Exam 10: Monopolistic Competition : The Competitive Model in More Realistic Setting

Exam 1: Economics Foundations and Models160 Questions

Exam 2: Choices and Trade - Offs in the Market192 Questions

Exam 3: Where Prices Come Frome : The Interaction of Demand and Supply202 Questions

Exam 4: Elasticity: The Responsiveness of Demand and Supply226 Questions

Exam 5: Economic Efficiency , Government Price Setting and Taxes187 Questions

Exam 6: Concumer Choice and Behavioural Economics254 Questions

Exam 7: Technology , Production and Costs300 Questions

Exam 8: Firms in Perfectly Compitive Markets270 Questions

Exam 9: Monopoly Markets281 Questions

Exam 10: Monopolistic Competition : The Competitive Model in More Realistic Setting255 Questions

Exam 11: Oligopoly : Firms in Less Competitve Markets186 Questions

Exam 12: The Market for Labour and Other Factors of Production253 Questions

Exam 13: International Trade111 Questions

Exam 14: Government Intervention in the Market122 Questions

Exam 15: Externalities , Environmental Policy and Public Goods212 Questions

Exam 16: The Distribution of Income and Social Policy120 Questions

Select questions type

Long-run equilibrium under monopolistic competition is similar to that under perfect competition in that

(Multiple Choice)

4.7/5  (44)

(44)

Tony's Italian Ice is a monopolistically competitive firm. If Tony's earns a profit in the short run, which of the following is most likely to occur?

(Multiple Choice)

4.9/5 (38)

The key characteristics of a monopolistically competitive market structure include

(Multiple Choice)

4.7/5 (35)

To maximise their profits and defend those profits from competitors, monopolistically competitive firms must

(Multiple Choice)

4.8/5 (32)

Suppose that if a local McDonald's restaurant reduces the price of a Big Mac from $4.00 to $3.25, the number of Big Macs it sells per day will increase from 4 to 5. Explain the output effect and the price effect resulting from this change. Using a graph, illustrate both the loss in revenue from selling each of the first 4 Big Macs for $0.75 less and the additional revenue from selling 1 more Big Mac. What is the total change in revenue received which results from this price decrease?

(Essay)

4.8/5 (33)

In both monopolistically competitive and perfectly competitive industries,

(Multiple Choice)

4.9/5 (22)

A monopolistically competitive firm faces a downward-sloping demand curve because

(Multiple Choice)

4.9/5 (39)

Firms in monopolistic competition compete by selling similar, but not identical products.

(True/False)

4.9/5 (33)

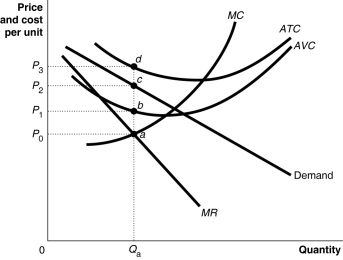

-Refer to Figure 10-4. What is the area that represents the total revenue made by the firm?

-Refer to Figure 10-4. What is the area that represents the total revenue made by the firm?

(Multiple Choice)

4.8/5 (30)

________ describes the actions a firm takes to maintain the differentiation of its product over time.

(Multiple Choice)

4.7/5 (37)

Economists have long debated whether there is a significant loss of well-being to society in markets that are monopolistically competitive rather than perfectly competitive. Which of the following offers the best reason why some economists believe that monopolistically competitive markets are less efficient than perfectly competitive markets?

(Multiple Choice)

4.9/5 (39)

Firms use two marketing tools to differentiate their products. What are these two tools?

(Multiple Choice)

5.0/5 (39)

-Refer to Table 10-5. What are the firm's profit-maximising or loss-minimising price and quantity?

(Multiple Choice)

4.8/5 (29)

Only one of the following statements is correct. The statements compare perfectly competitive (PC) markets and monopolistically competitive (MC) markets. Which statement is correct?

(Multiple Choice)

4.8/5 (32)

Which of the following is not a characteristic of a monopolistically competitive firm in long-run equilibrium?

(Multiple Choice)

4.8/5 (33)

Monopolistically competitive firms achieve allocative efficiency but not productive efficiency.

(True/False)

4.8/5 (40)

A monopolistically competitive firm that is earning profits will, in the long run, experience all of the following except

(Multiple Choice)

4.7/5 (33)

-Refer to Table 10-4. At Victoria's profit-maximising output,

(Multiple Choice)

4.8/5 (39)

New firms are able to enter monopolistically competitive markets because there are low barriers to entry.

(True/False)

4.8/5 (39)

Long-run equilibrium in a monopolistically competitive market is similar to long-run equilibrium in a perfectly competitive market in that in both markets, firms

(Multiple Choice)

4.7/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)