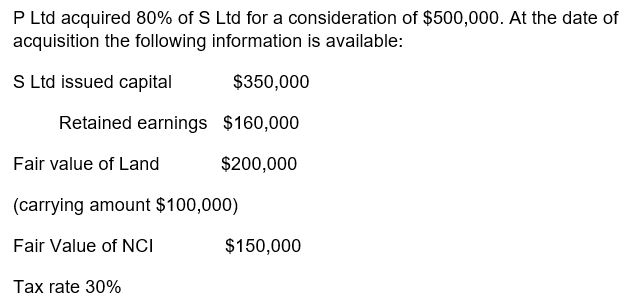

Exam 5: Non-Controlling Interest

Exam 1: Text Objectives and Introduction to Consolidation28 Questions

Exam 2: Principles of Consolidation42 Questions

Exam 3: Fair Value Adjustments and Tax Effects34 Questions

Exam 4: Intra-Group Transactions36 Questions

Exam 5: Non-Controlling Interest37 Questions

Exam 6: Partly-Owned Subsidiaries: Indirect Non-Controlling Interest27 Questions

Exam 7: Consolidated Cash Flow Statements25 Questions

Exam 8: Accounting for Joint Arrangements44 Questions

Exam 9: Accounting for Associates and Joint Ventures: the Equity Method37 Questions

Exam 10: Translation and Consolidation of Foreign Currency Financial Statements31 Questions

Exam 11: Segment Reporting by Diversified Entities27 Questions

Select questions type

Preference shares of a subsidiary not owned by the parent company will be included as part of the NCI.

(True/False)

4.8/5  (38)

(38)

The effect of all intra group transactions must be adjusted in calculating the NCI share of subsidiary profits.

(True/False)

4.7/5 (32)

A subsidiary's recorded profits and retained earnings must be adjusted for unrealised profits prior to calculation of NCI allocation.The adjustments apply to:

(Multiple Choice)

4.7/5 (41)

If A owns 80% of B and B owns 75% of C,A's ownership interest in B and C is characterised as direct.

(True/False)

4.9/5 (26)

Discuss the effect of intra group transactions on the calculation of the NCI share of subsidiary profits and retained earnings

(Essay)

4.9/5 (32)

The fair value method of measuring NCI includes an amount representing the non controlling shareholder's interest in goodwill.

(True/False)

4.7/5 (27)

The ownership interests in a group which includes partly owned subsidiaries consist of:

(Multiple Choice)

4.8/5 (42)

P Ltd purchased 80% of the issued ordinary shares of S Ltd.S Ltd capital structure is: Ordinary shares 200,000 fully paid shares x $1

Preference shares 50,000 fully paid shares x $1

Preference shares have the same rights as ordinary shares

The NCI in S Ltd is:

(Multiple Choice)

4.8/5 (34)

Accounting Standard AASB3 Business combinations allows the choice of measuring NCI using either the fair value method or the proportionate interest method.

(True/False)

4.7/5 (26)

Unrealised intra-group profit in opening inventory of a parent company is:

(Multiple Choice)

4.9/5 (40)

The disclosure of non controlling interest proportion of each equity balance in the consolidated financial statements provides useful information on:

(Multiple Choice)

4.8/5 (36)

Is the proprietary concept of consolidation is consistent with the proportional consolidation method?

(Essay)

4.9/5 (38)

-Using the proportionate interest goodwill method,goodwill on acquisition is:

-Using the proportionate interest goodwill method,goodwill on acquisition is:

(Multiple Choice)

4.8/5 (32)

The measurement of the NCI allocation will be based on the subsidiary company's equity account balances.

(True/False)

4.8/5 (30)

When an investment in a subsidiary is impaired,any impairment losses will be:

(Multiple Choice)

4.9/5 (36)

Company A owns 40% of Company B and this ownership is deemed to represent control.The non controlling interest in B is:

(Multiple Choice)

4.9/5 (42)

In preparing a consolidated financial report,the parent entity consolidates:

(Multiple Choice)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)