Exam 24: Segment Reporting

Exam 1: An Overview of the Australian External Reporting Environment70 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financial Reporting72 Questions

Exam 3: Theories of Accounting76 Questions

Exam 4: An Overview of Accounting for Assets77 Questions

Exam 5: Depreciation of Property, plant and Equipment77 Questions

Exam 6: Revaluations and Impairment Testing of Non-Current Assets76 Questions

Exam 7: Inventory75 Questions

Exam 8: Accounting for Intangibles77 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets76 Questions

Exam 10: An Overview of Accounting for Liabilities78 Questions

Exam 11: Accounting for Leases81 Questions

Exam 12: Accounting for Employee Benefits84 Questions

Exam 13: Share Capital and Reserves85 Questions

Exam 14: Accounting for Financial Instruments90 Questions

Exam 15: Revenue Recognition Issues79 Questions

Exam 16: The Statement of Comprehensive Income and Statement of Changes in Equity77 Questions

Exam 17: Accounting for Share-Based Payments77 Questions

Exam 18: Accounting for Income Taxes80 Questions

Exam 19: The Statement of Cash Flows77 Questions

Exam 20: Accounting for the Extractive Industries75 Questions

Exam 21: Accounting for General Insurance Contracts73 Questions

Exam 22: Accounting for Superannuation Plans77 Questions

Exam 23: Events Occurring After the End of the Reporting Period77 Questions

Exam 24: Segment Reporting77 Questions

Exam 25: Related Party Disclosures77 Questions

Exam 26: Earnings Per Share76 Questions

Exam 27: Accounting for Group Structures87 Questions

Exam 28: Further Consolidation Issues I: Accounting for Intragroup Transactions60 Questions

Exam 29: Further Consolidation Issues II: Accounting for Non-Controlling Interests44 Questions

Exam 30: Further Consolidation Issues IV: Accounting for Changes in the Degree of Ownership of a Subsidiary49 Questions

Exam 31: Accounting for Equity Investments,including Investments in Associates and Joint Arrangements70 Questions

Exam 32: Accounting for Foreign Currency Transactions78 Questions

Exam 33: Translating the Financial Statements of Foreign Operations52 Questions

Exam 34: Accounting for Corporate Social Responsibility73 Questions

Select questions type

Gollum Ltd provides the following segment information: Segment result (\ 000) Business segment: Industrial manufacturing (90) Project consulting 140 Mechanical engineering 20 Retailing (15) Agriculture 70 Geographical segment: Australia 100 Pacific Islands 40 US (15) There are no inter-segment sales.Which of the segments are reportable applying only the segment result test?

(Multiple Choice)

4.8/5  (36)

(36)

AASB 8 requires a number of reconciliations to be presented,including:

(Multiple Choice)

4.9/5 (45)

AASB 8 Operating Segments requires reconciliation of total reportable segment revenues,total profit or loss,total assets,total liabilities and other amounts disclosed for reportable segments to the corresponding amounts shown in the parent entity's separate financial statements.

(True/False)

4.8/5 (34)

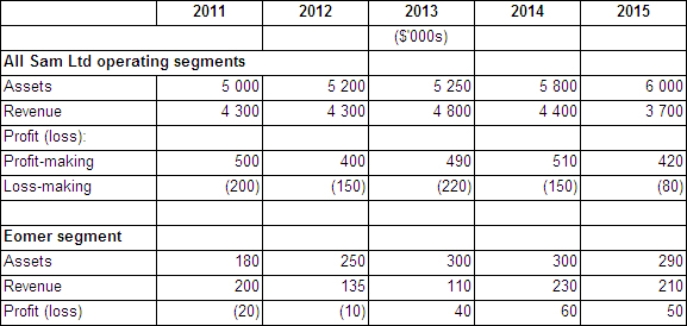

The following information relates to Sam Ltd and its Eomer segment:  In accordance with AASB 8 Operating Segments,in which years is the Eomer segment a reportable segment?

In accordance with AASB 8 Operating Segments,in which years is the Eomer segment a reportable segment?

(Multiple Choice)

4.8/5 (45)

IFRS 8 was issued as part of the ongoing process to converge IASB standards with the US accounting standards.

(True/False)

4.8/5 (35)

Management may be concerned that segment reporting will put the entity at competitive disadvantage,so it has been suggested that it can avoid providing accurate segment reports through opportunistic interpretation of the definition of a business segment.

(True/False)

4.8/5 (43)

The following information is provided for Gandalf Ltd: Business segment Segment revenue (\ 000) Segment result (\ 000) Segment assets (\ 000) Retailing 200 80 3000 Light manufacturing 1650 (2600) 2500 Mining 700 250 1000 Marine transport 3700 945 6000 General insurance 2320 1175 2500 Total 8570 (150) 15000 Which segments are reportable according to the guidelines provided in AASB 8?

(Multiple Choice)

4.8/5 (26)

AASB 8 bans the disclosure of segments that do not pass the '10 per cent test'.

(True/False)

4.8/5 (35)

Research has shown that companies only provide segment information when it is required by accounting regulation.

(True/False)

4.8/5 (40)

The consolidated statement of comprehensive income provides an indication of the aggregated financial performance of many dissimilar entities.

(True/False)

4.8/5 (48)

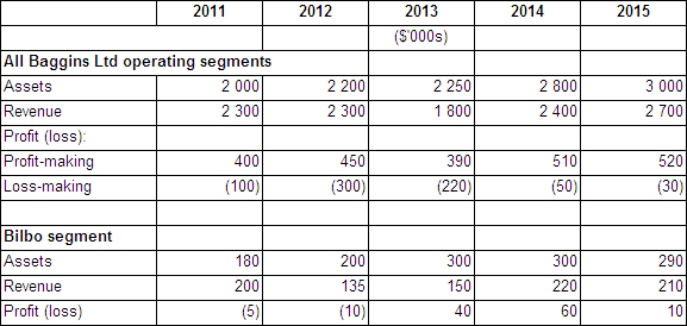

The following information relates to Baggins Ltd and its Bilbo segment:  In accordance with AASB 8 Operating Segments,in which years is the Bilbo segment a reportable?

In accordance with AASB 8 Operating Segments,in which years is the Bilbo segment a reportable?

(Multiple Choice)

4.8/5 (35)

AASB 8 allows reportable segments to be combined as a single operating segment if:

(a)they exhibit similar long-term financial performance; and (b)they are similar in all of the appropriate factors identified in the standard in relation to segment revenues,expenses,assets and liabilities.

(True/False)

4.8/5 (28)

In the situation where an entity has invested in segments that are diverse:

(Multiple Choice)

4.8/5 (32)

The following segment information is presented for Hobbitt Ltd: Business segment Segment revenue (\ 000) Segment result (\ 000) Segment assets (\ 000) Retailing 2000 950 14500 Light manufacturing 900 (60) 2000 Mining 800 (570) 3000 Marine transport 5900 1870 15060 General insurance 400 85 440 Total 10000 2275 35000 Which segments are reportable according to the guidelines provided in AASB 8?

(Multiple Choice)

4.9/5 (32)

Which of the following characteristics of a segment is not considered reportable in AASB 8 Operating Segments?

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)