

-What is the net monetary advantage of processing Product Y beyond the split-off point?

(Multiple Choice)

4.8/5 (41)

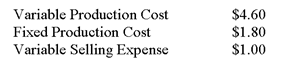

Dickson Company makes a product with the following costs:

The company uses the absorption costing approach to cost-plus pricing. The pricing calculations are based on budgeted production and sales of 60,000 units per year.

The company has invested $320,000 in this product and expects a return on investment of 15%.

Direct labour is a variable cost in this company.

-(Appendix 12A)The target selling price based on the absorption costing approach is closest to which of the following?

The company uses the absorption costing approach to cost-plus pricing. The pricing calculations are based on budgeted production and sales of 60,000 units per year.

The company has invested $320,000 in this product and expects a return on investment of 15%.

Direct labour is a variable cost in this company.

-(Appendix 12A)The target selling price based on the absorption costing approach is closest to which of the following?

(Multiple Choice)

4.8/5 (30)

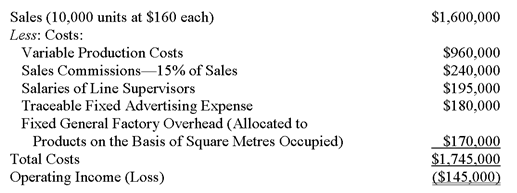

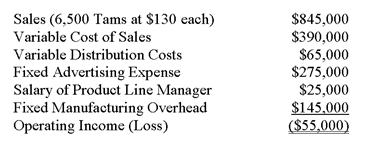

The Clemson Company reported the following results last year for the manufacture and sale of one of its products, known as a Tam:

Clemson Company is trying to determine whether to discontinue the manufacture and sale of Tams. The operating results reported above for last year are expected to continue in the foreseeable future if the product is not dropped. The fixed manufacturing overhead represents the costs of production facilities and equipment that the Tam product shares with other products produced by Clemson. If the Tam product were discontinued, there would be no change in the fixed manufacturing costs of the company.

-Assume that discontinuing the Tam product would result in a $120,000 increase in the contribution margin of other product lines.How many Tams would have to be sold next year for the company to be as well off as if it just dropped the line and enjoyed the increase in contribution margin from other products?

Clemson Company is trying to determine whether to discontinue the manufacture and sale of Tams. The operating results reported above for last year are expected to continue in the foreseeable future if the product is not dropped. The fixed manufacturing overhead represents the costs of production facilities and equipment that the Tam product shares with other products produced by Clemson. If the Tam product were discontinued, there would be no change in the fixed manufacturing costs of the company.

-Assume that discontinuing the Tam product would result in a $120,000 increase in the contribution margin of other product lines.How many Tams would have to be sold next year for the company to be as well off as if it just dropped the line and enjoyed the increase in contribution margin from other products?

(Multiple Choice)

4.9/5 (47)

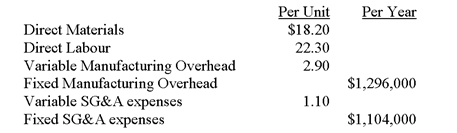

(Appendix 12A)Joeston Corporation makes a product with the following costs: Direct materials \ 14.70 Direct labour 14.10 Variable manufacturing overhead 3.70 Fixed manufacturing overhead. \ 305,200 Variable SG\&A expenses 3.00 Fixed SG\&A expenses 163,800

The company uses the absorption costing approach to cost-plus pricing.The pricing calculations are based on budgeted production and sales of 14,000 units per year.The company has invested $540,000 in this product and expects a return on investment of 10%.The markup on absorption cost would be closest to which of the following?

(Multiple Choice)

4.8/5 (26)

Eckert Company uses the absorption costing approach to cost-plus pricing to set prices for its products. Based on budgeted sales of 18,000 units next year, the unit product cost of a particular product is $60.40. The company's selling, general, and administrative expenses for this product are budgeted to be $370,800 in total for the year. The company has invested $260,000 in this product and expects a return on investment of 11%.

-(Appendix 12A)The markup on absorption cost for this product would be closest to which of the following?

(Multiple Choice)

4.9/5 (37)

Benjamin Signal Company produces products R,J,and C from a joint production process.Each product may be sold at the split-off point or be processed further.Joint production costs of $92,000 per year are allocated to the products based on the relative number of units produced.Data for Benjamin's operations for the current year are as follows:

Product Units Produced Allocated Joint Production Cost Sales Value at Split-off 8,000 \ 32,000 \ 76,000 10,000 40,000 71,000 5,000 20,000 48,000

Product R can be processed beyond the split-off point for an additional cost of $26,000 and can then be sold for $105,000. Product J can be processed beyond the split-off point for an additional cost of $38,000 and can then be sold for $117,000. Product C can be processed beyond the split-off point for an additional cost of $12,000 and can then be sold for $57,000.

Required:

Which products should be processed beyond the split-off point?

(Essay)

4.8/5 (39)

Dowchow Company makes two products from a common input. Joint processing costs up to the split-off point total $38,400 a year. The company allocates these costs to the joint products on the basis of their total sales values at the split-off point. Each product may be sold at the split-off point or processed further. Data concerning these products appear below:

-What is the net monetary advantage (disadvantage)of processing Product X beyond the split-off point?

(Multiple Choice)

4.9/5 (35)

The regular selling price for one Hom is $60. A special order has been received at Varone from the Fairview Company to purchase 8,000 Homs next year at 15% off the regular selling price. If this special order is accepted, the variable selling expense will be reduced by 25%. However, Varone would have to purchase a specialized machine to engrave the Fairview name on each Hom in the special order. This machine would cost $12,000, and Varone would have no use for it after the special order was filled. The total fixed costs, both manufacturing and selling, are constant within the relevant range of 30,000 to 40,000 Homs per year. Assume direct labour is a variable cost.

-If Varone has an opportunity to sell 37,960 Homs next year through regular channels and the special order is accepted for 15% off the regular selling price,what would be the effect on operating income next year due to accepting this order?

(Multiple Choice)

4.9/5 (36)

The Immanuel Company has just obtained a request for a special order of 6,000 jigs to be shipped at the end of the month at a selling price of $7 each. The company has a production capacity of 90,000 jigs per month with total fixed production costs of $144,000. At present, the company is selling 80,000 jigs per month through regular channels at a selling price of $11 each. For these regular sales, the cost for one jig is:

If the special order is accepted, Immanuel will not incur any selling expense; however, it will incur shipping costs of $0.30 per unit.

-If Immanuel accepts this special order,what will be the increase in the monthly operating income?

(Multiple Choice)

4.8/5 (29)

The manufacturing capacity of Jordan Company's facilities is 30,000 units a year.A summary of operating results for last year follows: Sales (18,000 units @ \ 100) \ 1,800,000 Variable Costs \ 990,000 Contribution Margin \ 810,000 Fixed Costs \ 495,000 Operating Income \ 315,000

A foreign distributor has offered to buy 15,000 units at $90 per unit next year.Jordan expects its regular sales next year to be 18,000 units.If Jordan accepts this offer and rejects some business from regular customers so as not to exceed capacity,what would be the total operating income next year? (Assume that the total fixed costs would be the same no matter how many units are produced and sold.)

(Multiple Choice)

4.9/5 (38)

Gata Co.plans to discontinue a department that has a $48,000 contribution margin and $96,000 of fixed costs.Of these fixed costs,$42,000 cannot be avoided.What would be the effect of discontinuing the department on Gata's overall operating income?

(Multiple Choice)

4.7/5 (39)

Hadley, Inc. makes a line of bathroom accessories. Because of a decline in sales, the company has 10,000 machine hours of idle capacity available each year. This idle capacity could be used by the company to make, rather than buy, one of the components used in its production process. Hadley needs 5,000 units of this component each year. At present, the component is being purchased from an outside supplier at $7.50 per unit. Variable production cost for the component would be $4.10 per unit, and additional supervisory costs would be $18,000 per year. Already existing fixed costs, which would be allocated to this part, amount to $300,000 per year.

-What would the annual cost of additional supervision have to be in order for Hadley to be economically indifferent to making or buying the component? (Assume all other conditions stay the same.)

(Multiple Choice)

4.9/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)