Exam 7: Property Acquisitions and Cost Recovery Deductions

Exam 1: Taxes and Taxing Jurisdictions85 Questions

Exam 2: Policy Standards for a Good Tax85 Questions

Exam 3: Taxes As Transaction Costs82 Questions

Exam 4: Maxims of Income Tax Planning92 Questions

Exam 5: Tax Research82 Questions

Exam 6: Taxable Income From Business Operations116 Questions

Exam 7: Property Acquisitions and Cost Recovery Deductions116 Questions

Exam 8: Property Dispositions122 Questions

Exam 9: Nontaxable Exchanges107 Questions

Exam 10: Sole Proprietorships, Partnerships, Llcs, and S Corporations97 Questions

Exam 11: The Corporate Taxpayer103 Questions

Exam 12: The Choice of Business Entity102 Questions

Exam 13: Jurisdictional Issues in Business Taxation107 Questions

Exam 14: The Individual Tax Formula113 Questions

Exam 15: Compensation and Retirement Planning107 Questions

Exam 16: Investment and Personal Financial Planning109 Questions

Exam 17: Tax Consequences of Personal Activities93 Questions

Exam 18: The Tax Compliance Process86 Questions

Select questions type

MACRS depreciation for buildings is based on the straight-line method.

(True/False)

4.9/5  (39)

(39)

The after-tax cost of an expenditure is minimized when the expenditure is deductible in the current year.

(True/False)

4.9/5 (40)

Which of the following statements about tax basis is false?

(Multiple Choice)

4.7/5 (39)

In 2014, Rydin Company purchased one asset costing $38,400 and elected to expense the entire cost. However, Rydin could only deduct $21,000 of the Section 179 expense because of the taxable income limitation. In 2015, Rydin purchased tangible personalty costing $80,000. Rydin's taxable income without regard to any Section 179 deduction was $912,400. Compute Rydin's 2015 Section 179 deduction.

(Multiple Choice)

4.7/5 (38)

Song Company, a calendar year taxpayer, purchased a total of $214,400 tangible personalty in 2015. How much of this cost can Song elect to expense under Section 179?

(Multiple Choice)

4.9/5 (38)

Shelley purchased a residential apartment for $1,400,000 and placed it in service on September 5. Which of the following statements is false?

(Multiple Choice)

4.9/5 (42)

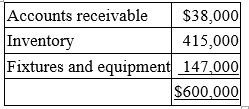

On April 2, Reid Inc., a calendar year taxpayer, paid a $750,000 lump-sum price to purchase a business. The appraised FMVs of the balance sheet assets were:  Which of the following statements is false?

Which of the following statements is false?

(Multiple Choice)

4.9/5 (50)

Poole Company made a $100,000 cash expenditure this year. Which of the following statements is false?

(Multiple Choice)

4.9/5 (37)

An asset's adjusted book basis and adjusted tax basis convey no information about the asset's fair market value.

(True/False)

4.7/5 (42)

Zola Inc. paid a $10,000 legal fee to the attorney who resolved a dispute over Zola's title to investment land. Zola's auditors required the corporation to expense the payment for financial statement purposes. The tax law required Zola to capitalize the payment to the basis of the land. This difference in accounting treatment results in a:

(Multiple Choice)

4.9/5 (33)

KJD Inc., a calendar year corporation, purchased $923,000 of equipment on November 13. This was KJD's only purchase of tangible personalty this year. KJD must use a midquarter convention to compute MACRS depreciation on the equipment.

(True/False)

4.9/5 (38)

Cobly Company, a calendar year taxpayer, made only one asset purchase this year: machinery costing $1,932,500. The machinery is 7-year recovery property, and Cobly placed it in service on October 12. How many months of MACRS depreciation on the machinery is Cobly allowed?

(Multiple Choice)

4.9/5 (35)

Terrance Inc., a calendar year taxpayer, purchased equipment for $2,765,000 and placed it in service on March 4, 2015. The equipment was seven-year recovery property and was the only depreciable asset that Terrance purchased during 2015.

a. Compute Terrance's tax depreciation with respect to the equipment for 2015 and 2016.

b. Compute Terrance's adjusted basis in the equipment in December 31, 2016.

c. How would your answer to a. change if Terrance placed the equipment in service in 2014 instead of 2015?

(Essay)

4.8/5 (35)

Richland Company purchased an asset in 2012 for $50,000 and sold it in 2015. The asset was 7-year recovery property. Richland's 2015 MACRS depreciation on the asset was $6,245.

(True/False)

4.7/5 (28)

Mallow Inc., which has a 35% tax rate, purchased a new business asset. First-year book depreciation was $37,225, and first-year MACRS depreciation was $55,025. As a result of this book/tax difference, Mallow recorded a $6,230 deferred tax asset.

(True/False)

4.9/5 (35)

Uqua Inc. purchased a depreciable asset for $189,000. First-year depreciation for book purposes was $22,000, and first-year MACRS depreciation was $37,800. If Uqua's marginal tax rate is 35%, the excess tax depreciation results in a $5,530:

(Multiple Choice)

4.8/5 (34)

The MACRS calculation is based on the estimated useful life of the depreciable asset.

(True/False)

4.7/5 (37)

Four years ago, Bettis Inc. paid a $5 million lump-sum price to purchase a business. Bettis allocated $600,000 of the price to goodwill. This year, Bettis' auditors required Bettis to write the goodwill down to $500,000 and record a $100,000 impairment expense. Because of the accounting treatment of goodwill, Bettis has a current:

(Multiple Choice)

4.8/5 (42)

Research and experimental expenditures are not deductible if they result in the development of a patented formula or process.

(True/False)

4.9/5 (37)

Mr. and Mrs. Carleton founded Carleton Industries in 1993. This year, an independent appraiser placed a $25 million value on Carleton's business; $5 million of the value was attributable to unrecorded goodwill. Which of the following statements is true?

(Multiple Choice)

4.7/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)