Exam 7: A: Consolidated Financial Statements - Ownership Patterns and Income Taxes

Exam 1: The Equity Method of Accounting for Investments121 Questions

Exam 1: A: the Equity Method of Accounting for Investments121 Questions

Exam 2: Consolidation of Financial Information116 Questions

Exam 2: A: Consolidation of Financial Information116 Questions

Exam 3: Consolidations - Subsequent to the Date of Acquisition120 Questions

Exam 3: A: Consolidations - Subsequent to the Date of Acquisition120 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership117 Questions

Exam 4: A: Consolidated Financial Statements and Outside Ownership117 Questions

Exam 5: Consolidated Financial Statements Intra-Entity Asset Transactions123 Questions

Exam 5: A: Consolidated Financial Statements Intra-Entity Asset Transactions123 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues117 Questions

Exam 6: A: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues117 Questions

Exam 7: Consolidated Financial Statements - Ownership Patterns and Income Taxes112 Questions

Exam 7: A: Consolidated Financial Statements - Ownership Patterns and Income Taxes112 Questions

Exam 8: Segment and Interim Reporting105 Questions

Exam 8: A: Segment and Interim Reporting115 Questions

Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk99 Questions

Exam 9: A: Foreign Currency Transactions and Hedging Foreign Exchange Risk99 Questions

Exam 10: Translation of Foreign Currency Financial Statements96 Questions

Exam 10: A: Translation of Foreign Currency Financial Statements96 Questions

Exam 11: Worldwide Accounting Diversity and International Accounting Standards63 Questions

Exam 11: A: Worldwide Accounting Diversity and International Accounting Standards63 Questions

Exam 12: Financial Reporting and the Securities and Exchange Commission76 Questions

Exam 12: A: Financial Reporting and the Securities and Exchange Commission76 Questions

Exam 13: Accounting for Legal Reorganizations and Liquidations75 Questions

Exam 13: A: Accounting for Legal Reorganizations and Liquidations78 Questions

Exam 14: Partnerships: Formation and Operation89 Questions

Exam 14: A: Partnerships: Formation and Operation89 Questions

Exam 15: Partnerships: Termination and Liquidation69 Questions

Exam 15: A: Partnerships: Termination and Liquidation69 Questions

Exam 16: Accounting for State and Local Governments, Part I83 Questions

Exam 16: A: Accounting for State and Local Governments, Part I83 Questions

Exam 17: Accounting for State and Local Governments, Part II42 Questions

Exam 17: A: Accounting for State and Local Governments, Part II47 Questions

Exam 18: Accounting for Not-For-Profit Entities72 Questions

Exam 18: A: Accounting for Not-For-Profit Entities72 Questions

Exam 19: Accounting for Estates and Trusts81 Questions

Exam 19: A: Accounting for Estates and Trusts81 Questions

Select questions type

B Co.owned 70% of the voting common stock of C Corp.; C Corp.owned 20% of B Co.There were no excess-value allocations at the dates the investments were acquired.For 2018, B Co.and C Corp.reported net income (not including the investment) of $600,000 and $300,000, respectively.B Co.and C Corp.declared dividends of $80,000 and $60,000, respectively.

Required:

Prepare a schedule showing net income attributable to B Co.'s controlling interest for 2018 using the treasury stock approach.

(Essay)

5.0/5  (34)

(34)

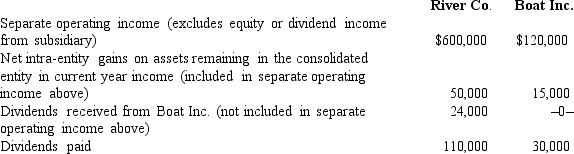

River Co. owns 80% of Boat Inc. The two companies file a consolidated income tax return and River uses the initial value method to account for the investment. The following information is available from the two companies' financial statements:

The income tax rate was 30%.

-The amount of income tax expense that should be assigned to Boat using the separate return method is approximately:

The income tax rate was 30%.

-The amount of income tax expense that should be assigned to Boat using the separate return method is approximately:

(Multiple Choice)

4.9/5 (41)

Horse Corporation acquires all of Pony, Inc.for $300,000 cash.On that date, Pony has net assets with fair value of $250,000 but a book value and tax basis of $200,000.The tax rate is 40 percent.Prior to this date, neither Horse nor Pony has reported any deferred income tax assets or liabilities.What amount of goodwill should be recognized on the date of the acquisition?

(Multiple Choice)

4.8/5 (40)

-Compute Whitton's accrual-based consolidated net income for 2018.

-Compute Whitton's accrual-based consolidated net income for 2018.

(Multiple Choice)

4.9/5 (39)

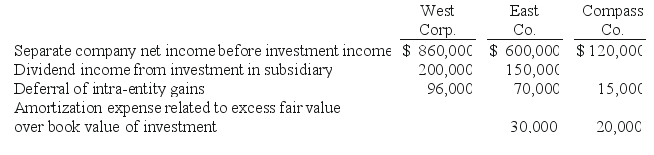

West Corp. owns 70% of the voting common stock of East Co. East owns 60% of Compass Co. West and East both use the initial value method to account for their investments. The following information is available from the financial statements and records of the three companies:

Separate company net income includes intra-entity gains before the consolidating deferral but does not include dividend income from investment in subsidiary.

-What amount of dividends should West Corp.recognize in its consolidated net income with respect to dividends received from Compass Co.?

Separate company net income includes intra-entity gains before the consolidating deferral but does not include dividend income from investment in subsidiary.

-What amount of dividends should West Corp.recognize in its consolidated net income with respect to dividends received from Compass Co.?

(Multiple Choice)

4.7/5 (41)

Explain how the treasury stock approach treats shares of the parent's common stock that are owned by the subsidiary and the rationale behind the approach.

(Essay)

4.8/5 (36)

What method is used in consolidation to account for a subsidiary's ownership of shares of its parent corporation?

(Short Answer)

4.8/5 (38)

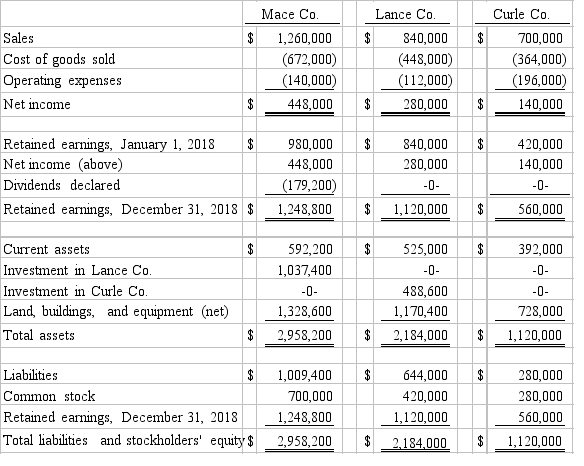

On January 1, 2017, Mace Co. acquired 75% of Lance Co.'s outstanding common stock. On the same date, Lance acquired an 80% interest in Curle Co. Both of these investments were acquired when book value was equal to fair value of identifiable net assets acquired. Both of these investments were accounted using the initial value method. Only Mace declared dividends in any year. Mace declared dividends each year equal to 40% of its separate net income before the calculation of any of its investment income. Separate net income totals for 2017, not including investment income for any company, were as follows:

Following are the 2018 financial statements for these three companies. Curle made numerous transfers of inventory to Lance since the takeover: $112,000 (2017) and $140,000 (2018). These transfers included the same markup applicable to Curle's outside sales. In each of these years, Lance held 20% of the inventory it bought from Curle and then sold that inventory to outsiders in the following year.

An effective income tax rate of 45% was applicable to all companies.

Following are the 2018 financial statements for these three companies. Curle made numerous transfers of inventory to Lance since the takeover: $112,000 (2017) and $140,000 (2018). These transfers included the same markup applicable to Curle's outside sales. In each of these years, Lance held 20% of the inventory it bought from Curle and then sold that inventory to outsiders in the following year.

An effective income tax rate of 45% was applicable to all companies.

-Required:

Determine the net income attributable to the noncontrolling interest in Lace for the year 2018.

-Required:

Determine the net income attributable to the noncontrolling interest in Lace for the year 2018.

(Essay)

4.8/5 (30)

On January 1, 2017, Mace Co. acquired 75% of Lance Co.'s outstanding common stock. On the same date, Lance acquired an 80% interest in Curle Co. Both of these investments were acquired when book value was equal to fair value of identifiable net assets acquired. Both of these investments were accounted using the initial value method. Only Mace declared dividends in any year. Mace declared dividends each year equal to 40% of its separate net income before the calculation of any of its investment income. Separate net income totals for 2017, not including investment income for any company, were as follows:

Following are the 2018 financial statements for these three companies. Curle made numerous transfers of inventory to Lance since the takeover: $112,000 (2017) and $140,000 (2018). These transfers included the same markup applicable to Curle's outside sales. In each of these years, Lance held 20% of the inventory it bought from Curle and then sold that inventory to outsiders in the following year.

An effective income tax rate of 45% was applicable to all companies.

-Required:

Determine net income attributable to the noncontrolling interest in Curle for the year 2018.

(Essay)

4.8/5 (35)

On January 1, 2018, Youder Inc.bought 120,000 shares of Nopple Co.for $384,000, giving Youder 30% ownership and the ability to apply significant influence to the operating and financing decisions of Nopple.Youder anticipated holding this investment for an indefinite time.In making this acquisition, Youder paid an amount equal to the book value for these shares.The fair value of each asset and liability was the same as its book value.Dividends and income for Nopple for 2018 were as follows:

Dividends declared and paid: $ .40 per share

Income before income tax provision: $400,000

Required:

Assume a 40% income tax rate.Prepare all necessary journal entries for Youder for 2018 beginning at acquisition and ending at tax accrual.

(Essay)

4.7/5 (35)

Alpha Corporation owns 100 percent of Beta Company, and Beta owns 80 percent of Gamma, Inc., all of which are domestic corporations. There were no excess allocation values at the date of acquisition of the subsidiaries. Information for the three companies for the year ending December 31, 2018 follows:

-What is the net income attributable to the noncontrolling interest in Gamma for 2018?

-What is the net income attributable to the noncontrolling interest in Gamma for 2018?

(Multiple Choice)

4.8/5 (33)

White Company owns 60% of Cody Company. Separate tax returns are required. For 2017, White's operating income (excluding taxes and any income from Cody) was $300,000 while Cody reported a pretax income of $125,000. During the period, Cody declared total dividends of $25,000; $15,000 (60%) to White and $10,000 to the noncontrolling

-Compute White's deferred income taxes for 2018.

(Multiple Choice)

4.8/5 (40)

-The accrual-based net income of Beagle Co.is calculated to be

-The accrual-based net income of Beagle Co.is calculated to be

(Multiple Choice)

4.8/5 (35)

-The accrual-based net income of Eckston Inc.is calculated to be

(Multiple Choice)

4.9/5 (33)

River Co. owns 80% of Boat Inc. The two companies file a consolidated income tax return and River uses the initial value method to account for the investment. The following information is available from the two companies' financial statements:

The income tax rate was 30%.

-How would the 10% Investment in Prescott owned by Bell be presented in the consolidated balance sheet?

(Multiple Choice)

4.8/5 (37)

On January 1, 2018, a subsidiary buys 8 percent of the outstanding voting stock of its parent corporation.The payment of $350,000 exceeded book value of the acquired shares by $50,000, attributable to a copyright with a 10-year useful life.During the year, the parent reported operating income of $675,000 (excluding investment income from the subsidiary), and paid $100,000 in dividends.If the treasury stock approach is used, how is the Investment in Parent Stock reported in the consolidated balance sheet at December 31, 2018?

(Multiple Choice)

4.8/5 (31)

C Co.currently owns 80% of D Co.and several other subsidiaries.C Co.is interested in gaining control of H Co.Why might C Co.allow D Co.to acquire H Co., rather than purchasing H Co.directly?

(Essay)

4.8/5 (39)

Required:

Under the treasury stock approach, what is Jull's net income attributable to the controlling interest in Solaver Co..?

(Essay)

4.9/5 (37)

Required:

Under the treasury stock approach, what is the net income attributable to the noncontrolling interest?

(Essay)

4.8/5 (41)

Gamma Co.owns 80% of Delta Corp., and Delta Corp.owns 15% of Gamma Co.The two companies use the treasury stock approach to account for mutual ownership.How should Delta Corp.'s ownership interest in Gamma Co.be accounted for in the consolidation?

(Essay)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)