Exam 1: Limits, Alternatives, and Choices

Exam 1: Limits, Alternatives, and Choices398 Questions

Exam 2: The Market System and the Circular Flow252 Questions

Exam 3: Demand, Supply, and Market Equilibrium339 Questions

Exam 4: Market Failures: Public Goods and Externalities235 Questions

Exam 5: Governments Role and Government Failure275 Questions

Exam 6: Elasticity255 Questions

Exam 7: Utility Maximization256 Questions

Exam 8: Behavioral Economics274 Questions

Exam 9: Businesses and the Costs of Production307 Questions

Exam 10: Pure Competition in the Short Run167 Questions

Exam 11: Pure Competition in the Long Run182 Questions

Exam 12: Pure Monopoly224 Questions

Exam 13: Monopolistic Competition194 Questions

Exam 14: Oligopoly and Strategic Behavior265 Questions

Exam 15: Technology, Rd, and Efficiency231 Questions

Exam 16: The Demand for Resources244 Questions

Exam 17: Wage Determination308 Questions

Exam 18: Rent, Interest, and Profit210 Questions

Exam 19: Natural Resource and Energy Economics290 Questions

Exam 20: Public Finance: Expenditures and Taxes232 Questions

Exam 21: Antitrust Policy and Regulation237 Questions

Exam 22: Agriculture: Economics and Policy217 Questions

Exam 23: Income Inequality, Poverty, and Discrimination272 Questions

Exam 24: Health Care240 Questions

Exam 25: Immigration197 Questions

Exam 26: International Trade241 Questions

Exam 27: The Balance of Payments, Exchange Rates, and Trade Deficits252 Questions

Exam 28: The Economics of Developing Countries249 Questions

Select questions type

The production possibilities curve illustrates the basic principle that

(Multiple Choice)

4.9/5  (39)

(39)

Entrepreneurship refers to a new college graduate who is looking for a job with a large company.

(True/False)

4.8/5 (33)

A nation's production possibilities curve shows the maximum combinations of resources that a nation can use.

(True/False)

4.9/5 (34)

A movement from one point to another along the production possibilities curve would imply that

(Multiple Choice)

4.8/5 (32)

If the marginal benefits are greater than the marginal cost of an activity, then society should allocate fewer resources to this activity.

(True/False)

4.8/5 (30)

What is a major opportunity cost of going to college on a full-time basis?

(Multiple Choice)

4.9/5 (29)

Suppose that a consumer purchases just two goods, X and Y. The ratio of the price of good X to the price of good Y is the

(Multiple Choice)

4.9/5 (37)

A nation that devotes more of its resources to the production of capital goods rather than consumer goods is likely to

(Multiple Choice)

4.8/5 (43)

A nation's production possibilities curve might shift to the left (inward) as a result of

(Multiple Choice)

4.7/5 (34)

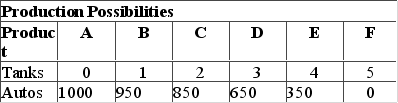

A nation can produce two products: tanks and autos. The table below is the nation's production possibilities schedule.  If the nation produces more and more tanks, the opportunity cost of each additional tank in terms of autos

If the nation produces more and more tanks, the opportunity cost of each additional tank in terms of autos

(Multiple Choice)

4.9/5 (39)

Assume that a consumer purchases only two products and there is a decrease in the consumer's income. The prices of the two products stay constant. The decrease in income will result in

(Multiple Choice)

4.8/5 (36)

When economists say that people act rationally in their self-interest, they mean that individuals

(Multiple Choice)

4.9/5 (36)

The economizing problem for individuals arises from the conflict between having relatively unlimited time and relatively limited jobs to do.

(True/False)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)