Exam 11: Optimal Portfolio Choice and the Capital Asset Pricing Model

Exam 1: The Corporation42 Questions

Exam 2: Introduction to Financial Statement Analysis74 Questions

Exam 3: Arbitrage and Financial Decision Making79 Questions

Exam 4: The Time Value of Money84 Questions

Exam 5: Interest Rates69 Questions

Exam 6: Valuing Bonds104 Questions

Exam 7: Valuing Stocks88 Questions

Exam 8: Investment Decision Rules83 Questions

Exam 9: Fundamentals of Capital Budgeting94 Questions

Exam 10: Capital Markets and the Pricing of Risk98 Questions

Exam 11: Optimal Portfolio Choice and the Capital Asset Pricing Model108 Questions

Exam 12: Estimating the Cost of Capital108 Questions

Exam 13: Investor Behaviour and Capital Market Efficiency74 Questions

Exam 14: Financial Options56 Questions

Exam 15: Option Valuation42 Questions

Exam 16: Real Options57 Questions

Exam 17: Capital Structure in a Perfect Market86 Questions

Exam 18: Debt and Taxes84 Questions

Exam 19: Financial Distress, managerial Incentives, and Information99 Questions

Exam 20: Payout Policy92 Questions

Exam 21: Capital Budgeting and Valuation With Leverage94 Questions

Exam 22: Valuation and Financial Modelling: a Case Study47 Questions

Exam 23: The Mechanics of Raising Equity Capital49 Questions

Exam 24: Debt Financing49 Questions

Exam 25: Leasing58 Questions

Exam 26: Working Capital Management45 Questions

Exam 27: Short-Term Financial Planning49 Questions

Exam 28: Mergers and Acquisitions52 Questions

Exam 29: Corporate Governance49 Questions

Exam 30: Risk Management52 Questions

Exam 31: International Corporate Finance45 Questions

Select questions type

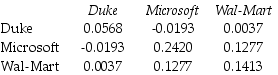

Use the table for the question(s) below.

Consider the following covariances between securities:

-The variance on a portfolio that is made up of a $6,000 investment in Microsoft stock and a $4,000 investment in Wal-Mart stock is closest to:

-The variance on a portfolio that is made up of a $6,000 investment in Microsoft stock and a $4,000 investment in Wal-Mart stock is closest to:

(Essay)

4.7/5  (38)

(38)

Consider an equally weighted portfolio that contains 20 stocks.If the average volatility of these stocks is 35% and the average correlation between the stocks is .4,then the volatility of this equally weighted portfolio is closest to:

(Multiple Choice)

4.9/5 (23)

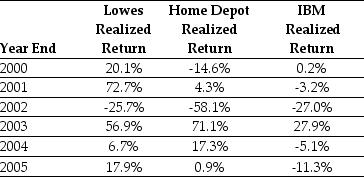

Use the table for the question(s) below.

Consider the following returns:

-The variance on a portfolio that is made up of equal investments in Lowes and Home Depot stock is closest to:

-The variance on a portfolio that is made up of equal investments in Lowes and Home Depot stock is closest to:

(Multiple Choice)

4.8/5 (40)

A portfolio is efficient if and only if ________ of every available security equals its ________.

(Multiple Choice)

4.8/5 (32)

The beta of a security captures the security's ________ to market risk.

(Multiple Choice)

4.8/5 (40)

What is the efficient frontier and how does it change when more stocks are used to construct portfolios?

(Essay)

4.7/5 (40)

Both conservative and aggressive investors will choose to hold the same portfolio of risky assets,

(Multiple Choice)

4.9/5 (33)

If investors have homogeneous expectations,then each investor will identify ________ portfolio as having ________ Sharpe ratio in the economy.

(Multiple Choice)

4.8/5 (37)

Use the table for the question(s) below.

Consider the following returns:

-The correlation between Lowes' and Home Depot's returns is closest to:

(Multiple Choice)

4.8/5 (28)

Consider an equally weighted portfolio that contains 100 stocks.If the average volatility of these stocks is 50% and the average correlation between the stocks is .7,then the volatility of this equally weighted portfolio is closest to:

(Multiple Choice)

4.8/5 (39)

Suppose you invest $15,000 in Merck stock and $25,000 in Home Depot stock.You expect a return of 16% for Merck and 12% for Home Depot.What is the expected return on your portfolio?

(Multiple Choice)

4.9/5 (31)

The capital market line (CML)represents ________ expected return available for ________ level of volatility.

(Multiple Choice)

4.8/5 (39)

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

-The expected return of a portfolio that consists of a long position of $10,000 in Wal-Mart and a short position of $2,000 in Microsoft is closest to:

-The expected return of a portfolio that consists of a long position of $10,000 in Wal-Mart and a short position of $2,000 in Microsoft is closest to:

(Multiple Choice)

4.8/5 (32)

Aggressive investors will invest more,choosing a portfolio that is near ________ or even beyond it by buying stocks on margin.

(Multiple Choice)

4.8/5 (34)

Consider a portfolio consisting of only Microsoft and Wal-Mart stock.Calculate the volatility of such a portfolio when the weight on Microsoft stock is 0%,25%,50%,75%,and 100%.

(Essay)

4.8/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)