Exam 13: Risk and the Pricing of Options

Exam 1: Corporate Finance and the Financial Manager93 Questions

Exam 2: Introduction to Financial Statement Analysis122 Questions

Exam 3: The Valuation Principle: the Foundation of Financial Decision Making120 Questions

Exam 4: The Time Value of Money101 Questions

Exam 5: Interest Rates118 Questions

Exam 6: Bonds122 Questions

Exam 7: Valuing Stocks122 Questions

Exam 8: Investment Decision Rules136 Questions

Exam 9: Fundamentals of Capital Budgeting108 Questions

Exam 10: Risk and Return in Capital Markets101 Questions

Exam 11: Systematic Risk and the Equity Risk Premium102 Questions

Exam 12: Determining the Cost of Capital107 Questions

Exam 13: Risk and the Pricing of Options112 Questions

Exam 14: Raising Equity Capital106 Questions

Exam 15: Debt Financing112 Questions

Exam 16: Capital Structure114 Questions

Exam 17: Payout Policy101 Questions

Exam 18: Financial Modelling and Pro Forma Analysis124 Questions

Exam 19: Working Capital Management122 Questions

Exam 20: Short-Term Financial Planning105 Questions

Exam 21: Risk Management111 Questions

Exam 22: International Corporate Finance113 Questions

Exam 23: Leasing88 Questions

Exam 24: Mergers and Acquisitions80 Questions

Exam 25: Corporate Governance53 Questions

Select questions type

When the exercise price of a call option is higher than the current price of the stock,the option is said to be:

(Multiple Choice)

4.8/5  (40)

(40)

ABX corporation stock is currently trading for $37.60.A one-year European call option on ABX is currently trading for $7.23,and a one-year European put option on ABX with the same strike price is currently trading for $0.76.If the stock pays no dividends,and the risk-free rate is 3% per year,what is the strike price of the options?

(Multiple Choice)

4.8/5 (41)

The Black-Scholes formula is notable because it does NOT require us to know:

(Multiple Choice)

4.9/5 (37)

Standard stock options are traded and bought and sold through dealers only and cannot be bought via an exchange.

(True/False)

4.8/5 (37)

You have shorted a call option on WSJ stock with a strike price of $50.The option will expire in exactly six months.If the stock is trading at $60 in three months,what will you owe for each share in the contract?

(Multiple Choice)

4.8/5 (40)

You have shorted a call option on WSJ stock with a strike price of $50.The option will expire in exactly six months.If the stock is trading at $45 in three months,what will you owe for each share in the contract?

(Multiple Choice)

4.7/5 (37)

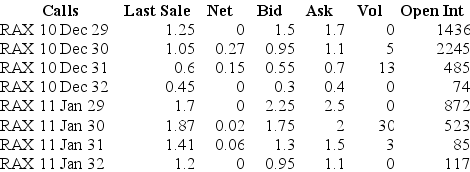

Use the table for the questions below

Consider the following information on options from the CBOE for Rackspace.

-Assume you want to sell 20 call option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

-Assume you want to sell 20 call option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

(Multiple Choice)

4.9/5 (32)

An investor purchases a call option and its underlying stock on the same day.If the stock appreciates by 25%,the call option will appreciate by:

(Multiple Choice)

4.9/5 (40)

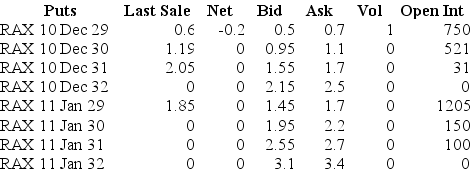

Use the table for the questions below

Consider the following information on options from the CBOE for Rackspace.

-Assume you want to sell 20 put option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

(Multiple Choice)

4.8/5 (38)

________ is the relationship between the value of a stock,a bond,and call and put options on the same stock with the same exercise price.

(Multiple Choice)

4.8/5 (35)

The price of a European call option on Lululemon stock with an exercise price of $34.50 and one year to expiry is trading at $2.52.The current price of the stock is $34,and the risk-free rate is 4%.With no arbitrage,what must be the price of a European put on Lululemon with an exercise price of $34.50?

(Multiple Choice)

4.9/5 (33)

The ________ side of an options contract has the option to exercise,while the ________ side has an obligation to fulfill the contract.

(Multiple Choice)

4.9/5 (41)

Suppose a stock is currently trading for $35,and in one period it will either increase to $38 or decrease to $33.If the one-period risk-free rate is 6%,what is the price of a European put option that expires in one period and has an exercise price of $36?

(Multiple Choice)

4.7/5 (31)

A put option on a stock has an exercise price of $31.If the stock price at expiration is $33.40,what is the option payoff for a short put position?

(Multiple Choice)

4.9/5 (34)

You pay $3.25 for a call option on Luther Industries that expires in three months with a strike price of $40.00.Three months later,at expiration,Luther Industries is trading at $41.00 per share.Your profit per share on this transaction is closest to:

(Multiple Choice)

4.9/5 (36)

Debt holders can be thought as owning the firm but having ________ a call option on the assets of the firm with a strike price equal to ________.

(Multiple Choice)

4.9/5 (28)

A call option on a stock has an exercise price of $22.25.If the stock price at expiration is $25,what is the option payoff for a long call position?

(Multiple Choice)

4.9/5 (34)

A(n)________ in the volatility of assets of the firm benefits ________ at a cost to debt holders.

(Multiple Choice)

4.8/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)