Exam 24: Segment Reporting

Exam 1: An Overview of the Australian External Reporting Environment70 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financial Reporting72 Questions

Exam 3: Theories of Accounting76 Questions

Exam 4: An Overview of Accounting for Assets77 Questions

Exam 5: Depreciation of Property, plant and Equipment77 Questions

Exam 6: Revaluations and Impairment Testing of Non-Current Assets76 Questions

Exam 7: Inventory75 Questions

Exam 8: Accounting for Intangibles77 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets76 Questions

Exam 10: An Overview of Accounting for Liabilities78 Questions

Exam 11: Accounting for Leases81 Questions

Exam 12: Accounting for Employee Benefits84 Questions

Exam 13: Share Capital and Reserves85 Questions

Exam 14: Accounting for Financial Instruments90 Questions

Exam 15: Revenue Recognition Issues79 Questions

Exam 16: The Statement of Comprehensive Income and Statement of Changes in Equity77 Questions

Exam 17: Accounting for Share-Based Payments77 Questions

Exam 18: Accounting for Income Taxes80 Questions

Exam 19: The Statement of Cash Flows77 Questions

Exam 20: Accounting for the Extractive Industries75 Questions

Exam 21: Accounting for General Insurance Contracts73 Questions

Exam 22: Accounting for Superannuation Plans77 Questions

Exam 23: Events Occurring After the End of the Reporting Period77 Questions

Exam 24: Segment Reporting77 Questions

Exam 25: Related Party Disclosures77 Questions

Exam 26: Earnings Per Share76 Questions

Exam 27: Accounting for Group Structures87 Questions

Exam 28: Further Consolidation Issues I: Accounting for Intragroup Transactions60 Questions

Exam 29: Further Consolidation Issues II: Accounting for Non-Controlling Interests44 Questions

Exam 30: Further Consolidation Issues IV: Accounting for Changes in the Degree of Ownership of a Subsidiary49 Questions

Exam 31: Accounting for Equity Investments,including Investments in Associates and Joint Arrangements70 Questions

Exam 32: Accounting for Foreign Currency Transactions78 Questions

Exam 33: Translating the Financial Statements of Foreign Operations52 Questions

Exam 34: Accounting for Corporate Social Responsibility73 Questions

Select questions type

Which of the following is not likely to be a 'chief operating decision maker' as referred to in AASB 8 Operating Segments?

(Multiple Choice)

4.8/5  (37)

(37)

An important argument for providing segmental information in the financial reports is:

(Multiple Choice)

4.8/5 (34)

The guidelines to determine that a segment is reportable in accordance with AASB 8 Operating Segments includes:

(Multiple Choice)

4.9/5 (49)

AASB 8 identifies a number of purposes for segment data.These include to:

(Multiple Choice)

4.9/5 (34)

In accordance with AASB 8 Operating Segments,which of the following statements is incorrect?

(Multiple Choice)

5.0/5 (33)

Discuss the specific financial information items that must be disclosed in relation to segment reporting.

(Essay)

4.9/5 (42)

The guidelines to determine that a segment is reportable in accordance with AASB 8 Operating Segments includes:

(Multiple Choice)

4.8/5 (31)

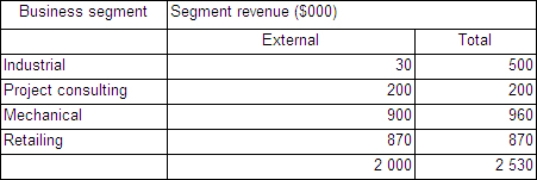

Gandulf Ltd provides the following segment information: Segment\nobreakspaceresult (\ 000) Business segment: Industrial manufacturing 500 Project consulting 90 Mechanical engineering 700 Retailing 140 Agriculture 70 Total 1500 Geographical segment: Australia 1000 Pacific Islands 340 US 160 Total 1500 Which of the segments are reportable applying only the segment asset test?

(Multiple Choice)

4.7/5 (31)

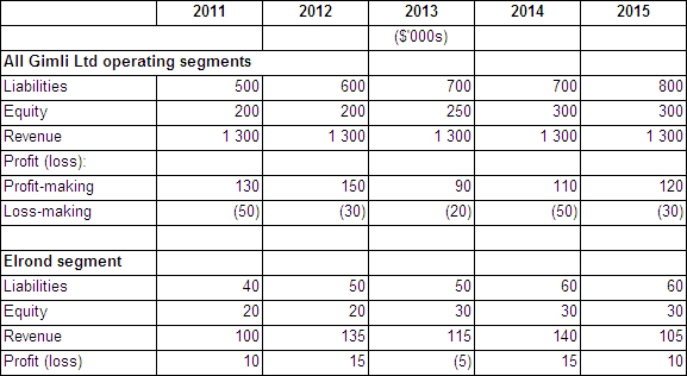

The following information relates to Gimli Ltd and its Elrond segment:  In accordance with AASB 8 Operating Segments,in which years is the Elrond segment a reportable segment?

In accordance with AASB 8 Operating Segments,in which years is the Elrond segment a reportable segment?

(Multiple Choice)

4.9/5 (38)

AASB 8 requires reconciliation of reported segments' amounts to the entity's reported amount for which of the following items?

(Multiple Choice)

4.9/5 (35)

Discuss the entity-wide disclosures in AASB 8 that need to been made about major customers.

(Essay)

4.8/5 (43)

Information about operating segments that do not meet any of the quantitative thresholds:

(Multiple Choice)

4.8/5 (34)

For a segment to be reportable,AASB 8 requires that majority of revenues be earned from external parties and the segment satisfies one of the three quantitative thresholds.

(True/False)

4.8/5 (29)

The guidelines for determining that a segment is reportable in accordance with AASB 8 include:

(Multiple Choice)

5.0/5 (36)

The core principle of AASB 8 Operating Segments is for a reporting entity to disclose information to enable users of its financial statements to evaluate the nature and financial effects of the business activities in which it engages and the economic environments in which it operates.

(True/False)

4.8/5 (48)

The following segment information relates to Tolkein Enterprises:  Applying the tests for identifying a reportable segment in accordance with AASB 8,which of the above segments qualify for reporting and do the segments satisfy the 75 per cent test?

Applying the tests for identifying a reportable segment in accordance with AASB 8,which of the above segments qualify for reporting and do the segments satisfy the 75 per cent test?

(Multiple Choice)

4.8/5 (45)

Edwards and Smith (1996)found that one of the main reasons companies resisted segment disclosures is:

(Multiple Choice)

4.9/5 (40)

AASB 8 does not require disclosure of a reportable segment if a segment is mainly transacting with related parties.

(True/False)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)