Exam 11: Optimal Portfolio Choice and the Capital Asset Pricing Model

Exam 1: The Corporation42 Questions

Exam 2: Introduction to Financial Statement Analysis74 Questions

Exam 3: Arbitrage and Financial Decision Making79 Questions

Exam 4: The Time Value of Money84 Questions

Exam 5: Interest Rates69 Questions

Exam 6: Valuing Bonds104 Questions

Exam 7: Valuing Stocks88 Questions

Exam 8: Investment Decision Rules83 Questions

Exam 9: Fundamentals of Capital Budgeting94 Questions

Exam 10: Capital Markets and the Pricing of Risk98 Questions

Exam 11: Optimal Portfolio Choice and the Capital Asset Pricing Model108 Questions

Exam 12: Estimating the Cost of Capital108 Questions

Exam 13: Investor Behaviour and Capital Market Efficiency74 Questions

Exam 14: Financial Options56 Questions

Exam 15: Option Valuation42 Questions

Exam 16: Real Options57 Questions

Exam 17: Capital Structure in a Perfect Market86 Questions

Exam 18: Debt and Taxes84 Questions

Exam 19: Financial Distress, managerial Incentives, and Information99 Questions

Exam 20: Payout Policy92 Questions

Exam 21: Capital Budgeting and Valuation With Leverage94 Questions

Exam 22: Valuation and Financial Modelling: a Case Study47 Questions

Exam 23: The Mechanics of Raising Equity Capital49 Questions

Exam 24: Debt Financing49 Questions

Exam 25: Leasing58 Questions

Exam 26: Working Capital Management45 Questions

Exam 27: Short-Term Financial Planning49 Questions

Exam 28: Mergers and Acquisitions52 Questions

Exam 29: Corporate Governance49 Questions

Exam 30: Risk Management52 Questions

Exam 31: International Corporate Finance45 Questions

Select questions type

We can determine the appropriate risk premium for an investment from its ________ with the efficient portfolio.

(Multiple Choice)

4.7/5  (37)

(37)

To identify the efficient portfolio we must know ________,________,and ________ between investments.

(Multiple Choice)

4.9/5 (37)

A hyperbola curve represents the set of portfolios that we can create using ________ weights.

(Multiple Choice)

4.8/5 (28)

Use the information for the question(s) below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT) at $50 per share, 200 shares of Lowes (LOW) at $30 per share, and 100 shares of Ball Corporation (BLL) at $40 per share.

-The weight on Abbott Labs in your portfolio is:

(Multiple Choice)

4.8/5 (37)

Use the information for the question(s) below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT) at $50 per share, 200 shares of Lowes (LOW) at $30 per share, and 100 shares of Ball Corporation (BLL) at $40 per share.

-The weight on Lowes in your portfolio is:

(Multiple Choice)

4.7/5 (37)

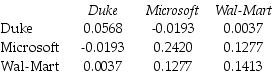

Use the table for the question(s) below.

Consider the following covariances between securities:

-What is the variance on a portfolio that has $3,000 invested in Duke Energy,$4,000 invested in Microsoft,and $3,000 invested in Wal-Mart stock?

-What is the variance on a portfolio that has $3,000 invested in Duke Energy,$4,000 invested in Microsoft,and $3,000 invested in Wal-Mart stock?

(Essay)

4.8/5 (46)

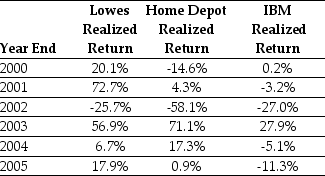

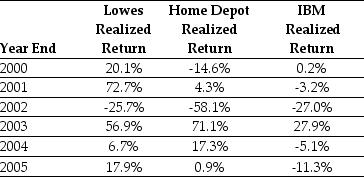

Use the table for the question(s) below.

Consider the following returns:

-Calculate the covariance between Home Depot's and IBM's returns.

-Calculate the covariance between Home Depot's and IBM's returns.

(Essay)

4.9/5 (35)

The efficient portfolio offers ________ Sharpe ratio and therefore ________ risk-return tradeoff available.

(Multiple Choice)

4.8/5 (44)

Use the table for the question(s) below.

Consider the following returns:

-The volatility on Lowes' returns is closest to:

-The volatility on Lowes' returns is closest to:

(Multiple Choice)

4.8/5 (37)

Suppose that you want to maximize your expected return without increasing your risk.How can you achieve this goal? Without increasing your risk,what is the maximum expected return you can expect?

(Essay)

4.8/5 (34)

the CAPM allows us to identify the efficient portfolio of risky assets without having any knowledge of the ________ of each security.

(Multiple Choice)

4.8/5 (40)

The relationship between risk and return for individual securities becomes evident only when we measure ________.

(Multiple Choice)

4.9/5 (39)

Use the information for the question(s) below.

Suppose that you currently have $250,000 invested in a portfolio with an expected return of 12% and a volatility of 10%. The efficient (tangent) portfolio has an expected return of 17% and a volatility of 12%. The risk-free rate of interest is 5%.

-You want to maximize your expected return without increasing your risk.Without increasing your volatility beyond its current 10%,the maximum expected return you could earn is closest to:

(Multiple Choice)

4.9/5 (29)

Use the table for the question(s) below.

Consider the following returns:

-The volatility on IBM's returns is closest to:

(Multiple Choice)

4.8/5 (36)

Use the information for the question(s) below.

You are presently invested in the Luther Fund, a broad-based mutual fund that invests in stocks and other securities. The Luther Fund has an expected return of 14% and a volatility of 20%. Risk-free Treasury Bills are currently offering returns of 4%. You are considering adding a precious metals fund to your current portfolio. The metals fund has an expected return of 10%, a volatility of 30%, and a correlation of -.20 with the Luther Fund.

-The expected return on the precious metals fund is closest to:

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)