Exam 8: Cost-Based Inventories and Cost of Sales

Exam 1: The Framework for Financial Reporting79 Questions

Exam 2: Accounting Judgements129 Questions

Exam 3: Statements of Income and Comprehensive Income130 Questions

Exam 4: Statements of Financial Position and Changes in Equity; Disclosure Notes131 Questions

Exam 5: The Statement of Cash Flows177 Questions

Exam 7: Financial Assets: Cash and Receivables119 Questions

Exam 8: Cost-Based Inventories and Cost of Sales169 Questions

Exam 9: Property,Plant,and Equipment; Intangibles; and Goodwill191 Questions

Exam 10: Depreciation,Amortization,and Impairment165 Questions

Exam 11: Financial Instruments: Investments in Debt and Equity Securities118 Questions

Select questions type

On December 31,2013,a company had an item (that it sells regularly) which was returned by a customer because it was defective.Although it originally cost $150,and was sold to the customer for $280,it can be sold as used for only $140.Prior to making it saleable the company must spend $30 to repair it and the estimated cost to resell it is $20.The company expects a normal profit of 10 percent on the resale of damaged merchandise.The net realizable value (NRV) of this item is:

(Multiple Choice)

4.9/5  (40)

(40)

The following information relates to a firm with several similar products: Cost Retail Beginning inventory \ 29,000 \ 45,000 Purchases 140,000 190,000 Purchases discounts taken 3,000 Purchases returns 5,000 8,000 Freight-in 20,000 Net mark-ups 40,000 Net markdowns 12,000 Sales 190,000 Employee discounts 3,000 Using the retail inventory method and the average cost flow assumption (not LCM),what is ending inventory? When performing your calculations,round your cost ratios to one decimal point.

(Multiple Choice)

4.7/5 (35)

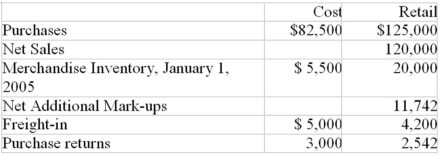

A small toy store uses the retail method FIFO,LCM to value its inventory.The following information is available for 2005:  Net Markdowns

Required: Determine the December 31,2005 inventory cost under the retail method-FIFO basis.

Net Markdowns

Required: Determine the December 31,2005 inventory cost under the retail method-FIFO basis.

(Essay)

4.8/5 (38)

On December 31 (end of the accounting period) a company completed an inventory count and included some merchandise that had been received but was not unpacked.No purchase had been recorded.The error causes an:

(Multiple Choice)

4.8/5 (33)

At the end of the first year of a firm's operations,the total inventory at cost was $200 and the market value (for purposes of Lower of Cost or NRV valuation) was $220.The corresponding values at the end of years 2 and 3 are as follows: Year 2 Year 3 Cost \ 400 \ 600 Market 340 640 Required: provide the adjusting entries at the end of years 2 and 3 to record inventory at Lower of Cost or NRV using:

(a) the direct reduction method,and

(b) the inventory allowance method.

(Essay)

4.7/5 (39)

Items on Harris's ledger for inventory that are purchased and correctly debited to 2013 purchases,but improperly included in 2013 ending inventory would have overstated both asset and pre-tax income of 2013.

(True/False)

4.8/5 (33)

Which of the following is not a true statement concerning a perpetual inventory system:

(Multiple Choice)

4.7/5 (47)

Complete the following schedule based on the data given below: Transaction Units Unit Cost 1. Beginning Inventory 4,000 \ 1.00 2. Purchase. 6,000 \ 1.10 3. Sale (a \ 4.00) 7,000 4. Purchase. 2,000 \ 1.30 Ending Cost of Inventory Goods Sold a. FIFO. \ \_\_ b. Annual weighted average \_\_ \_\_

(Essay)

4.8/5 (29)

Four different independent errors relating to inventory are described below.You are to indicate the dollar amount by which various financial statement components are misstated and whether the error causes each component to be too high or too low.For example,if the effect of the error is to cause the component to be too high by $300,you should enter + 300 in the appropriate column; if it makes the component too low by $750,enter $-750.If a component is unaffected,enter a 0.Similarly,if on financial statements of a later year the error would have counterbalanced on that later year's statements,enter a 0.A periodic inventory system is used unless specifically stated to the contrary.

(a) The 2001 ending inventory is understated by $400 and the related purchase on credit for that amount was not recorded until 2013.

(b) At the end of 2001,the company failed to recognize that $1,500 of inventory was in the hands of a consignee.At the end of 2013,a similar error was made and the cost of goods consigned out was $1,100.

(c) In running a total of inventory count sheets,a clerk included one line for $350 twice at the end of 2001; therefore,the inventory was overstated $350.

(d) On December 31,2001,a customer agreed to buy goods for $2,500 and asked that delivery be delayed until January 3,2013.The goods,on which the average mark-up was 40 percent of sale price,were still on hand on December 31.They were included in the 2001 inventory.The customer was properly billed for the goods,and the sale was recorded on December 31,2001. 2001 Statements 2002 Statements Owners' Cost of Error Assets Liabilities Equity Goods Sold (a) (b) (c) (d)

(Essay)

5.0/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)