Exam 24: Cost Allocation and Responsibility Accounting

Exam 1: Accounting and the Business Environment143 Questions

Exam 2: Recording Business Transactions156 Questions

Exam 3: The Adjusting Process152 Questions

Exam 4: Completing the Accounting Cycle156 Questions

Exam 5: Merchandising Operations160 Questions

Exam 6: Merchandise Inventory155 Questions

Exam 7: Accounting Information Systems137 Questions

Exam 8: Internal Control and Cash160 Questions

Exam 9: Receivables138 Questions

Exam 10: Plant Assets, Natural Resources, and Intangibles151 Questions

Exam 11: Current Liabilities and Payroll162 Questions

Exam 12: Partnerships161 Questions

Exam 13: Corporations158 Questions

Exam 14: Long-Term Liabilities151 Questions

Exam 15: Investments135 Questions

Exam 16: The Statement of Cash Flows154 Questions

Exam 17: Financial Statement Analysis112 Questions

Exam 18: Introduction to Managerial Accounting179 Questions

Exam 19: Job Order Costing152 Questions

Exam 20: Process Costing144 Questions

Exam 21: Cost-Volume-Profit Analysis172 Questions

Exam 22: Master Budgets114 Questions

Exam 23: Flexible Budgets and Standard Cost Systems173 Questions

Exam 24: Cost Allocation and Responsibility Accounting129 Questions

Exam 25: Short-Term Business Decisions161 Questions

Exam 26: Capital Investment Decisions122 Questions

Select questions type

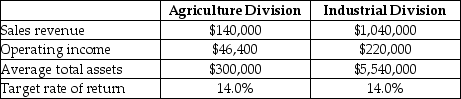

Huntswell Corporation has two major divisions: Agricultural Products and Industrial Products. It provides the following information for the year 2014.  Calculate the profit margin ratio for the Industrial Division of the company.

Calculate the profit margin ratio for the Industrial Division of the company.

Free

(Multiple Choice)

5.0/5  (29)

(29)

Correct Answer: Verified

Verified

C

Traditional costing systems employ multiple allocation rates, but an activity-based costing system uses only one rate for allocating manufacturing overhead.

Free

(True/False)

4.9/5 (40)

Correct Answer:Verified

False

In a balanced scorecard, which of the following is a key performance indicator of the financial perspective?

Free

(Multiple Choice)

4.8/5 (35)

Correct Answer:Verified

D

Brannon Company manufactures ceiling fans and uses an activity-based costing system. Each ceiling fan consists of 20 separate parts. The direct material cost is $95 and each ceiling fan requires 2.5 hours of machine time to manufacture. There is no direct labor cost. Additional information is as follows:  What is the total manufacturing cost per ceiling fan?

What is the total manufacturing cost per ceiling fan?

(Multiple Choice)

4.9/5 (42)

The primary objective in setting transfer prices is to achieve goal congruence by selecting a price that will maximize overall company profits.

(True/False)

4.8/5 (40)

The ROI (Return on Investment)formula focuses on the amount of operating income earned before other revenue/expense items, such as interest expense, by utilizing the average total assets employed for the year.

(True/False)

4.9/5 (43)

In many cases, the amount of the transfer price does not affect the overall company profits.

(True/False)

4.8/5 (38)

The payroll department of a manufacturing company is most likely to be a(n):

(Multiple Choice)

4.8/5 (53)

Performance evaluation systems provide top management with a framework for maintaining control over the entire organization.

(True/False)

4.7/5 (38)

Activity-based costing refines the cost allocation process even more than the traditional allocation costing.

(True/False)

5.0/5 (41)

Which of the following is the correct formula for calculating return on investment?

(Multiple Choice)

4.7/5 (39)

Huntswell Corporation has two major divisions: Agricultural Products and Industrial Products. It provides the following information for the year 2014  Calculate the residual income for the Agriculture division.

Calculate the residual income for the Agriculture division.

(Multiple Choice)

4.8/5 (34)

Which of the following statements is correct regarding the activity-based costing system?

(Multiple Choice)

4.8/5 (44)

Cost center responsibility reports generally focus on the static budget variance.

(True/False)

4.8/5 (38)

Which of the following is the most appropriate cost driver for allocating the cost of warranty services?

(Multiple Choice)

4.9/5 (41)

Which of the following statements most accurately describes residual income?

(Multiple Choice)

4.8/5 (27)

Smaller variances signal that operations are close to target and do not require management's immediate attention.

(True/False)

4.9/5 (33)

The manager of a cost center is responsible for controlling costs and generating revenues of the company.

(True/False)

4.9/5 (47)

Operating income alone does not indicate how efficiently a segment is using its assets.

(True/False)

4.8/5 (36)

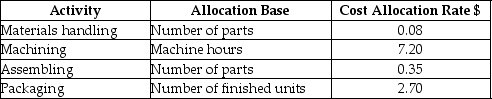

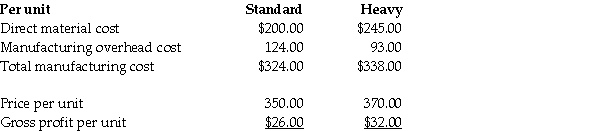

AAA Metal Bearings produces two sizes of metal bearings (sold by the crate)-standard and heavy. The standard bearings require $200 of direct materials per unit (per crate)and the heavy bearings require $245 of direct materials per unit. The operation is mechanized and there is no direct labor. Previously AAA used a single plant-wide allocation rate for manufacturing overhead, which was $1.55 per machine hour. Based on the single rate, gross profit was as follows:  Although the data showed that the heavy bearings were more profitable than the standard bearings, the plant manager knew that the heavy bearings required much more processing in the metal fabrication phase than the standard bearings, and that this factor was not adequately reflected in the single allocation rate. He suspected that it was distorting the profit data. He suggested adopting an activity-based costing approach.

Working together, the engineers and accountants identified the following three manufacturing activities, and broke down the annual overhead costs as shown below:

Although the data showed that the heavy bearings were more profitable than the standard bearings, the plant manager knew that the heavy bearings required much more processing in the metal fabrication phase than the standard bearings, and that this factor was not adequately reflected in the single allocation rate. He suspected that it was distorting the profit data. He suggested adopting an activity-based costing approach.

Working together, the engineers and accountants identified the following three manufacturing activities, and broke down the annual overhead costs as shown below:  Engineers believed that metal fabrication costs should be allocated by weight, and estimated that the plant processed 12,000 kilos of metal per year. Machine processing costs were correlated to machine hours, and the engineers estimated a total of 380,000 machine hours for the year. Packaging costs were the same for both types of products, and so they could be allocated simply by the number of units produced. The production plan provided for 4,000 units of standard and 1,000 units of heavy bearings to be produced during the year. Additional data on a per unit basis was as given below:

Engineers believed that metal fabrication costs should be allocated by weight, and estimated that the plant processed 12,000 kilos of metal per year. Machine processing costs were correlated to machine hours, and the engineers estimated a total of 380,000 machine hours for the year. Packaging costs were the same for both types of products, and so they could be allocated simply by the number of units produced. The production plan provided for 4,000 units of standard and 1,000 units of heavy bearings to be produced during the year. Additional data on a per unit basis was as given below:  Using the data above, calculate activity rates. Then, following the ABC methodology, calculate the production cost and gross profit for one unit of standard bearings. (Round your intermediate calculations to two decimal places).

Using the data above, calculate activity rates. Then, following the ABC methodology, calculate the production cost and gross profit for one unit of standard bearings. (Round your intermediate calculations to two decimal places).

(Essay)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)